Demonetization Cash Deposits Addition Deleted as Books Fully Explained Cash Balance:

Income Tax Addition for Unexplained Cash Deposits During Demonetization Period deleted for Cash Balance Backed by Books of account and computation of income

ITAT Sets Aside Assessment Order in Unxplained Cash Deposits Dispute

Demonetization Cash Deposits Addition Deleted as Books Fully Explained Cash Balance

The Income Tax Appellate Tribunal (ITAT) restored a matter involving additions made towards the alleged unexplained cash deposits made during the demonetization period.

The income tax return (ITR) filed by the assessee, Sabrunnisa Israr Ahmad Shaikh, was selected for scrutiny, and during the proceedings, the AO questioned the cash deposits of Rs 12 lakh made by the assessee during the demonetization period. The assessee, to substantiate the source of the deposits, submitted a copy of the capital account, balance sheet, and computation of income. The AO, however, noted that the assessee did not have enough cash balance to make a deposit of Rs 12 lakh in the Specified Bank Notes during the demonetization period. Therefore, the AO passed an order holding that the assessee failed to prove the source of the cash deposits.

During the proceedings, the assessee paid Rs 2,27,332 tax under the head "income from other sources." Therefore, the AO restricted the addition to Rs 9,72,668 under section 69A, treating it as income from undisclosed sources. The CIT(A) also upheld this addition. Therefore, the assessee approached the ITAT.

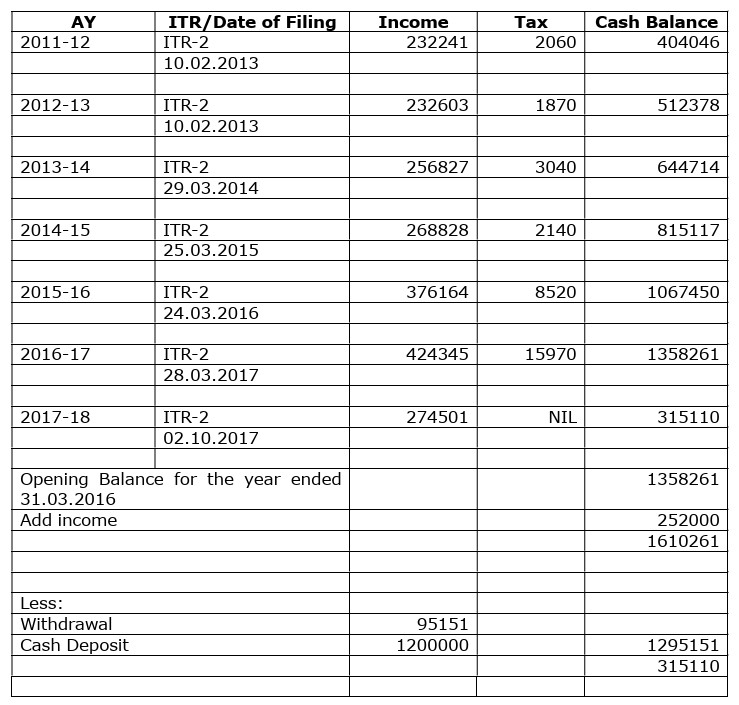

The assessee contended that the cash deposits were the accumulated past savings. She submitted that she earns income from two properties and from a sweet shop run by her husband. The assessee also produced a copy of the cash flow statement showing the opening cash balance as Rs 13,58,261 as of 01/04/2016, and the Rs 12 lakh deposit was made out of this balance.

The ITAT agreed with the contentions of the assessee, noting that the lower authorities did not consider the cash flow statement submitted by the assessee. Since the lower authorities did not properly examine the cash balance in the cash flow statement, the ITAT restored the issue to the Assessing Officer for fresh consideration. The AO was directed to verify the details submitted by the assessee in the cash flow statement. The assessee was also directed to comply with the notices and submit the details asked by the AO.

Accordingly, the tribunal set aside the order.

The ITAT agreed with the contentions of the assessee, noting that the lower authorities did not consider the cash flow statement submitted by the assessee. Since the lower authorities did not properly examine the cash balance in the cash flow statement, the ITAT restored the issue to the Assessing Officer for fresh consideration. The AO was directed to verify the details submitted by the assessee in the cash flow statement. The assessee was also directed to comply with the notices and submit the details asked by the AO.

Accordingly, the tribunal set aside the order.

The ITAT agreed with the contentions of the assessee, noting that the lower authorities did not consider the cash flow statement submitted by the assessee. Since the lower authorities did not properly examine the cash balance in the cash flow statement, the ITAT restored the issue to the Assessing Officer for fresh consideration. The AO was directed to verify the details submitted by the assessee in the cash flow statement. The assessee was also directed to comply with the notices and submit the details asked by the AO.

Accordingly, the tribunal set aside the order.About Author

Nidhi

Content Writer

Nidhi is a skilled content writer specializing in personal finance. She creates clear, engaging articles on mutual funds, investments, insurance, and wealth-building strategies. With a passion for simplifying complex financial topics, Nidhi helps readers make informed money decisions with confidence. She can be reached at [email protected]

Nidhi is a skilled content writer specializing in personal finance. She creates clear, engaging articles on mutual funds, investments, insurance, and wealth-building strategies. With a passion for simplifying complex financial topics, Nidhi helps readers make informed money decisions with confidence. She can be reached at [email protected]

Studycafe

Studycafe New Delhi, Delhi, India

New Delhi, Delhi, India 1832

1832My Recent Articles

- Karnataka High Court Gives Another Chance in GST Matter Due to Lack of Hearing

- Delay Should Be Condoned if Explanation is Unrefuted: ITAT

- Non-Service of Income Tax Notice, Ill health of taxpayer, ITAT condones Appeal filing delay

- Books of Accounts Cannot be Rejected Without Any Specific Defect: ITAT Kolkata

- Karnataka High Court Sends ITC Matter Back to GST Authorities for Reconsideration

Up Next

Loading suggestions…

Recent Posts

All Posts

Tags

Recent Posts

All Posts