Income Slabs and deductions under Income Tax applicable for AY 20-21/FY 19-20

Income Slabs and deductions under Income Tax applicable for AY 20-21/FY 19-20 Firstly I would like to congratulate the CA Fraternity that a

Income Slabs and deductions under Income Tax applicable for AY 20-21/FY 19-20

Firstly I would like to congratulate the CA Fraternity that a CA has presented Interim Budget for the year 2019. It is indeed a proud moment for all the Chartered Accountants.

Hona'ble Finance Minister Mr Piyush Goyal presented Interim Budget 2019 on 1st of Feburary 2019. While the Income Tax Slab have been kept unchanged for AY 2020-21, some interesting changes have been proposed in the tax structure which will have an impact on the tax liability of Individuals specially middle class people.

I have made summary of Income Slabs, deductions and Allowance under Income Tax applicable for AY 20-21/FY 19-20 based on Interim Budget Presented by our Hon'able Finance minister.

Kindly note that any change of Income Slabs, deductions or Allowance under Income Tax suggested in this article is based on Interim Finance bill proposed by BJP Government and is subject to it's approval from parliament.

Income Slabs and deductions under Income Tax applicable for AY 20-21/FY 19-20

Slab Rates for FY 19-20 or AY 20-21

Slab rates for FY 19-20 or AY 20-21 for General Public or Individuals below 60 years of Age

|

Tax Slab for Individuals |

Tax Rate |

|---|---|

|

Upto 2,50,000 |

Nil |

|

2,50,000-5,00,000 |

5% |

|

5,00,000-10,00,000 |

20% |

|

Over 10,00,000 |

30% |

Slab Rates for FY 19-20 or AY 20-21 for Senior Citizen who are resident and above 60 and below 80 years of Age

|

Tax Slab for Individuals |

Tax Rate |

|---|---|

|

Upto 3,00,000 |

Nil |

|

3,00,000-5,00,000 |

5% |

|

5,00,000-10,00,000 |

20% |

|

Over 10,00,000 |

30% |

Slab Rates for FY 19-20 or AY 20-21 for Very Senior Citizen who are resident and above 80 years of Age

|

Tax Slab for Individuals |

Tax Rate |

|---|---|

|

Upto 5,00,000 |

Nil |

|

5,00,000-10,00,000 |

20% |

|

Over 10,00,000 |

30% |

*Less : Tax rebate maximum upto Rs. 12500 for Total income upto Rs. 5,00,000

Add : Education + Health Cess of 4%

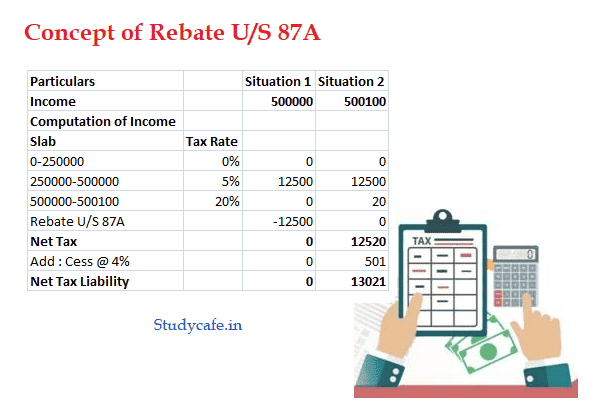

Concept of Rebate U/S 87A

*Let us Understand the Concept of Rebate with a small Example

|

Particulars |

Situation 1 |

Situation 2 |

|

|

Income |

500000 |

500100 |

|

|

Computation of Income |

|

|

|

|

Slab |

Tax Rate |

||

|

0-250000 |

0% |

0 |

0 |

|

250000-500000 |

5% |

12500 |

12500 |

|

500000-500100 |

20% |

0 |

20 |

|

Rebate U/S 87A |

-12500 |

0 |

|

|

Net Tax |

0 |

12520 |

|

|

Add : Cess @ 4% |

0 |

501 |

|

|

Net Tax Liability |

|

0 |

13021 |

It means when total income is upto Rs. 5L, then no tax shall be payable by the assessee. But if total income exceeds Rs. 5L, the same shall be taxed at existing Slab rate.

Income Slabs and deductions under Income Tax applicable for AY 20-21/FY 19-20

Popular Deductions under Income Tax applicable for AY 20-21/FY 19-20

|

Section |

Sources of Investments |

Amount |

|

80C |

Rs. 1,50,000 => LIC / PPF / KVP / EPF / SSY / NSC / HOME LOAN PRINCIPAL / SCHOOL FEES/ ELSS/STAMP DUTY |

Rs. 1,50,000 |

|

80CCD(1B) |

Rs. 50,000 => NPS |

Rs. 50,000 |

|

24 |

Rs. 2,00,000 => Home loan interest |

Rs. 2,00,000 |

|

80DD |

Rs. 75000/125000 => Exp of disabled dependent |

Rs. 75000/125000 |

|

80U |

Rs. 75000/125000 => own Physical Disability |

Rs. 75000/125000 |

|

80TTA |

Rs. 10,000 = > Interest on Savings Account. [Persons other than Senior citizen / Very senior citizen] |

Rs. 10,000 |

|

80TTB |

Rs. 50,000 = > Interest on Savings Account. and Interest on deposits with Post Offices, Banks, Co-operative bank. Only available to senior citizen & Very senior Citizen |

Rs. 50,000 |

|

80G |

Donation ( Only if paid by cheque/ Bank Mode ) |

Upto 50% of Donation or 10% Total income. whichever is higher |

|

80GG |

Deduction for the rent paid (Not available to Individuals who gets HRA from Employment). Least of the following shall be available :- |

|

|

1) Rent paid minus 10 percent the adjusted total income. |

||

|

2) Rs 5,000 per month |

||

|

3) 25 percent of the adjusted total income |

||

|

80D |

Mediclaim For self, spouse and dependent children ( Only if paid by cheque/ Bank Mode ) |

Rs. 25000/50000 |

|

Up to Rs. 25,000 [Rs. 50,000 if person is a senior citizen] |

||

|

80D |

Mediclaim For Parents ( Only if paid by cheque/ Bank Mode ) |

Rs. 25000/50000 |

|

Upto Rs. 25,000 shall be allowed [Rs. 50,000 if person is a senior citizen] |

Deductions under Income Tax applicable for AY 20-21/FY 19-20 specially for Salaried Individuals

|

16(ia) |

Standard Deduction [Rs. 50,000 or the amount of salary, whichever is lower] |

Individual Salaried Employee |

|

16(ii) |

Entertainment allowance [actual or at the rate of 1/5th of salary, whichever is less] [limited to Rs. 5,000] |

Government employees |

|

16(iii) |

Employment tax |

Salaried assessees |

|

10(13A) |

HRA ExemptionLeast of the following is exempt:a) Actual HRA Receivedb) 40% of Salary (50%, if house situated in Mumbai, Calcutta, Delhi or Madras)c) Rent paid minus 10% of salary* Salary= Basic + DA (if part of retirement benefit) + Turnover based CommissionNote:i. Fully Taxable, if HRA is received by an employee who is living in his own house or if he does not pay any rentii. It is mandatory for employee to report PAN of the landlord to the employer if rent paid is more than Rs. 1,00,000 [Circular No. 08 /2013 dated 10th October, 2013]. |

Salaried assessees |

Disclaimer: The entire contents of this document have been prepared on the basis of relevant provisions and as per the information existing at the time of the preparation. Although care has been taken to ensure the accuracy, completeness and reliability of the information provided, I assume no responsibility therefore. Users of this information are expected to refer to the relevant existing provisions of applicable Laws. The user of the information agrees that the information is not a professional advice and is subject to change without notice. I assume no responsibility for the consequences of use of such information. In no event shall I shall be liable for any direct, indirect, special or incidental damage resulting from, arising out of or in connection with the use of the information.

About Author

CA Deepak Gupta

Co Founder

StudyCafe

StudyCafe Delhi, Delhi, India

Delhi, Delhi, India 3423

3423My Recent Articles

- UltraTech Cement slapped with Rs. 808.78 Cr Income Tax Demand

- GST: High Court upheld constitutional validity of Section 16(2)(c), asks government to address ITC issues of genuine purchasers

- Old vs New Tax Regime for Tax Year 2026-27

- High court criticizes Income Tax Department for not releasing ITR Utilities despite 11 years of directions

- Fino Payments Bank CEO Rishi Gupta Gets Bail in GST Case, Bank Clarifies No Direct Link

Loading suggestions…

Recent Posts

All Posts

Tags

No tags yet.

Recent Posts

All Posts

Tags

No tags yet.