Cash Transactions to be reported in Income Tax SFT:

IT Dept. has decided the value and nature of transactions for various entities that will help in deciding when to do SFT filing.

Filing Statement of Financial Transactions

Table of Contents

Cash Transactions to be reported in Income Tax SFT

The Income Tax Department of India has decided the value and nature of transactions for various entities that will help in deciding when to do SFT filing. The SFT transaction in 26S specifies all the transactions, such as investments, expenditures and more, beyond taxpayers' decision or threshold limit.

The Income Tax Department will use SFTs to record information on certain high-value transactions as specified in Section 285BA of the Income Tax Act of 1961.

The Income Tax Department will use SFTs to record information on certain high-value transactions as specified in Section 285BA of the Income Tax Act of 1961.

Section 285BA

Section 285BA, read with Rule 114E, of the Income Tax Act of 1961 requires specified entities to furnish details of Specified Financial Transactions (SFTs) or any reportable account registered, recorded, or maintained by them throughout the financial year. The information is submitted in Form 61A, which includes several sections for collecting SFT-related information. All high-value transactions are registered on Form 61A, which allows the Income Tax Department to keep track of them.Transactions Required to be Reported under SFT

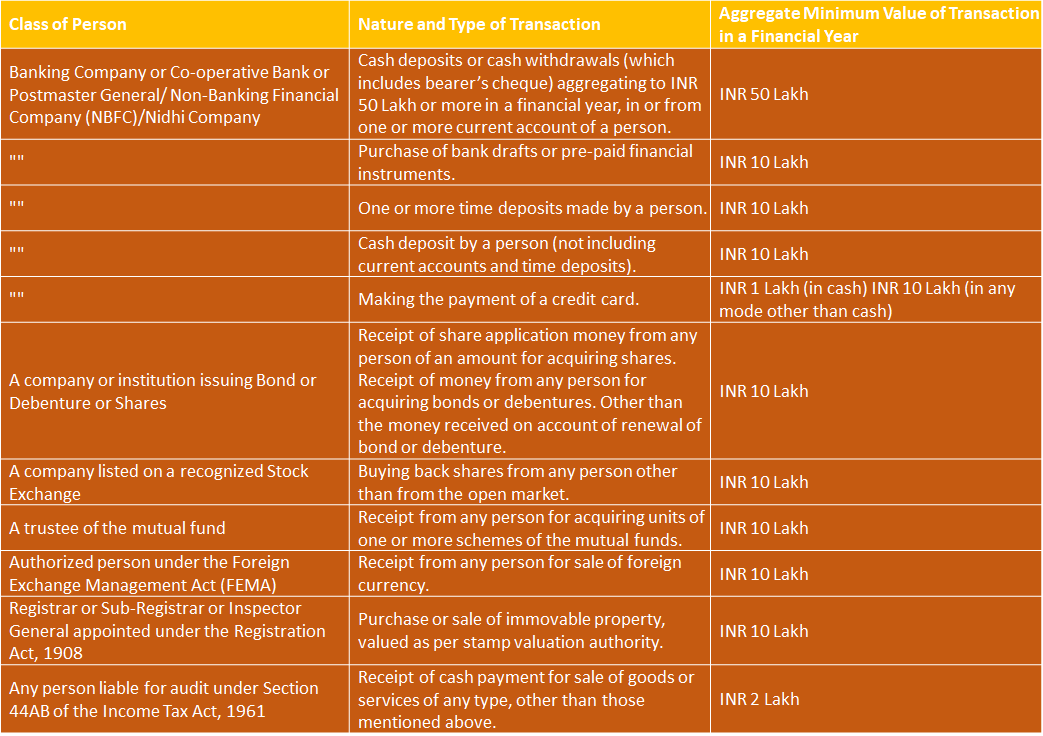

The following transactions should be reported under SFT:SFT Format

Form 61A is divided into different components, including: Part A: It seeks statement-related information and is frequent in all types of transactions. This component requires the following information: reporting entity details, statement details, and principal office details. Part B: Report on aggregated financial transactions. It is a person-based report. This component requires information such as the report number, individual details, a financial transaction summary, and financial transaction details. Part C: Report information for a bank or post office account. It's account-based reporting. This area requires the following information: report number, account details, account summary, and personal information. Part D: Immovable property transfers require detailed reporting. It is transactional reporting. This area requires the following information: the report number, transaction data, and personal details.SFT Filing Required by Persons

The following persons should file SFT or reportable accounts registered, recorded, or maintained by them during the reporting period:- A financial institution is either a bank or a cooperative bank.

- A Non-Banking Financial Company (NBFC).

- An entity that issues credit cards.

- An individual or entity to whom an audit under Section 44AB of the Income Tax Act of 1961 applies.

- Postal Service Offices.

- A company issuing shares.

- A company that issues bonds or debentures.

- A Nidhi Company is specified in Section 406 of the Companies Act, 2013.

- A mutual fund company.

- A company listed on the recognised stock exchange.

- A mutual fund trustee or an authorized representative of the trustee.

- An Inspector General or Sub-Registrar appointed under the Registration Act of 1908.

- Offshore banking units, money changers, authorized dealers, and others as defined by the Foreign Exchange Management Act of 1999.

Steps to File SFT

To easily file an SFT via the income tax portal, follow the procedures below: Step 1: Visit at Income Tax Insight portal and access the ‘Resources’ section. Download the Report Generation and Validation Utility Form 61A, and Generic Submission Utility. Step 2: Follow the preparation recommendations to create the general and transaction-specific SFT in the recommended format. Step 3: Once completed, digitally sign the form and send it to the reporting portal using the designated director's login credentials. Step 4: After successfully completing the online submission, an acknowledgement number will be emailed to the registered email address.Due Date of Filing SFT

The SFT must be digitally signed and sent electronically in Form 61A to the Director of Income Tax (Intelligence and Criminal Investigation) or the Joint Director of Income Tax (Intelligence and Criminal Investigation). The deadline for submitting SFTs is May 31, of the year after the preceding year in which the transaction occurred.Consequences of failing to file SFT on Time

Failure to submit SFT before the deadline will result in punitive repercussions under Section 271FA. The penalty for default could be INR 500 per day. Furthermore, Section 285BA(5) empowers income tax officials to issue notices to individuals who fail to file SFT within 30 days of receiving the notice or within the time-frame indicated in the notice. Failure to do so will result in a penalty of INR 1,000 per day beginning with the expiration of the notice period.Filing Inaccurate or Defective SFT

If anybody learns or discovers an inaccuracy in the information supplied in the SFT after filing it, he must tell the appropriate authorities within 10 days of discovering the discrepancy. He must supply accurate facts. Furthermore, if there is a deficiency in the SFT filed by the person, the income tax authority may warn him and give him the opportunity to amend the same within 30 days of such notification, or within such extended term as the income tax authority may specify. If the person fails to correct the deficiency within a defined time period, the SFT is deemed invalid, and the provisions of this Act apply as if the person had omitted to provide the SFT. However, effective September 1, 2019, failure to correct the flaw in the SFT will be considered submission of incorrect information in the SFT.Consequence of providing inaccurate or defective information in SFT

According to Section 271FAA of the Income Tax Act, 1961, if the specified reporting financial institution referred to in Section 285BA(1) that is required to file an SFT or reportable account gives erroneous information in SFT, and where:- The error is caused by a failure to comply with the due diligence obligations, or it is intentionally developed by that person.

- When a person is aware of an inaccuracy but fails to report it to the proper authority or agency.

- When an inaccuracy is discovered after the SFT has been filed, and the proper information is not provided within 10 days.

- The specified income-tax authority may then impose a penalty of INR 50,000 on the defaulting person.

SFT provided by a Prescribed Reporting Financial Institution

Section 285BA further requires the designated reporting financial institution to establish an SFT or reportable account to promote the effective exchange of information between residents and non-residents. The statement for each calendar year must be submitted in Form 61B by May 31 of the following year.About Author

PRATEEK MAURYA

<a href="https://explain24.com" target="_blank">Explain24</a> <a href="https://pngtovtf.com/png-to-vtf-converter/" target="_blank">PNG to VTF</a>

StudyCafe

StudyCafe Prayagraj, Uttar Pradesh, India

Prayagraj, Uttar Pradesh, India 77

77My Recent Articles

- ITR Filing 2023-24: How to Download and Understand Form 26AS for Tax Filing

- Instant Mixes Flour of Dosa and Idli subject to 18% GST; Can't be Classified as "Sattu": Gujarat AAAR

- Reliance Power now a Debt-Free Company; Paid all its Debts and Remaining Dues

- GST Teams step up action against Illegal Fuel resale in North Kerala

- GST Officer Voluntarily Surrenders before Jalandhar Court

Up Next

Loading suggestions…

Recent Posts

All Posts

Tags

No tags yet.

Recent Posts

All Posts

Tags

No tags yet.