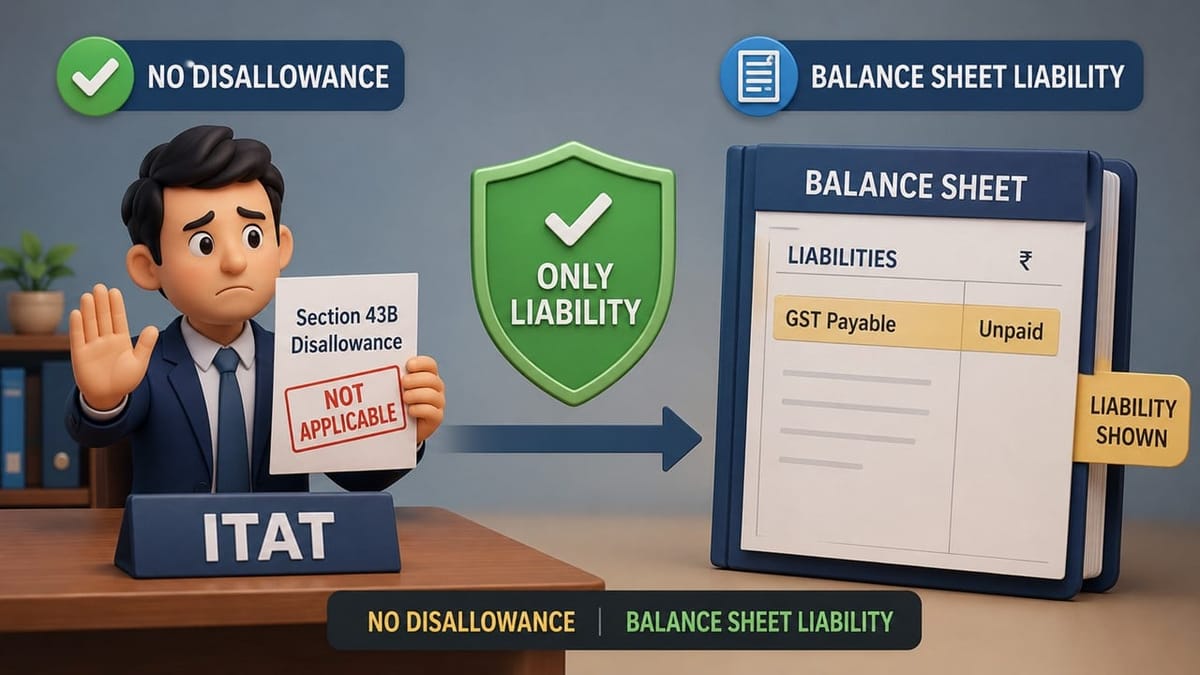

ITAT Delhi held that unpaid GST shown merely as a balance-sheet liability, without being claimed as an expenditure, cannot be disallowed under Section 43B.

Vanshika verma | May 31, 2026 |

No Section 43B Disallowance for Unpaid GST Shown Only as Balance Sheet Liability: ITAT

The Income Tax Appellate Tribunal (ITAT), Delhi Bench, has ruled in favour of KBH Energy & Infra Services Pvt. Ltd for Assessment Year 2019-20 and deleted a GST-related disallowance of Rs 45,62,808 made under Section 43B of the Income Tax Act.

The company had originally filed its income tax return declaring business income of about Rs. 35,92 ,068. While processing the return, the CPC added Rs. 45 ,62,808 towards unpaid GST liability and Rs. 49,288 towards delayed PF payment, increasing the taxable income substantially.

The company objected to the addition of GST, stating that the GST amount outstanding was never claimed as an expense in the Profit & Loss Account. Instead, it appeared on the balance sheet as a current liability. Therefore, the company submitted that none of the deductions claimed by the company was liable to be disallowed under Section 43B.

The CIT(A) agreed that the amount of GST was not debited to the profit & loss account. However, CIT (A) again sustained the disallowance on the ground that GST forms part of turnover and should have been accounted for in a different manner.

The taxpayer before the ITAT had relied on several judicial precedents, including the decisions of Delhi and Ahmedabad Benches of the Tribunal, which held that section 43B applies only in cases where a deduction has been claimed. A tax liability recorded as a balance sheet liability and not claimed as an expense cannot be disallowed.

On reviewing the facts, the Tribunal observed that the GST liability of Rs. 45,62 ,808 was not reflected in the Profit & Loss Account nor claimed as a deduction. The Tribunal noted that the CIT(A) has admitted this fact but has not assigned any legal basis for sustaining the disallowance.

The ITAT relied on earlier Tribunal decisions and High Courts’ judgements and held that Section 43B cannot be invoked where no deduction has been claimed by the assessee.

Accordingly, the Tribunal deleted the entire GST disallowance and allowed the appeal of the assessee.

In case of any Doubt regarding Membership you can mail us at [email protected]

Join Studycafe's WhatsApp Group or Telegram Channel for Latest Updates on Government Job, Sarkari Naukri, Private Jobs, Income Tax, GST, Companies Act, Judgements and CA, CS, ICWA, and MUCH MORE!"