CBIC levied anti-dumping duty on imports of Hydrofluorocarbon Blends

CBIC levied anti-dumping duty on imports of Hydrofluorocarbon Blends Imports of Hydrofluorocarbon (HFC) Blends — The Authority advises imposing an an…

CBIC levied anti-dumping duty on imports of Hydrofluorocarbon Blends

Imports of Hydrofluorocarbon (HFC) Blends — The Authority advises imposing an anti-dumping duty equal to the lesser of the margin of dumping and the margin of injury, in order to protect domestic industry from harm. As a result, the Authority recommends imposing an antidumping duty equivalent to the amount specified in Col. 7 of the duty table appended below on imports of subject goods originating in or exported from the subject country, beginning on the date of the Central Government's notification in this respect. For this purpose, the landed value of imports shall be the assessable value as established by Customs under the Customs Act, 1962, and the corresponding level of custom duties, with the exception of taxes imposed under Sections 3, 3A, 8B, 9, 9A of the Customs Tariff Act, 1975.

Seeks to levy anti-dumping duty on imports of ‘Hydrofluorocarbon Blends (All blends other than 407 and 410 are excluded)’ originating in or exported from China PR for a period of five years- Notification No. 76/2021-Customs (ADD)

G.S.R.—(E). – – In the case of "Hydrofluorocarbon (HFC) Blends," however. All blends except 407 and 410 are prohibited." (hereinafter referred to as the subject goods), falling under tariff item 3824 78 00 of the First Schedule to the Customs Tariff Act, 1975 (51 of 1975) (hereinafter referred to as the Customs Tariff Act), originating in, or exported from the People's Republic of China (hereinafter referred to as the subject country), and imported into India, the designated authority in its final findings vide notification F. No. 06/34/2020-DGTR, dated September 27, 2021.

(i) the product under consideration has been exported at a price below normal value, resulting in dumping; (ii) the domestic industry has suffered material injury; (iii) there is a causal link between dumping of the product under consideration and injury to the domestic industry; and (iv) there is a causal link between dumping of the product under consideration and injury to the domestic industry, and has recommended imposition of anti-dumping duty on imports of the subject goods, originating in, or exported from from the subject countries and imported into India, in order to remove injury to the domestic industry.

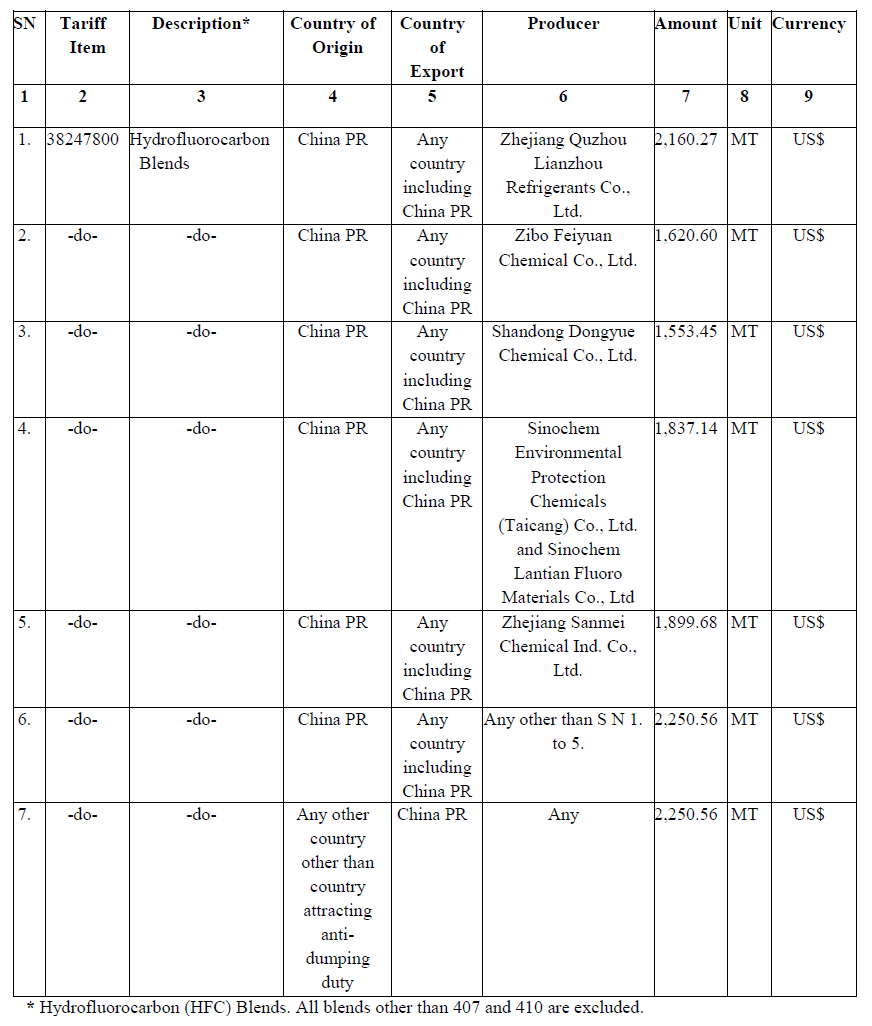

Now, in exercise of the powers conferred by sub-sections (1) and (5) of section 9A of the Customs Tariff Act, read with rules 18 and 20 of the Customs Tariff (Identification, Assessment and Collection of Anti-dumping Duty on Dumped Articles and for Determination of Injury) Rules, 1995, the Central Government, after considering the aforesaid final findings of the designated authority, hereby imposes on the subject goods, the description of which is specified in sub-section (3) of the Table below, falling under the tariff item of the First Schedule to the Customs Tariff Act as specified in the corresponding entry in column (2), originating in the countries as specified in the corresponding entry in column (4), exported from the countries as specified in the corresponding entry in column (5), produced by the producers as specified in the corresponding entry in column (6), and imported into India, an anti-dumping duty at the rate equal to the amount as specified in the corresponding entry in column (7), in the currency as specified in the corresponding entry in column (9) and as per unit of measurement as specified in the corresponding entry in column (8) of the said Table, namely :-

The anti-dumping duty imposed by this notification will be due in Indian currency for a period of five years (unless cancelled, superseded, or amended earlier) from the date of publication of this notification in the Official Gazette.

Explanation.- For the purposes of this notification, the rate of exchange applicable for the purpose of calculating such anti-dumping duty shall be the rate specified in the notification issued from time to time by the Government of India, through the Ministry of Finance (Department of Revenue), in exercise of the powers conferred by section 14 of the Customs Act, 1962 (52 of 1962), and the relevant date for determining the rate of exchange shall be the date.

To Read Notification Download PDF Given Below:

The anti-dumping duty imposed by this notification will be due in Indian currency for a period of five years (unless cancelled, superseded, or amended earlier) from the date of publication of this notification in the Official Gazette.

Explanation.- For the purposes of this notification, the rate of exchange applicable for the purpose of calculating such anti-dumping duty shall be the rate specified in the notification issued from time to time by the Government of India, through the Ministry of Finance (Department of Revenue), in exercise of the powers conferred by section 14 of the Customs Act, 1962 (52 of 1962), and the relevant date for determining the rate of exchange shall be the date.

To Read Notification Download PDF Given Below:

The anti-dumping duty imposed by this notification will be due in Indian currency for a period of five years (unless cancelled, superseded, or amended earlier) from the date of publication of this notification in the Official Gazette.

Explanation.- For the purposes of this notification, the rate of exchange applicable for the purpose of calculating such anti-dumping duty shall be the rate specified in the notification issued from time to time by the Government of India, through the Ministry of Finance (Department of Revenue), in exercise of the powers conferred by section 14 of the Customs Act, 1962 (52 of 1962), and the relevant date for determining the rate of exchange shall be the date.

To Read Notification Download PDF Given Below:About Author

Sushmita Goswami

Content Manager

Sushmita Goswami is a content writer with 2+ years of experience in Finance, Recruitment, Education and career Related Content. She is a Graduate from Delhi University in Journalism and Mass Communication

Sushmita Goswami is a content writer with 2+ years of experience in Finance, Recruitment, Education and career Related Content. She is a Graduate from Delhi University in Journalism and Mass Communication

Studycafe

Studycafe  New Delhi , Delhi, India

New Delhi , Delhi, India 886

886My Recent Articles

- What to Consider When Choosing an Online Trading Platform?

- Post Office Franchise Scheme: Take Post Office Franchise at Rs 5000 and Earn Commission upto 20%; Check Details Here

- IAN invests INR 4.5 crore in Fintech NBFC Indium Finance

- UPI a Digital Public Good, No Charges in Consideration: Finance Ministry

- ITR Filing Penalty: Check Taxpayers Exempt from Paying a Late Fee even Missing the Deadline

Up Next

Loading suggestions…

Recent Posts

All Posts

Recent Posts

All Posts