HC Upholds Taxpayer’s Right to Avail ITC; Holds Extended Deadline Overrides Earlier GST Time Limit:

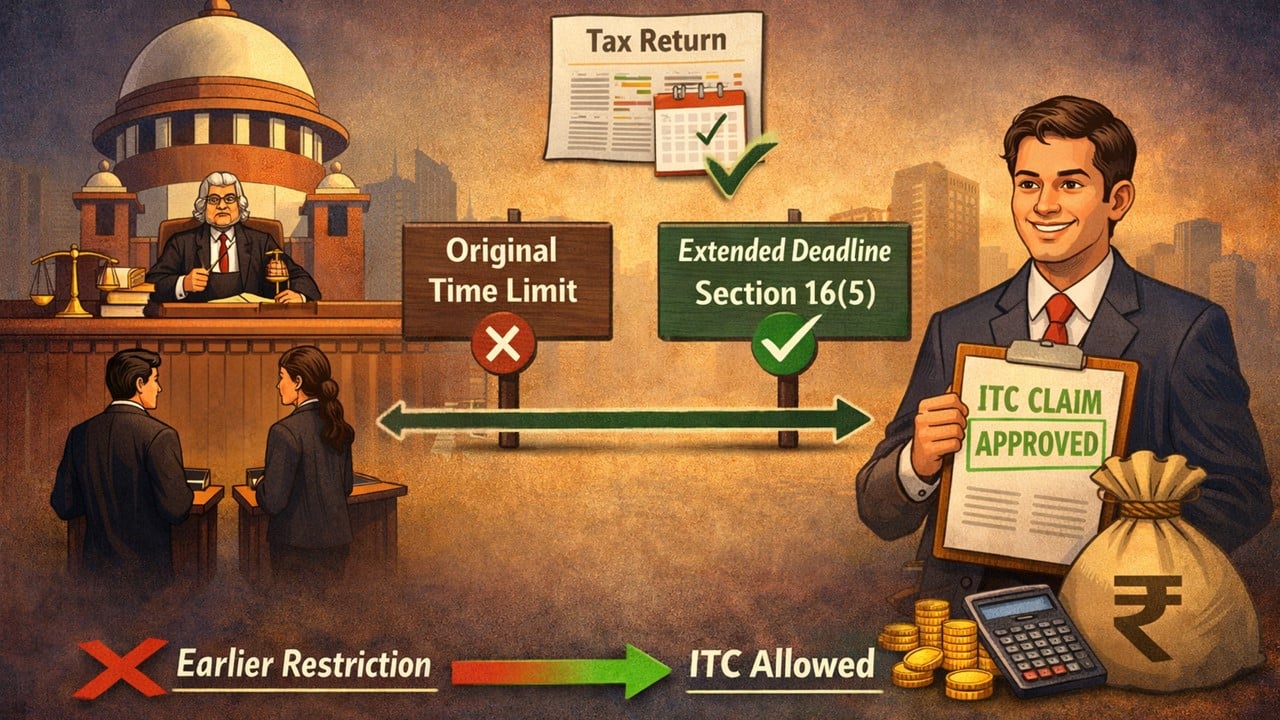

The High Court held that returns filed within the extended deadline under Section 16(5) override the earlier time limit, and allowed the taxpayer to avail ITC.

Case Remanded to Tax Authorities for Fresh Consideration

HC Upholds Taxpayer’s Right to Avail ITC; Holds Extended Deadline Overrides Earlier GST Time Limit

The Kerala High Court has decided on a writ petition filed by Royalbison Autorentals India Private Limited against the State Tax Officer and another authority, challenging an order passed under Section 73 of the CGST Act, denying the Input Tax Credit (ITC) claimed by the petitioner on the grounds that the petitioner failed to furnish its GSTR-3B return for the month of March 2020 within the statutory time limit prescribed under Section 16(4) of the CGST Act for the financial year 2019-20. As per the provisions of income tax, ITC cannot be claimed if returns are filed beyond the specified deadline.

However, the petitioner argued that as per the new provision of Section 16(5), the petitioner was allowed to claim ITC (Input Tax Credit) since the petitioner filed its return for March 2020 on October 24, 2020, which was within the extended deadline mentioned in Section 16(5) of the Act, i.e., November 30, 2021.

The court, when examining the facts of the case, noted that Section 16(5) begins with the words “Notwithstanding anything contained in subsection (4),” meaning it overrides the earlier time limit. Since the return filed by the company was within the allowed time limit as prescribed under Section 16(5), it was entitled to claim ITC.

Accordingly, the court quashed the impugned order denying the ITC and remanded the case back to the tax authorities to reconsider the matter and additionally directed the authority to pass fresh orders within three months after giving the company a proper opportunity for a hearing.

About Author

Saloni Kumari

Content Writer

Saloni is a Content Writer with 2+ years of experience at studycafe.in. She writes legal, taxation, and finance related content including GST, Income Tax etc. Skilled in translating complex judicial pronouncements and regulatory developments into clear, and reader-friendly articles. Experienced in covering judgements of ITAT, High Court, GSTAT, and news related to Income Tax, GST, and corporate law. She can be reached at [email protected].

Saloni is a Content Writer with 2+ years of experience at studycafe.in. She writes legal, taxation, and finance related content including GST, Income Tax etc. Skilled in translating complex judicial pronouncements and regulatory developments into clear, and reader-friendly articles. Experienced in covering judgements of ITAT, High Court, GSTAT, and news related to Income Tax, GST, and corporate law. She can be reached at [email protected].

StudyCafe

StudyCafe Delhi, Delhi, India

Delhi, Delhi, India 2487

2487My Recent Articles

- ITAT Grants Fresh Opportunity to Explain Rs 2.39 Crore Demonetisation Cash Deposit Addition After Main Director’s DeathPremium

- ITAT Grants Taxpayer Fresh Opportunity to Contest Rs 44.16 Lakh Addition After Finding No Decision on MeritsPremium

- Trust’s Sections 12AB and 80G Registration Cannot Be Denied Before Charitable Project Is Completed, Holds ITATPremium

- ITAT Says Identity and Creditworthiness Irrelevant Where Loan Was Directly Paid to Haryana Mining DepartmentPremium

- Earlier Rejection Cannot Be Sole Ground to Reject Fresh Section 12AB and 80G Registration Applications, Says ITATPremium

Up Next

Loading suggestions…

Recent Posts

All Posts

Recent Posts

All Posts