Goodbye Multiple TDS Forms! IT Dept Notifies New Unified Form 141; Effective April 2026:

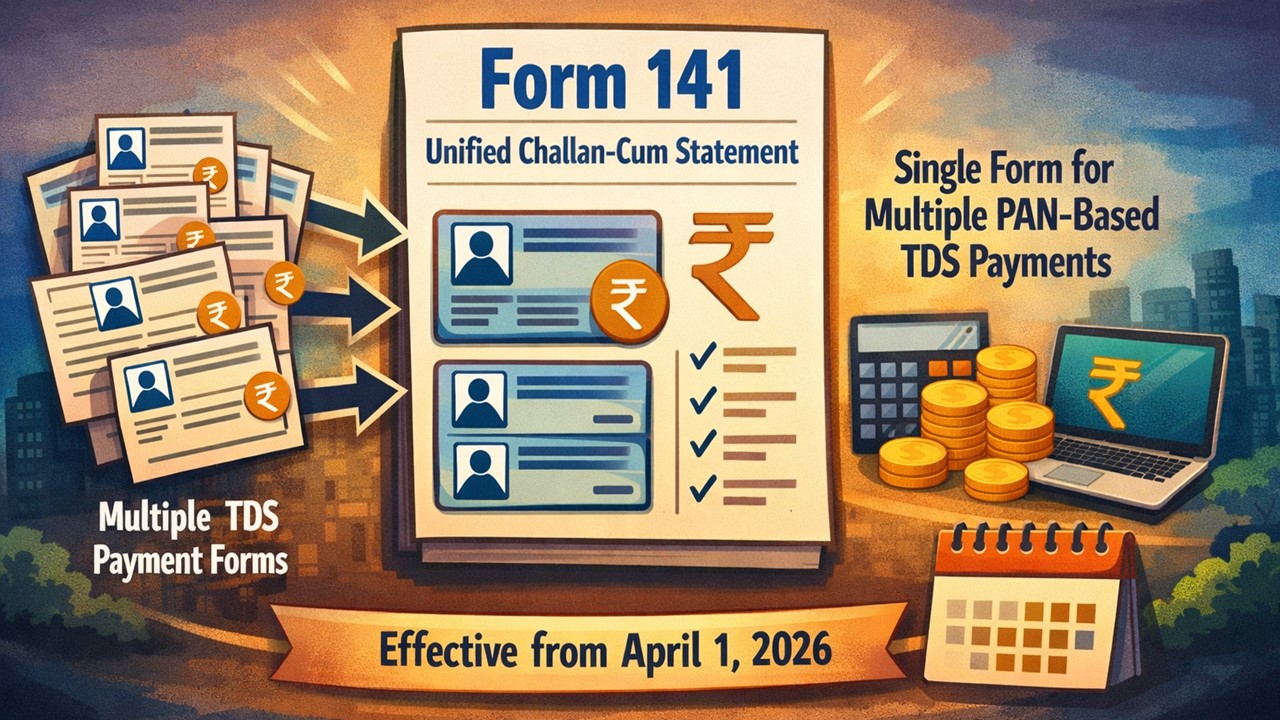

Form 141 is a unified challan-cum-statement that simplifies multiple PAN-based TDS payments into a single, easy-to-use form effective from April 1, 2026.

Form 141 Replaces All Major TDS Forms

Table of Contents

Goodbye Multiple TDS Forms! IT Dept Notifies New Unified Form 141; Effective April 2026

The Income Tax Department has notified a new combined challan-cum-statement called Form 141, under Section 393(1) of the Income Tax Act 2025, effective from April 01, 2026. The form has replaced all the existing TDS forms, including Forms 26QB, 26QC, 26QD, and 26QE. Now, taxpayers can make various PAN-based TDS payments using a single unified form, eliminating the need to use multiple forms.

TDS Payments Covered under Form 141

The newly introduced Form 141 can be used for making several TDS payments, including TDS on rent payments exceeding Rs 50,000 per month (previously used Form 26QC), TDS on the transfer of immovable property (agricultural land not included) valued at Rs 50 lakh or more (previously used Form 26QB), TDS on payments to contractors or professionals exceeding Rs 50 lakh in a financial year by individuals/HUFs not subject to tax audit (previously used Form 26QD) and TDS on the transfer of Virtual Digital Assets (VDA) like cryptocurrencies or NFTs (previously used Form 26QE).How to Use Form 141 for Making TDS Payments?

The Form 141 can be accessed at the income tax e-filing portal. To use this form for making any TDS payment, a taxpayer will first need to log in to the Income Tax Portal. Thereafter, move to the “Income Tax Act 2025” section, available on the homepage. Then, select the “New Payment” option. Thereafter, Form 141 will be displayed on the screen. Now, you can proceed to make the TDS payment using the form.Details Required to Fill From 141

Taxpayers will need to provide PAN details for both the deductor and the deductee while filing the form. Other than that, the address, mobile number, and email ID of both parties and transaction details such as the nature of the service and the payment method will also be needed.About Author

Saloni Kumari

Content Writer

Saloni is a Content Writer with 2+ years of experience at studycafe.in. She writes legal, taxation, and finance related content including GST, Income Tax etc. Skilled in translating complex judicial pronouncements and regulatory developments into clear, and reader-friendly articles. Experienced in covering judgements of ITAT, High Court, GSTAT, and news related to Income Tax, GST, and corporate law. She can be reached at [email protected].

Saloni is a Content Writer with 2+ years of experience at studycafe.in. She writes legal, taxation, and finance related content including GST, Income Tax etc. Skilled in translating complex judicial pronouncements and regulatory developments into clear, and reader-friendly articles. Experienced in covering judgements of ITAT, High Court, GSTAT, and news related to Income Tax, GST, and corporate law. She can be reached at [email protected].

StudyCafe

StudyCafe Delhi, Delhi, India

Delhi, Delhi, India 2487

2487My Recent Articles

- ITAT Grants Fresh Opportunity to Explain Rs 2.39 Crore Demonetisation Cash Deposit Addition After Main Director’s DeathPremium

- ITAT Grants Taxpayer Fresh Opportunity to Contest Rs 44.16 Lakh Addition After Finding No Decision on MeritsPremium

- Trust’s Sections 12AB and 80G Registration Cannot Be Denied Before Charitable Project Is Completed, Holds ITATPremium

- ITAT Says Identity and Creditworthiness Irrelevant Where Loan Was Directly Paid to Haryana Mining DepartmentPremium

- Earlier Rejection Cannot Be Sole Ground to Reject Fresh Section 12AB and 80G Registration Applications, Says ITATPremium

Up Next

Loading suggestions…

Recent Posts

All Posts

Tags

Recent Posts

All Posts