GSTR-10: CA Certification in case of filing GST Final Return

GSTR-10: CA Certification in case of filing GST Final Return A Taxable person, whos GST has been cancelled or who has surrended his GST Numb

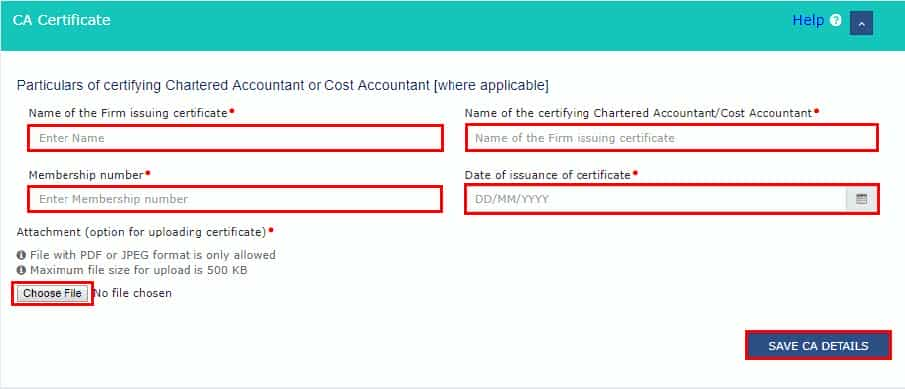

So the Answer here is no. CA Certification is not compulsory while filing GSTR-10, but is required only in case the taxpayer was having stock and tax invoices related to the inputs held in stock are not available.

Legal Text

Rule 44 of CGST Rules 2017, deals with Manner of reversal of credit under special circumstances. Relevant Extract of same is given below for referance.

(1) The amount of input tax credit relating to inputs held in stock, inputs contained in semi-finished and finished goods held in stock, and capital goods held in stock shall, for the purposes of sub-section (4) of section 18 or sub-section (5) of section 29, be determined in the following manner, namely,-

(a) for inputs held in stock and inputs contained in semi-finished and finished goods held in stock, the input tax credit shall be calculated proportionately on the basis of the corresponding invoices on which credit had been availed by the registered taxable person on such inputs;

(b) for capital goods held in stock, the input tax credit involved in the remaining useful life in months shall be computed on pro-rata basis, taking the useful life as five years.

Illustration:

Capital goods have been in use for 4 years, 6 month and 15 days. The useful remaining life in months= 5 months ignoring a part of the month Input tax credit taken on such capital goods= C Input tax credit attributable to remaining useful life= C multiplied by 5/60

(2) The amount, as specified in sub-rule (1) shall be determined separately for input tax credit of central tax, State tax, Union territory tax and integrated tax. (3) Where the tax invoices related to the inputs held in stock are not available, the registered person shall estimate the amount under sub-rule (1) based on the prevailing market price of the goods on the effective date of the occurrence of any of the events specified in sub-section (4) of section 18 or, as the case may be, sub-section (5) of section 29. (4) The amount determined under sub-rule (1) shall form part of the output tax liability of the registered person and the details of the amount shall be furnished in FORM GST ITC-03, where such amount relates to any event specified in sub-section (4) of section 18 and in FORM GSTR-10, where such amount relates to the cancellation of registration. (5) The details furnished in accordance with sub-rule (3) shall be duly certified by a practicing chartered accountant or cost accountant. Rule 81 of CGST Rules 2017, deals with Final return. Same is given below for referance. Every registered person required to furnish a final return under section 45, shall furnish such return electronically in FORM GSTR-10 through the common portal either directly or through a Facilitation Centre notified by the Commissioner. Sub-section (5) of section 29 of CGST Act 2017, deals with Cancellation of Registration. Same is given below for referance. Every registered person whose registration is cancelled shall pay an amount, by way of debit in the electronic credit ledger or electronic cash ledger, equivalent to the credit of input tax in respect of inputs held in stock and inputs contained in semi-finished or finished goods held in stock or capital goods or plant and machinery on the day immediately preceding the date of such cancellation or the output tax payable on such goods, whichever is higher, calculated in such manner as may be prescribed:About Author

CA Pratibha Goyal

Co Founder

Studycafe

Studycafe New Delhi, Delhi, India

New Delhi, Delhi, India 1486

1486My Recent Articles

- Biggest Labour Reform in Indian History: 4 Labour Codes Effective from today

- Tax Audit and ITR Due date not extended in this case: Know More

- Government notifies Agreement and Protocol between India and Qatar [Read Notification]

- CA Breaking: Results of ICAI Examination to be announced soon, Know probable Date

- Breaking: GSTR-3B Due Date for September 2025 extended by CBIC amid Diwali Festivities

Loading suggestions…

Recent Posts

All Posts

Tags

No tags yet.

Recent Posts

All Posts

Tags

No tags yet.