HC: VAT Refund Cannot Be Adjusted Against Settled Dues Under Amnesty Scheme:

High Court disallows refund adjustment against dues settled under Maharashtra Amnesty Scheme 2023.

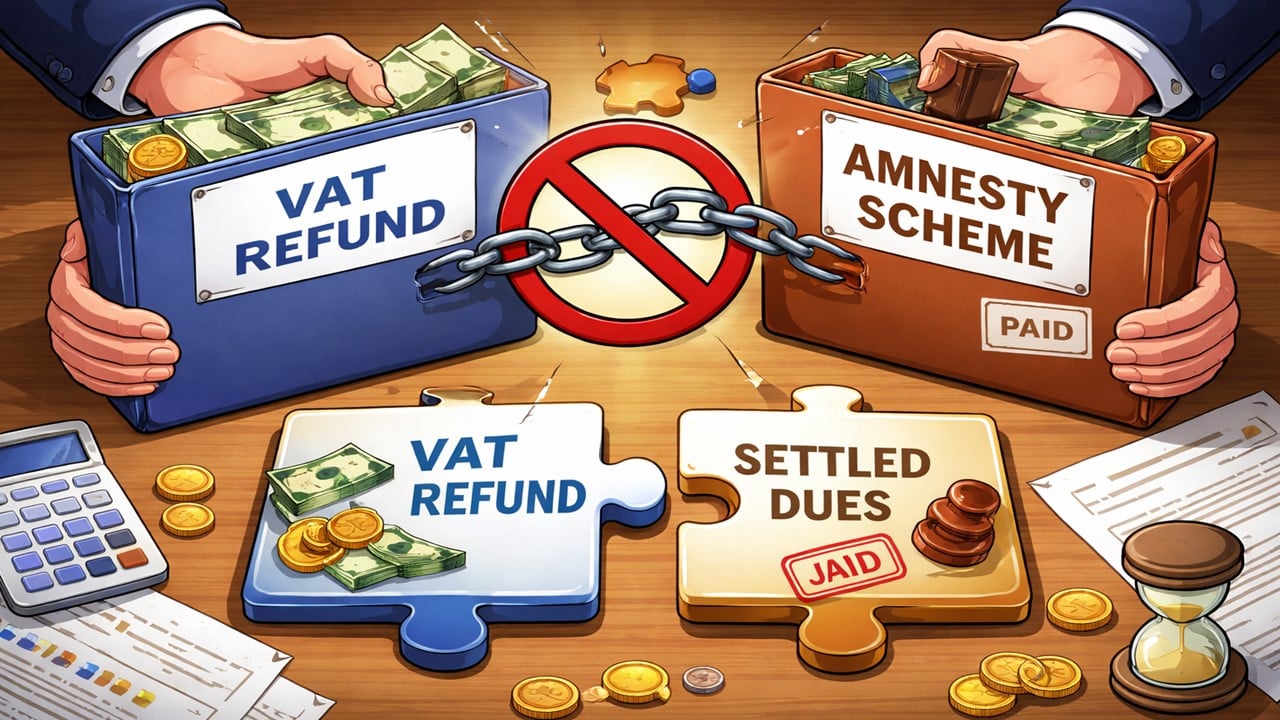

High Court Rules Settlement Scheme Overrides MVAT Refund Adjustment Provisions

For the later years 2008–09 and 2009–10, tax demands were raised, which the petitioner chose to settle under the Maharashtra Settlement of Arrears Act, 2023. It applied under the one-time settlement scheme and paid the required amounts as determined by the department. Despite this, the authorities passed an order adjusting the earlier refund of Rs. 33.29 lakh (relating to 2007–08) against alleged dues of 2008–09.

Feeling aggrieved, the petitioner approached the Bombay High Court, arguing that such adjustment was not only contrary to the scheme of the Settlement Act but was also done without giving any opportunity of being heard.Issue Before Court: Whether refund of one tax period can be adjusted against dues of another while granting settlement benefits.

HC's Ruling: The Court allowed the petition and set aside the settlement order. It held that the Settlement Act is a complete code in itself, meant to bring closure to disputes, and once the taxpayer fulfils its conditions, the benefit cannot be diluted by applying provisions of the MVAT Act. The adjustment of refund under MVAT provisions cannot be imported into settlement proceedings.The Court further noted that the petitioner had already paid the required amount under the scheme and no outstanding dues remained. It also found that the adjustment was made without giving a hearing, violating principles of natural justice. Accordingly, the authorities were directed to grant full settlement benefits and refund Rs. 33.29 lakh along with applicable interest within two weeks.

To Read Full Judgment, Download PDF Given BelowAbout Author

Meetu Kumari

Content Manager

Studycafe

Studycafe Jodhpur, Rajasthan, India

Jodhpur, Rajasthan, India 2264

2264My Recent Articles

- ITAT Condones 302-Day Delay, Restores Salary Assessment for Fresh VerificationPremium

- ITAT Condones Delay After Tax Consultant's Death, Restores Appeals for Fresh HearingPremium

- ITAT Remands Salary Addition, Says Taxability Depends on Salary Becoming Due, Not Mere ReceiptPremium

- ITAT Deletes TP Royalty Adjustment, Orders Fresh Review of Commission BenchmarkingPremium

- ITAT Quashes Reassessment Over Unsigned Section 148 Notice Issued to AssesseePremium

Loading suggestions…

Recent Posts

All Posts

Recent Posts

All Posts