ICAI UDIN Update: Auditor’s Opinion Now Mandatory, Know More:

ICAI's new UDIN rules, effective June 2025, mandate CAs to disclose audit opinions for greater transparency in GST, tax, and assurance audits.

New ICAI UDIN Rule Mandates Audit Opinion Disclosure from June 2025

ICAI UDIN Update: Auditor’s Opinion Now Mandatory, Know More

The Institute of Chartered Accountants of India (ICAI) has introduced the latest update regarding the Unique Document Identification Number (UDIN). A new requirement for all Chartered Accountants (CAs) when they generate a UDIN for certain types of work. The update is to be effective from June 2025 and will apply specifically to two broad categories of professional services:

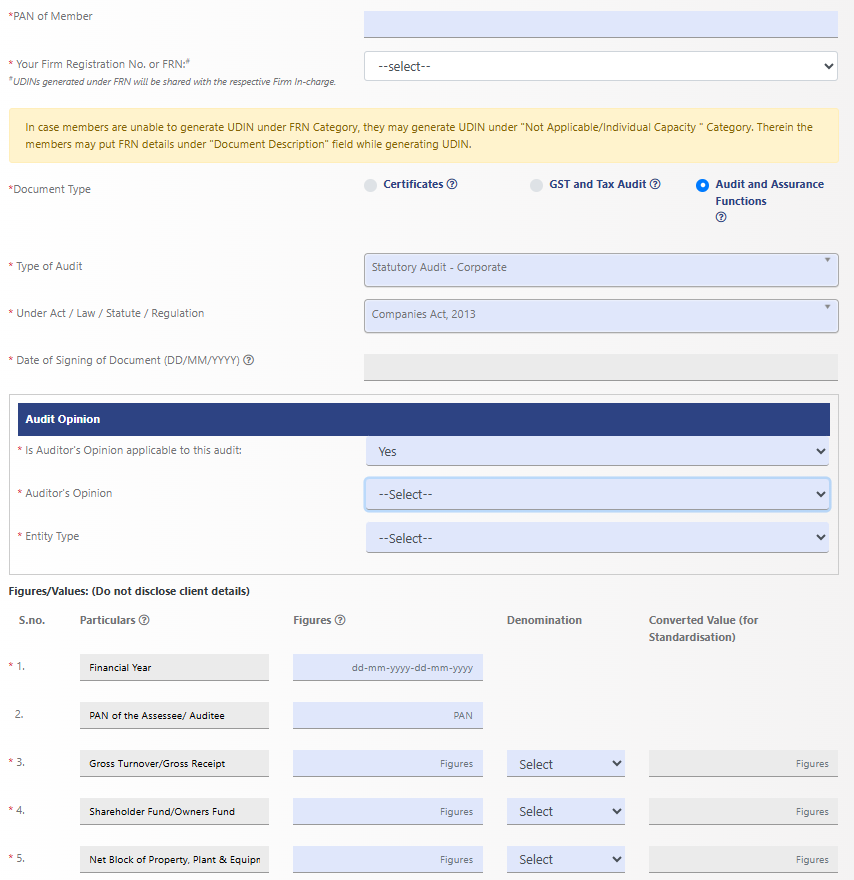

From now on, when a chartered accountant (CA) generates a UDIN for such assignments, they are compelled to share details of their audit opinion. This new update adds another layer in reporting to make things more transparent and help regulators keep a closer eye on what is going on. Chartered Accountants must fill out some additional fields related to the audit report they are signing. Here is exactly what needs to be shared:

From now on, when a chartered accountant (CA) generates a UDIN for such assignments, they are compelled to share details of their audit opinion. This new update adds another layer in reporting to make things more transparent and help regulators keep a closer eye on what is going on. Chartered Accountants must fill out some additional fields related to the audit report they are signing. Here is exactly what needs to be shared:

- GST & Tax Audits

- Audit and Assurance Functions

From now on, when a chartered accountant (CA) generates a UDIN for such assignments, they are compelled to share details of their audit opinion. This new update adds another layer in reporting to make things more transparent and help regulators keep a closer eye on what is going on. Chartered Accountants must fill out some additional fields related to the audit report they are signing. Here is exactly what needs to be shared:

- The CA has to clearly indicate whether the audit opinion is applicable to the engagement. For example: “Yes” if the document contains an auditor's opinion. “No” if it does not (like in certain certifications or reports that are not audit reports).

- If the opinion is applicable, then the CA has to select the type of opinion they have expressed. For example: Unmodified, Modified, Qualified, Adverse, Disclaimer, Key Audit Matter, Emphasis of Matter, and Other Matter. This will facilitate the ICAI to track the nature and frequency of different opinions expressed across the profession.

- The CA also needs to mention whether the entity being audited is listed (i.e., a company listed on a stock exchange) or non-listed (i.e., privately held or unlisted entities).

- If the company or organisation is non-listed, the CA will be asked to provide additional details.

- ICAI has clearly stated that any additional information filled in this process will not be visible to third-party verifiers.

About Author

Saloni Kumari

Content Writer

Saloni is a Content Writer with 2+ years of experience at studycafe.in. She writes legal, taxation, and finance related content including GST, Income Tax etc. Skilled in translating complex judicial pronouncements and regulatory developments into clear, and reader-friendly articles. Experienced in covering judgements of ITAT, High Court, GSTAT, and news related to Income Tax, GST, and corporate law. She can be reached at [email protected].

Saloni is a Content Writer with 2+ years of experience at studycafe.in. She writes legal, taxation, and finance related content including GST, Income Tax etc. Skilled in translating complex judicial pronouncements and regulatory developments into clear, and reader-friendly articles. Experienced in covering judgements of ITAT, High Court, GSTAT, and news related to Income Tax, GST, and corporate law. She can be reached at [email protected].

StudyCafe

StudyCafe Delhi, Delhi, India

Delhi, Delhi, India 2486

2486My Recent Articles

- ITAT Grants Taxpayer Fresh Opportunity to Contest Rs 44.16 Lakh Addition After Finding No Decision on MeritsPremium

- Trust’s Sections 12AB and 80G Registration Cannot Be Denied Before Charitable Project Is Completed, Holds ITATPremium

- ITAT Says Identity and Creditworthiness Irrelevant Where Loan Was Directly Paid to Haryana Mining DepartmentPremium

- Earlier Rejection Cannot Be Sole Ground to Reject Fresh Section 12AB and 80G Registration Applications, Says ITATPremium

- Cash Deposited During Demonetisation Cannot Be Taxed Under Section 69A if Linked to Business, Holds ITAT Premium

Up Next

Loading suggestions…

Recent Posts

All Posts

Recent Posts

All Posts