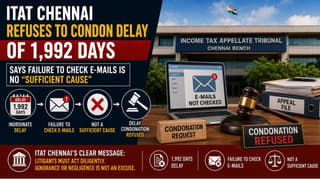

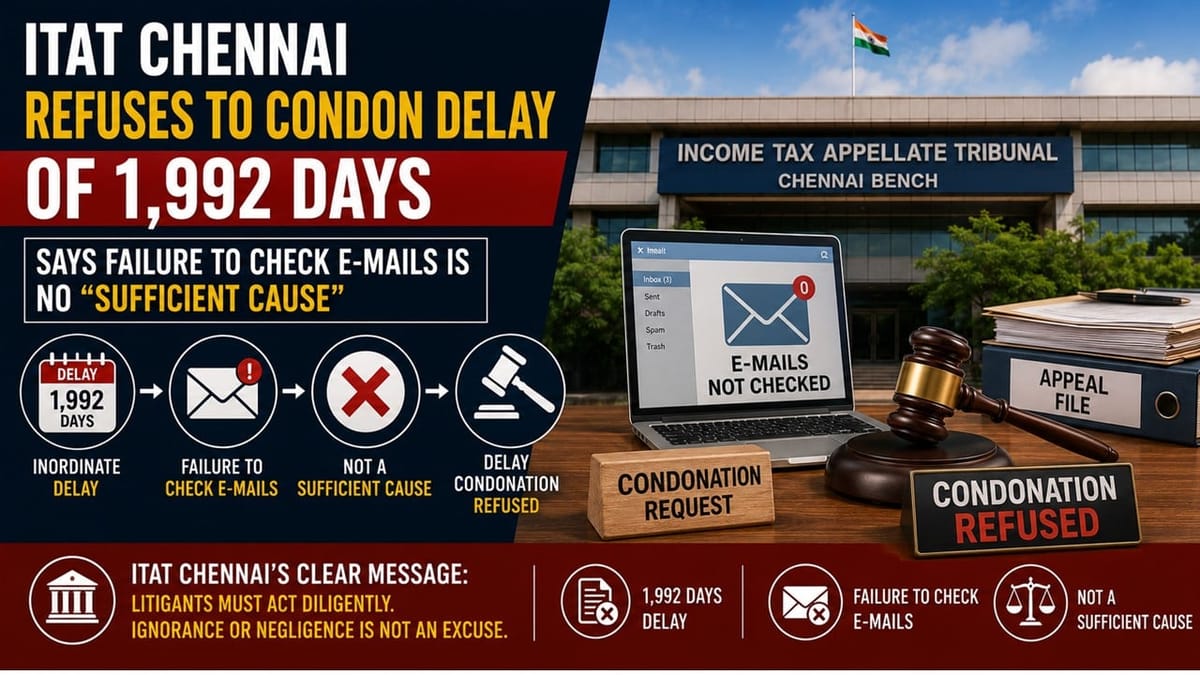

The Income Tax Appellate Tribunal (ITAT) Chennai has held that failure to verify e-mails for an extended period does not constitute a sufficient cause for condonation of delay.

Saima | Jun 15, 2026 |

ITAT Chennai Refuses to Condone Delay of 1,992 Days, Says Failure to Check E-mails is No “Sufficient Cause”

The Income Tax Appellate Tribunal (ITAT) Chennai held that failure to verify e-mails and mere lack of diligence do not constitute “sufficient cause” for condonation of delay.

The assessee is an individual who filed his return of income for AY 2017-18 declaring total income of Rs 36,50,716. While processing the return under Section 143(1) of the Income Tax Act, 1961, the Central Processing Centre (CPC), Bengaluru did not grant the foreign tax credit of Rs 6,26,183 claimed under Section 90 of the Act.Subsequently, the assessee moved an application under Section 154 seeking rectification. However, the CPC rejected the claim and maintained that no foreign tax credit was admissible.

Aggrieved by the order dated 18.07.2019 passed under Section 154, the assessee preferred an appeal before theCIT(A) filed with a delay of 1,992 days. The CIT(A) declined to condone the delay and dismissed the appeal as barred by limitation.

The assessee thereafter approached the ITAT and contended that he was unaware of the intimation issued by the CPC since the communication had been sent to his registered e-mail address, which remained unchecked.

The Tribunal observed that apart from stating that the e-mail containing the intimation was not noticed, the assessee had failed to place any material on record to demonstrate circumstances beyond his control which prevented timely filing of the appeal. The Bench held that although the expression “sufficient cause” deserves liberal interpretation, the party seeking condonation must furnish a bona fide and acceptable explanation covering the entire period of delay.

According to the Tribunal, the assessee had remained inactive for more than five years and had failed to furnish any documentary evidence or specific explanation accounting for the entire period of delay. The explanation offered was vague. Accordingly, the Tribunal held that the assessee had failed to establish any sufficient cause for condonation of delay and it upheld the order of the CIT(A) while dismissing the appeal.

In case of any Doubt regarding Membership you can mail us at [email protected]

Join Studycafe's WhatsApp Group or Telegram Channel for Latest Updates on Government Job, Sarkari Naukri, Private Jobs, Income Tax, GST, Companies Act, Judgements and CA, CS, ICWA, and MUCH MORE!"