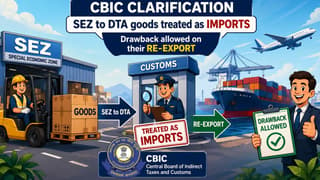

The Central Board of Indirect Taxes and Customs issued a clarification stating SEZ to DTA goods were treated as imports and allowed drawback on their re-export under Section 74 of the Customs Act, 1962.

Kashish Bhardwaj | Apr 30, 2026 |

CBIC Update on SEZ Goods: Re-export from DTA Now Eligible for Drawback

The Central Board of Indirect Taxes and Customs (CBIC) has issued an Instruction No. 06/2026-Customs, dated April 27, 2026, under Section 74 of the Customs Act, 1962. This clarification is regarding eligibility for drawback in case of the supply of goods from SEZ to DTA and subsequent re-export. In this, it has been clarified whether the goods coming from SEZ to DTA will be considered an import or not, and if those goods are re-exported later, whether there will be any drawback on them or not.

In this clarification, it has been told that earlier there were different interpretations in the field offices. In some places, DTA movement from SEZ was not being considered as an import, due to which the drawback was being rejected. Now the CBIC has clarified that an SEZ is treated like foreign territory. So when goods come from an SEZ to a DTA, they will be treated as imports.

Based on this, if the same goods have come to DTA after paying duty and are later re-exported, then they will be considered eligible for drawback. It has also been made clear that the goods should be identifiable, and only those goods should be re-exported that were earlier imported (from SEZ to DTA).

In case of any Doubt regarding Membership you can mail us at [email protected]

Join Studycafe's WhatsApp Group or Telegram Channel for Latest Updates on Government Job, Sarkari Naukri, Private Jobs, Income Tax, GST, Companies Act, Judgements and CA, CS, ICWA, and MUCH MORE!"