GST Audit 2023: Audit cases likely to be taken up by Department as GST Audit Manual 2023 released:

In a move to help businesses as well as reduce litigation, a Model All India GST Audit Manual 2023 has been finalized for use by the Centre and state tax officials.

GST Audit Manual 2023

Table of Contents

GST Audit 2023: Audit cases likely to be taken up by Department as GST Audit Manual 2023 released

In a move that is expected to help businesses as well as reduce litigation, a Model All India GST Audit Manual 2023 has been finalized for use by the Centre and state tax officials.

Goods and Services Tax in India has stepped towards the completion of five years. One of the main objectives of introduction of GST was to create one common market in the country by totally removing the wide disparities and compliance complexities of various laws of taxation of the States and Centre. In taxation of goods and services (not as "activities", per se, but as "objects" or "events"), that had led to not only tax inefficiency but had also interfered in investment decisions of businesses. GST has provided a uniform structure in taxation of goods and services throughout the country. There is total uniformity in terms of the taxable event, tax rates, point of levy, provisions for registration, return filing, tax payment, refunds, audit, adjudication, appeals etc. In fact, the CGST and SGST laws are almost mirror images. GSTN, as an enabling organisation, has created the necessary digital backbone to ensure seamless uniformity in the process and procedures relating to registration of taxpayers, return filing, tax payment, refunds etc.

Audit processes envisaged under the GST regime are ably assisted by a technological tool named "BI Tools" developed by GSTN, tools of "DGARM", concept of "Registered Person Master File (RPMF)" of DG Audit. Various States also developed technological and analytical tools, such as "e-Shodhane Audit Module" of Karnataka, "Tax Payers at a Glance" by West Bengal, Standard Operating Procedure of Bihar focusing areas of concern in Audit which not only complements and enhances the knowledge of the Audit officers also provides data backups and analysis.

The technological tool is intended to encompass verification, examination, investigation, scrutiny and the like. Members of the Committee, as well as all the Members of the Sub-Committees and their leadership deserve kudos for forging a consensus consistent with the best audit practices.

We hope that the model manual in your hands would lead to implementation of an effective audit mechanism consisting of best practices and procedures tried and tested by the various indirect tax authorities in the country in the interest of revenue, to improve internal control at work in organisations of taxpayers and reduced burden of compliance upon taxpayers.

While emphasis has been placed in this Manual on developing a well-established audit procedure based on sound principles, it is needless to say that there cannot be a uniform approach to the audit of every taxpayer. Occasions may arise when a fact or figure apparent on the documents may need an examination with reference to some other sets of documents or even other sources. Therefore, the scope of audit in GST may vary depending on facts and circumstances of audit. An attempt has been made to address these issues in this document.

A Committee of Officers (CoO) on GST Audit was constituted by the GST Council Secretariat, comprising officers from the CBIC, States, GSTN and GST Council secretariat. The details of the said committee, alongwith its timelines and Terms of References (ToR) are discussed in detail. To explore each of the six ToRs in greater detail, sub-committees were formed for each ToR. The proposal contained in each report of the sub-committees has been incorporated in the relevant Chapter of this Manual.

The task of preparation of a comprehensive All India Model GST Audit Manual (hereinafter called the Model GSTAM/ the Manual) for the Centre and the States was allotted to the Committee of Officers on GST Audit. For this purpose, a sub-committee of officers was constituted to compile existing and desirable audit practices and to draft a model audit manual.

The Model GST Audit Manual has been prepared after incorporating many of these suggestions. The Manual tries to take into account the differential structure of GST revenue administration prevailing in different States and the Centre.

Hence, GST audit is not restricted to the reconciliation of only the tax liability & payment of tax by a taxable person, but its scope is also extended to assessment with reference to the provisions of GST laws.

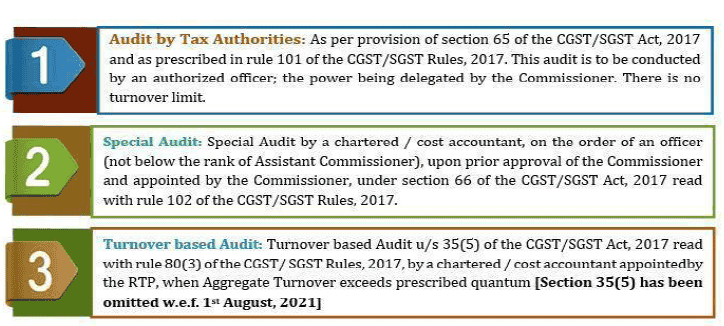

Types of Audit in GST

Three types of Audit are prescribed in GST:

Hence, GST audit is not restricted to the reconciliation of only the tax liability & payment of tax by a taxable person, but its scope is also extended to assessment with reference to the provisions of GST laws.

Types of Audit in GST

Three types of Audit are prescribed in GST:

Note: This Model GST Audit Manual is focused on audit by Tax Authorities only. The audited books of accounts and audit report submitted by the taxpayer in prescribed Form(s) are also subject to audit u/s 65.

To Read More Download PDF Given Below:

Note: This Model GST Audit Manual is focused on audit by Tax Authorities only. The audited books of accounts and audit report submitted by the taxpayer in prescribed Form(s) are also subject to audit u/s 65.

To Read More Download PDF Given Below:

Purpose of this Manual

This Manual aims to be an extensive and comprehensive document with a holistic approach towards GST audit which will not only facilitate the Audit Officers of the Centre and the States/UTs but will also create an impact in facilitating the auditees during the exercise of audit. The objective of this manual is to provide insights into the principles and procedures of audit and to give a holistic view of the entire process to the users of this Manual. In the pre-GST regime, the audit process of States/UTs often got lengthened due to procurement and production of various statutory forms by the auditees in order to claim statutory deductions in the States/UTs. The GST regime does not require production of any such statutory forms and hence it is expected that substantial time of both the auditor and the auditee would be saved. Furthermore, audit in the GST regime has been designed in such a way as to complete the entire process within a short span of time. This will require the officers to concentrate on the process of examination of the books of accounts of a particular auditee within a short timeframe while at the same time yielding optimum results from the auditing exercise. Eventually, this would help the auditee also, who would be relieved from his engagement in the process of auditing sooner than was the case earlier. This manual has been designed to cater to a systematic workflow of audit, ranging from brief criteria of selection to the completion of the process. It includes mechanisms for Joint and Thematic audit as and when they are approved by the Council. It is hoped that this Model Audit Manual would form an important yet dynamic reference for audit principles, practices, and procedures for GST audit practitioners in the country.Chapter 1

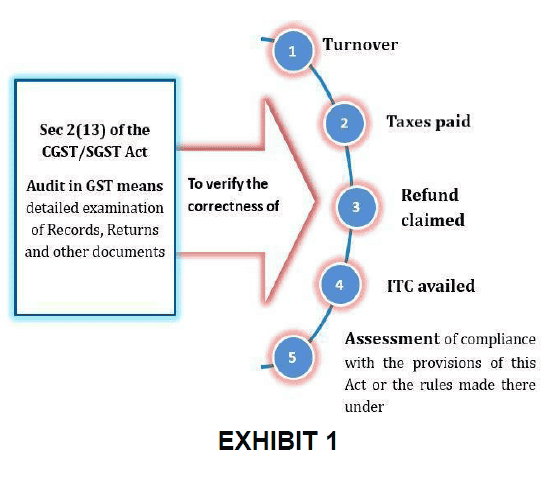

Definition of audit under CGST/SGST Act, 2017 Audit is defined in sub-sec 13 of sec 2 of the CGST/SGST Act, 2017 as – "detailed examination of records, returns and other documents maintained or furnished by the taxable person under this Act or Rules made thereunder or under any other law for the time being in force to verify, inter alia, the correctness of turnover declared, taxes paid, refund claimed and input tax credit availed, and to assess his compliance with the provisions of this Act or rules made thereunder".

Hence, GST audit is not restricted to the reconciliation of only the tax liability & payment of tax by a taxable person, but its scope is also extended to assessment with reference to the provisions of GST laws.

Types of Audit in GST

Three types of Audit are prescribed in GST:

Note: This Model GST Audit Manual is focused on audit by Tax Authorities only. The audited books of accounts and audit report submitted by the taxpayer in prescribed Form(s) are also subject to audit u/s 65.

To Read More Download PDF Given Below:About Author

Reetu

Content Manager

Reetu is a Content Writer with 4+ years of experience in GST, Income Tax, Finance, Company Law, Education and Career Related Content. She is a B.COM (Honrs.) Graduate.

Reetu is a Content Writer with 4+ years of experience in GST, Income Tax, Finance, Company Law, Education and Career Related Content. She is a B.COM (Honrs.) Graduate.

Studycafe

Studycafe Delhi, Delhi, India

Delhi, Delhi, India 8072

8072My Recent Articles

- Income Tax Guide for Indian Defence Personnel for Tax Filing, Taxable Allowances and Other Benefits

- Income Tax Return Breaking: ITR Forms released for AY 25-26

- Ex-DRT Officials Sentenced to 5 Years Rigorous Imprisonment by Madras High Court along with Rs.27 Lakh Fine

- GSTN issued Advisory on Case Sensitivity in IRN Generation

- RBI to issue Notes of Rs.10 and Rs.500 bearing Signature of Guv Malhotra

Up Next

Loading suggestions…

Recent Posts

All Posts

Recent Posts

All Posts