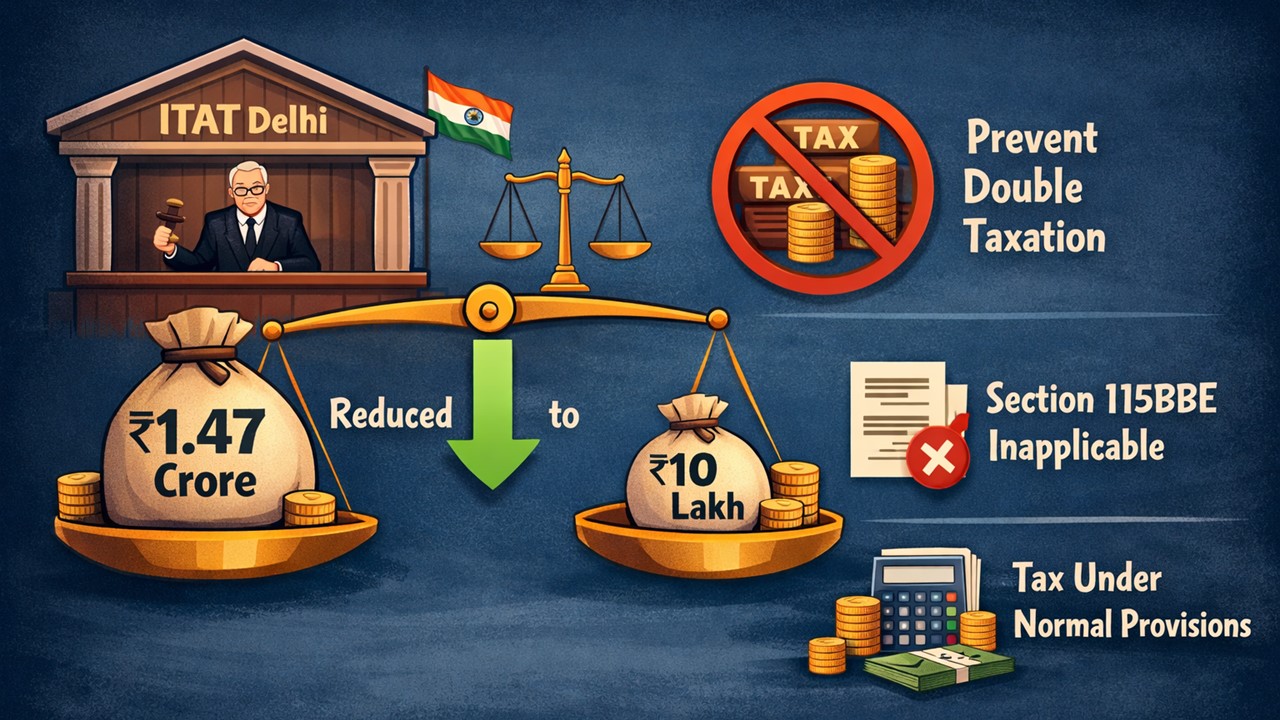

ITAT Curbs Rs 1.47 Cr Addition to Rs 10 Lakh, Rejects 115BBE Applicability to Avoid Double Taxation:

The ITAT reduced a Rs 1.47 crore addition to Rs 10 lakh to prevent double taxation and held that Section 115BBE was inapplicable, directing taxation under normal provisions.

ITAT Delhi Limits Addition to Rs 10 Lakh

ITAT Curbs Rs 1.47 Cr Addition to Rs 10 Lakh, Rejects 115BBE Applicability to Avoid Double Taxation

ITAT Delhi held that, even though the assessee failed to fully prove transactions with a suspicious party, taxing the entire Rs 1.47 crore would cause double taxation. It restricted the addition to Rs 10 lakh and ruled Section 115BBE inapplicable, taxing income under normal provisions.

The key issue involved an addition of Rs 1.47 crore made on the assessee's income on the grounds of unexplained credit from a trading firm, Kangna Agro Product, under Section 68 of the Income Tax Act. The said company was found to be fake by the tax authorities during a survey.

When the aggrieved assessee filed an appeal before the Commissioner of Income Tax (Appeals) [CIT(A)], the impugned addition of Rs 1.47 crore was sustained. Thereafter, the assessee filed the present appeal before the ITAT Delhi.

When the tribunal analysed the entire case, it noted that the assessee had submitted all the relevant documents, like VAT returns, a copy of Form C, a stock register, Bank Statement, etc., proving that the entire credits in question belonged to M/s Kangna Agro Products only and were the cash sales made to the said company.

After reviewing all the submitted evidence, the tribunal observed that the assessee had made enough and reasonable efforts to prove the impugned transaction. However, the explanation cannot be fully considered valid, since during the survey conducted by the tax authority, the company in question was found to be suspicious.

Simultaneously, the Tribunal noted that taxing the entire amount would result in double taxation, as the sales were already recorded in the books. Further, the VAT return of the said entity cannot be dismissed at hand without solid reasons. As a result, the tribunal decided to reduce the impugned addition amount to Rs 10 lakh. It noted that it was relevant to address the possible discrepancies in the present matter.

Moreover, on the issue concerning taxation under Section 115BBE, the tribunal held that the higher tax rate would not apply, as the provision was effective only for transactions after April 1, 2017. Accordingly, the tax authorities have been directed to tax the addition under normal provisions of tax and not under the provisions of 115BBE. With these directions, the appeal was partly allowed.

About Author

Saloni Kumari

Content Writer

Saloni is a Content Writer with 2+ years of experience at studycafe.in. She writes legal, taxation, and finance related content including GST, Income Tax etc. Skilled in translating complex judicial pronouncements and regulatory developments into clear, and reader-friendly articles. Experienced in covering judgements of ITAT, High Court, GSTAT, and news related to Income Tax, GST, and corporate law. She can be reached at [email protected].

Saloni is a Content Writer with 2+ years of experience at studycafe.in. She writes legal, taxation, and finance related content including GST, Income Tax etc. Skilled in translating complex judicial pronouncements and regulatory developments into clear, and reader-friendly articles. Experienced in covering judgements of ITAT, High Court, GSTAT, and news related to Income Tax, GST, and corporate law. She can be reached at [email protected].

StudyCafe

StudyCafe Delhi, Delhi, India

Delhi, Delhi, India 2484

2484My Recent Articles

- ITAT Says Identity and Creditworthiness Irrelevant Where Loan Was Directly Paid to Haryana Mining DepartmentPremium

- Earlier Rejection Cannot Be Sole Ground to Reject Fresh Section 12AB and 80G Registration Applications, Says ITATPremium

- Cash Deposited During Demonetisation Cannot Be Taxed Under Section 69A if Linked to Business, Holds ITAT Premium

- ITAT Condones 1,731-Day Delay, Remands Cancer Trust's Section 12A Registration Application for Fresh ConsiderationPremium

- ITAT Lowers Estimated Profit Rate from 8% to 4% After Considering State Shutdown and Medicine Trade MarginsPremium

Up Next

Loading suggestions…

Recent Posts

All Posts

Recent Posts

All Posts