ICAI Holds CA Guilty Under Clause (8) for Accepting Audit Without Informing Previous Auditor; Penalty Imposed:

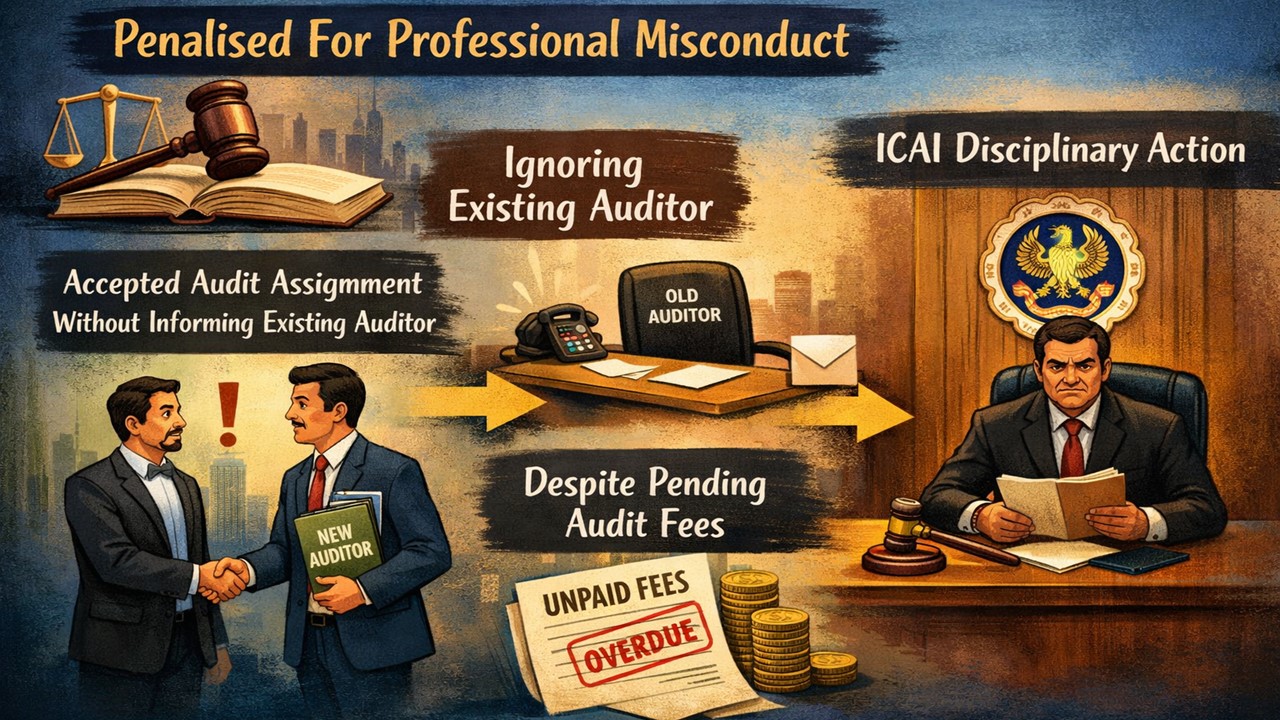

ICAI penalised a CA for professional misconduct after he accepted an audit assignment without informing the existing auditor and despite pending audit fees.

Failure to Inform Previous Auditor Costs CA

ICAI Holds CA Guilty Under Clause (8) for Accepting Audit Without Informing Previous Auditor; Penalty Imposed

The Institute of Chartered Accountants of India (ICAI) Disciplinary Committee (Bench-IV) has held a CA guilty of professional misconduct for contravention of Clause (8) of Part I of the First Schedule to the Chartered Accountants Act, 1949. The final order on the matter was issued on February 10, 2026.

CA Varun Gupta (Complainant) had filed a complaint against CA. Manoj Kumar Jain (Respondent) raised allegations that in the financial year 2019-20, the respondent CA had conducted an audit of M/s Nambirajan Finance Private Limited. The complainant's company was the statutory auditor of the company since FY 2010-11. In FY 2019-20, respondent CA accepted the company's audit; however, till then, the complainant's firm had not resigned or been removed.

The Committee noted that, as per Clause (8) of Part I of the First Schedule to the Act, the respondent should have communicated with the previous auditor in writing before accepting the audit. However, the respondent failed at the same time. The Committee highlighted that this is a compulsory requirement under the ICAI norms to ensure professional transparency and independence, not just a formality.

It was further noted that at the time when the company's audit was accepted by the respondent CA, the previous audit had not paid its outstanding audit fees. According to the Council’s General Guidelines, 2008, an incoming auditor is not permitted to accept an audit of a firm if the previous auditor had not received its outstanding audit fees.

Considering the aforesaid findings, the ICAI Disciplinary Committee held the Chartered Accountant (CA) Manoj Kumar Jain guilty of professional misconduct under Clause (8) of Part I of the First Schedule and Clause (1) of Part II of the Second Schedule to the Chartered Accountants Act, 1949. Also, reprimanded CA and imposed a penalty amounting to Rs. 1 lakh, which is required to be paid within 60 days from the date of receiving the order.

About Author

Saloni Kumari

Content Writer

Saloni is a Content Writer with 2+ years of experience at studycafe.in. She writes legal, taxation, and finance related content including GST, Income Tax etc. Skilled in translating complex judicial pronouncements and regulatory developments into clear, and reader-friendly articles. Experienced in covering judgements of ITAT, High Court, GSTAT, and news related to Income Tax, GST, and corporate law. She can be reached at [email protected].

Saloni is a Content Writer with 2+ years of experience at studycafe.in. She writes legal, taxation, and finance related content including GST, Income Tax etc. Skilled in translating complex judicial pronouncements and regulatory developments into clear, and reader-friendly articles. Experienced in covering judgements of ITAT, High Court, GSTAT, and news related to Income Tax, GST, and corporate law. She can be reached at [email protected].

StudyCafe

StudyCafe Delhi, Delhi, India

Delhi, Delhi, India 2487

2487My Recent Articles

- ITAT Grants Fresh Opportunity to Explain Rs 2.39 Crore Demonetisation Cash Deposit Addition After Main Director’s DeathPremium

- ITAT Grants Taxpayer Fresh Opportunity to Contest Rs 44.16 Lakh Addition After Finding No Decision on MeritsPremium

- Trust’s Sections 12AB and 80G Registration Cannot Be Denied Before Charitable Project Is Completed, Holds ITATPremium

- ITAT Says Identity and Creditworthiness Irrelevant Where Loan Was Directly Paid to Haryana Mining DepartmentPremium

- Earlier Rejection Cannot Be Sole Ground to Reject Fresh Section 12AB and 80G Registration Applications, Says ITATPremium

Up Next

Loading suggestions…

Recent Posts

All Posts

Recent Posts

All Posts