Delhi GST issues instruction on Verification and monitoring in cases of reversal of ineligible ITC:

Delhi GST has issued guidelines to ensure correct reversal and reporting of ineligible ITC in GSTR-3B.

Delhi GST Issues New Guidelines for Proper Reversal and Reporting of Ineligible ITC

Delhi GST Issues Instruction on Verification and Monitoring in Cases of Reversal of Ineligible ITC

Incorrect reporting in GSTR-3B, particularly of IGST ITC on exempt outward supplies, can distort settlement to the State, especially when reversal of ineligible credit is not properly declared.

In some cases, it has been noticed that there is a huge input tax credit on inward supplies, but outward supplies are exempted. In such cases, the taxpayer doesn't reverse the IGST Credit, which is ineligible; the IGST credit will go to the indivisible pool and the IGST settlement gets affected. If the actual ineligible IGST credit is properly reversed by the taxpayers, the State will get 50% of the ineligible credit so reversed every month.

Taxpayers may not be aware of the IGST Settlement through the fund transfer mechanism and do not report their IGST ITC claim and reversal correctly, as they believe there is no intention on their part to evade tax. The IGST amount gets appropriated to the State whenever there is a break in the ITC Chain.

In this regard, Circular No. 01/2022-GST State Tax dated 11.10.2022, has also been issued by this Department where in Para 4 detailed guidelines for availment of ineligible ITC and reversal thereof have been provided and all the Ward/Proper Officers are directed to ensure that the guidelines on the subject mater are strictly followed by the taxpayers.

In this regard, the following additional guidelines are being issued for the procedure, verification and monitoring of such cases:

Procedural Clarifications for Reporting ITC in Table 4 in GSTR-3B

To ensure the inflow of IGST Credit eligible to the State, the disclosure of correct figures in GSTR 3B by the taxpayers shall be ensured through the following steps.

To ensure the inflow of IGST Credit eligible to the State, the disclosure of correct figures in GSTR 3B by the taxpayers shall be ensured through the following steps.

- Total ITC to be auto-populated in table 4A from GSTR-2B

- The taxpayer should not deduct the amount of ineligible input tax credit directly by editing the total amount of input tax credit auto-populated in Table 4A of FORM GSTR-3B.

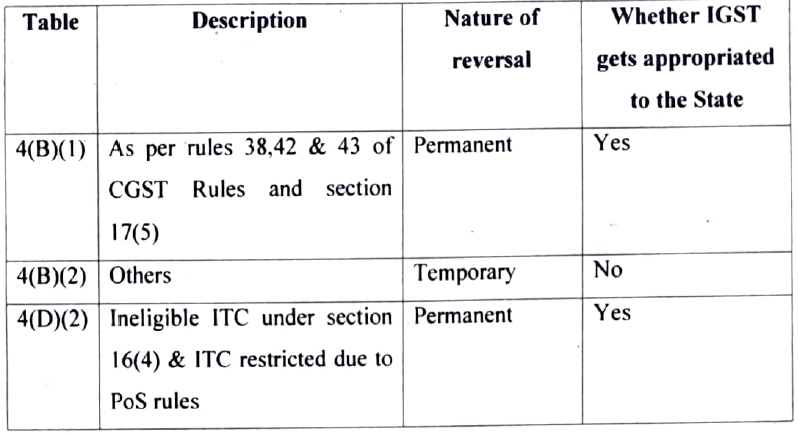

- Permanent reversals (under Section 17(5), Rules 38, 42, 43) must be declared in Table 4(B)(1).

- Temporary reversals (e.g., under Rule 37, Section 16(2)) to be shown in Table 4(B)(2) and reclaimable upon conditions being met.

- Net ITC = Table 4(A) - [4(B)(1) + 4(B)(2)].

To ensure the inflow of IGST Credit eligible to the State, the disclosure of correct figures in GSTR 3B by the taxpayers shall be ensured through the following steps.About Author

CA Pratibha Goyal

Co Founder

CA Pratibha Goyal is Chartered Accountant qualified in 2016, is a Member of The Institute of Chartered Accountants of India having wide experience in the field of Auditing, Taxation, ROC, GST and Secretarial matters etc.

She has written over a thousand articles & has made several videos on topics related to Auditing & Taxation. As a Speaker she has delivered various sessions on various branches of NIRC of ICAI.

CA Pratibha Goyal is Chartered Accountant qualified in 2016, is a Member of The Institute of Chartered Accountants of India having wide experience in the field of Auditing, Taxation, ROC, GST and Secretarial matters etc.

She has written over a thousand articles & has made several videos on topics related to Auditing & Taxation. As a Speaker she has delivered various sessions on various branches of NIRC of ICAI.

Studycafe

Studycafe New Delhi, Delhi, India

New Delhi, Delhi, India 1486

1486My Recent Articles

- Biggest Labour Reform in Indian History: 4 Labour Codes Effective from today

- Tax Audit and ITR Due date not extended in this case: Know More

- Government notifies Agreement and Protocol between India and Qatar [Read Notification]

- CA Breaking: Results of ICAI Examination to be announced soon, Know probable Date

- Breaking: GSTR-3B Due Date for September 2025 extended by CBIC amid Diwali Festivities

Up Next

Loading suggestions…

Recent Posts

All Posts

Tags

No tags yet.

Recent Posts

All Posts

Tags

No tags yet.