Cash found with Advocate sourced from professional fees cannot be taxed as Unexplained Money: ITAT:

Cash found with Advocate sourced from professional fees cannot be taxed as Unexplained Money: ITAT The assessee is a practicing Advocate appearing in…

Unexplained Cash

Table of Contents

ITAT Order:

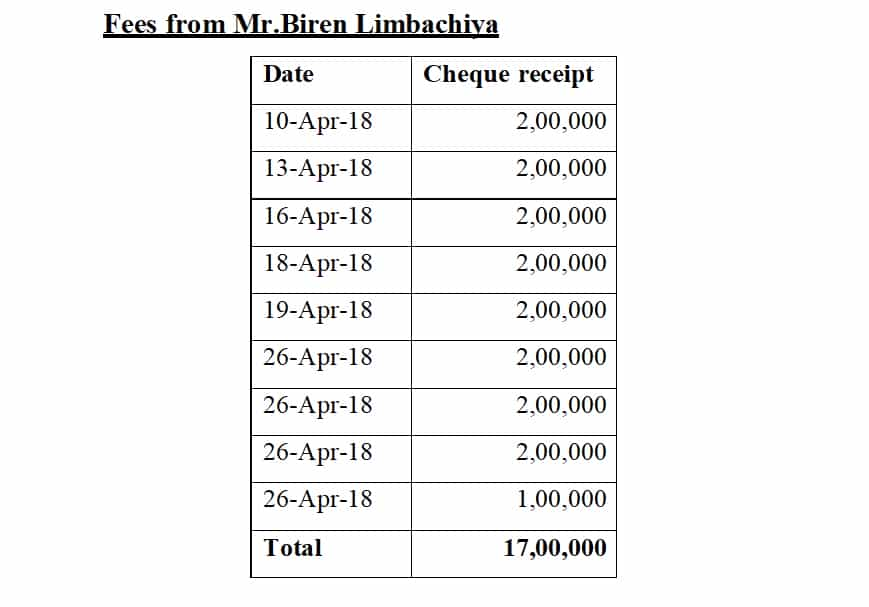

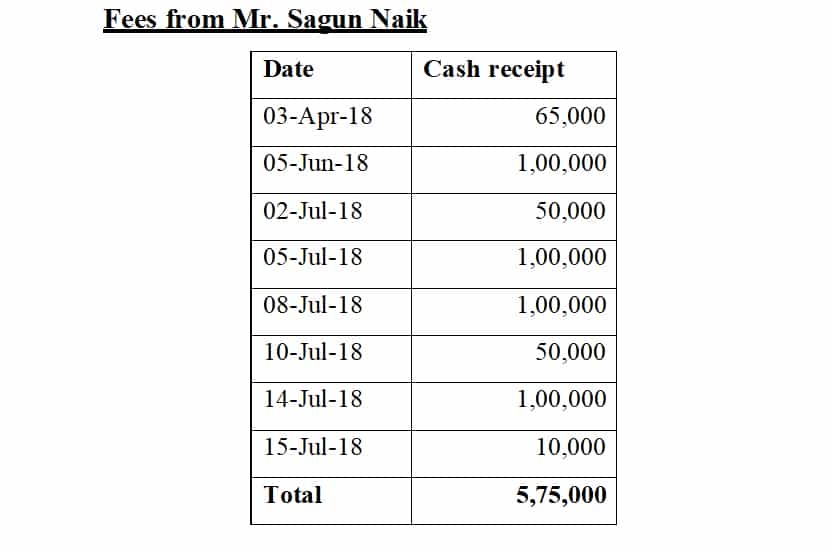

9. We have heard both the parties and perused the material available on record. To recapitulate the fact that the submission of the assessee is that he carried a cash balance of Rs. 16,00,000/- in order to pay the Senior Counsel in Delhi where the case of his clients are listed before the Hon’ble Supreme Court. The assessee further submitted that the source for the cash is from the professional fees which have been counted in the books of accounts. On perusal of records we notice that the assessee has submitted the cash book, bank statement and ledger copy of professional fees etc. before the lower authorities. It is also noticed the date wise breakup of fee received in cash from Mr. Sagun Naik and the receipt of professional fee in cheque from Mr.Biren Limbachiya have also been submitted before the lower authorities. The details submitted by the assessee before the lower authorities is extracted herein below:-

10. On perusal of the ledger account of the professional fees (page 68 to 76 of paper book), we notice that the above amounts have been accounted in the ledger as income. During the course of hearing, the ld. DR submitted that the cash book is not reliable and drew our attention to certain pages in the cash book (page 57 of the paper book) where while recording the transactions on 02.07.2018 it is mentioned as “professional fee received in cash deposited into Bank received from Sagun Naik”. The ld. DR argued that there is no subsequent deposit in the bank and the ld. DR further drew our attention to couple of more entries such entries to submit that the cash book is not reliable. The ld. AR argued that the narration cannot be taken as the deciding factor, The ld AR submitted that these entries towards professional fees have been disclosed as received in cash and have been offered to tax as income. The ld. AR in this regard drew out attention to the ledger account of professional fees received (page 68 to 76 in the paper book) to submit that the impugned in transactions are reconciling to the entries in the professional fees ledger account which would substantiate that the same is already forming part of the taxable income of the assessee. We also notice on perusal of records that the cash balance of the assessee as on the date of confiscation was Rs. 19,81,403/- (page 58 in the paper book). Further the submission that assessee has been periodically withdrawing money from the bank account in cash is also substantiated from the entries in the bank statement (page 59 to 66 of paper book). From the perusal of these facts we see merit in the submissions of the ld. AR that the source for Rs. 16,00,000/- confirmed from the assessee is from his professional income and therefore cannot be treated as unexplained. Before the proceeding further we look at the provisions of Section 69A is extracted as under:-

10. On perusal of the ledger account of the professional fees (page 68 to 76 of paper book), we notice that the above amounts have been accounted in the ledger as income. During the course of hearing, the ld. DR submitted that the cash book is not reliable and drew our attention to certain pages in the cash book (page 57 of the paper book) where while recording the transactions on 02.07.2018 it is mentioned as “professional fee received in cash deposited into Bank received from Sagun Naik”. The ld. DR argued that there is no subsequent deposit in the bank and the ld. DR further drew our attention to couple of more entries such entries to submit that the cash book is not reliable. The ld. AR argued that the narration cannot be taken as the deciding factor, The ld AR submitted that these entries towards professional fees have been disclosed as received in cash and have been offered to tax as income. The ld. AR in this regard drew out attention to the ledger account of professional fees received (page 68 to 76 in the paper book) to submit that the impugned in transactions are reconciling to the entries in the professional fees ledger account which would substantiate that the same is already forming part of the taxable income of the assessee. We also notice on perusal of records that the cash balance of the assessee as on the date of confiscation was Rs. 19,81,403/- (page 58 in the paper book). Further the submission that assessee has been periodically withdrawing money from the bank account in cash is also substantiated from the entries in the bank statement (page 59 to 66 of paper book). From the perusal of these facts we see merit in the submissions of the ld. AR that the source for Rs. 16,00,000/- confirmed from the assessee is from his professional income and therefore cannot be treated as unexplained. Before the proceeding further we look at the provisions of Section 69A is extracted as under:-

“ Where in any financial year the assessee is found to be the owner of any money, bullion, jewellery or other valuable article and such money, bullion, jewellery or valuable article is not recorded in the books of account, if any, maintained by him for any source of income, and the assessee offers no explanation about the nature and source of acquisition of the money, bullion, jewellery or other valuable article, or the explanation offered by him is not, in the opinion of the Income- tax Officer, satisfactory, the money and the value of the bullion, jewellery or other valuable article may be deemed to be the income of the assessee for such financial year."

From the plain reading of the above provisions it is clear that the addition under section 69A could be made if the assessee is found to be the owner of money that is not recorded in the books of account and the assessee is not offering explanation about the source of money. In assessee’s case we notice that the assessee has recorded the impugned amount in the books of account and has also offered the same to tax by including the it as professional fees. In view of these discussions and considering the facts of the present case, we are of the view that the amount cannot be treated as unexplained and therefore we delete the addition u/s 69A of the Act. For Official Judgment Download PDF Given Below:About Author

CA Pratibha Goyal

Co Founder

Studycafe

Studycafe New Delhi, Delhi, India

New Delhi, Delhi, India 1486

1486My Recent Articles

- Biggest Labour Reform in Indian History: 4 Labour Codes Effective from today

- Tax Audit and ITR Due date not extended in this case: Know More

- Government notifies Agreement and Protocol between India and Qatar [Read Notification]

- CA Breaking: Results of ICAI Examination to be announced soon, Know probable Date

- Breaking: GSTR-3B Due Date for September 2025 extended by CBIC amid Diwali Festivities

Loading suggestions…

Recent Posts

All Posts

Recent Posts

All Posts