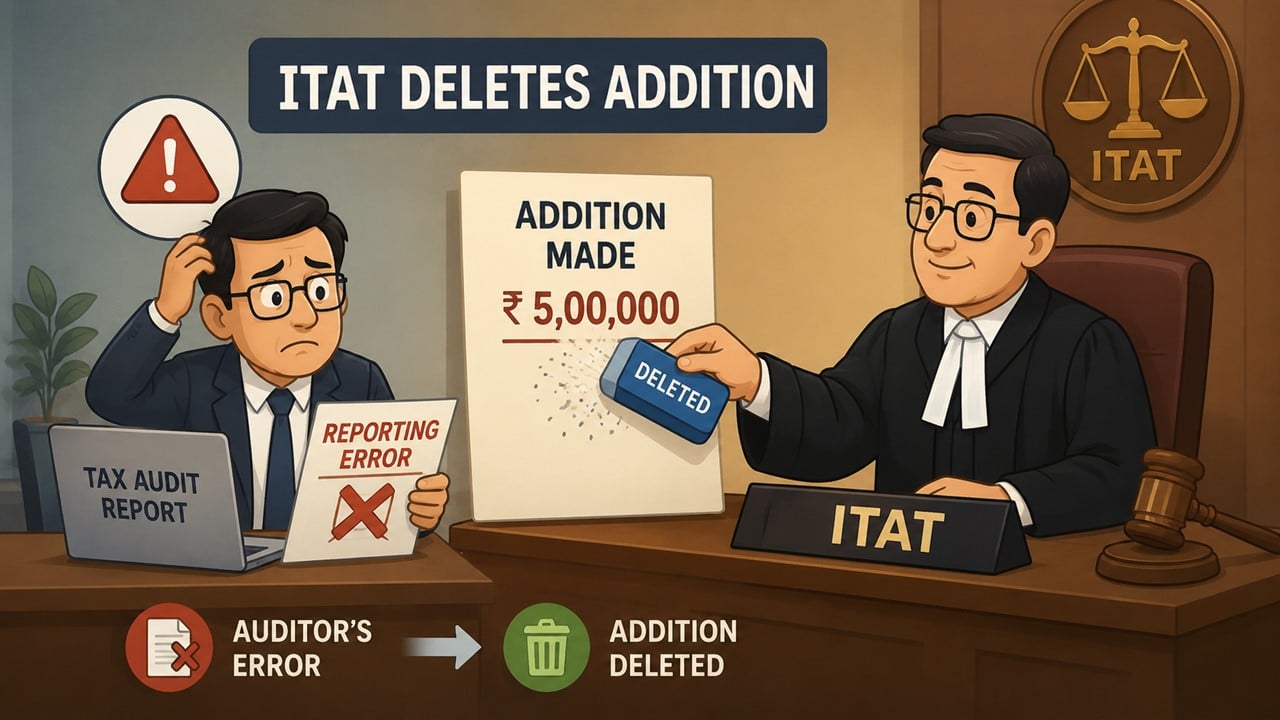

ITAT Deletes Addition Arising from Auditor’s Reporting Error in Tax Audit Report:

ITAT deleted a Rs 13.01 lakh addition made solely due to an auditor’s erroneous reporting in Form 3CD, holding that taxing already-disclosed income again would amount to double taxation.

ITAT Quashes Addition Based on Audit Report Mistake

Table of Contents

ITAT Deletes Addition Arising from Auditor’s Reporting Error in Tax Audit Report

The Mumbai Bench of the Income Tax Appellate Tribunal (ITAT) provided relief to taxpayer Hiloni Partosh Kapasi by deleting an addition that had been made during the processing of her income tax return for Assessment Year 2022-23.

Background of the case

The taxpayer had earned income from three sources: futures & Options (F&O) trading, Capital gains and Income from other sources, such as interest and dividends. Since the F&O transactions were treated as business activities, the accounts were subjected to a tax audit, and Form 3CD was filed along with the return of income. During the audit, the auditor mistakenly reported several items under Clause 16(d) of Form 3CD. The purpose of including this clause is to disclose income that should have been brought into account in the Profit and Loss Account. The reported amounts were long-term capital gains, short-term capital gains, savings bank interest, interest on RBI bonds, interest on fixed deposits and dividend income of Rs. 13,01,040. Based on this reporting, the Central Processing Centre (CPC) stated that the addition was made in the hands of the assessee. Being aggrieved by the order of the CPC, the assessee approached the CIT(A). The CIT(A) did not accept the taxpayer's explanation and upheld the adjustment, observing that the taxpayer had not sufficiently established that the audit report contained a clerical error. The assessee then approached the ITAT. To support the claim, the taxpayer produced a certificate from the auditor admitting that the reporting under Clause 16(d) was a mistake. The auditor clarified that no amount was actually required to be reported under that clause and that the correct disclosure should have been "Nil". The Tribunal also noted that the auditor had wrongly reported the figures under Clause 16(d) and that such reporting was contrary to the guidance provided for tax audits. The ITAT observed that the addition of Rs.13,01,038 was made merely based on an incorrect entry in the tax audit report, and the taxation of the same income again will amount to double taxation. There was no reason to make a separate addition, as the income was already disclosed and assessed under the relevant heads. Thus, the Tribunal deleted the entire addition and allowed the appeal of the taxpayer.

About Author

Vanshika verma

Content Writer

Vanshika Verma is a Content Writer with 1+ year of experience at Studycafe.in. A B.Com graduate from Delhi University, She writes articles on Finance, Tax, ICAI, GST, and the latest financial news, with a focus on making complex topics easy for readers and professionals.

Vanshika Verma is a Content Writer with 1+ year of experience at Studycafe.in. A B.Com graduate from Delhi University, She writes articles on Finance, Tax, ICAI, GST, and the latest financial news, with a focus on making complex topics easy for readers and professionals.

Studycafe

Studycafe Delhi, Delhi, India

Delhi, Delhi, India 1575

1575My Recent Articles

- ITAT Directs Grant of Full Section 87A Rebate, Rejects CPC's Restricted ComputationPremium

- ITAT Quashes Reassessment Based on Unverified Insight Portal InformationPremium

- ITAT Sets Aside Rs 3.61 Crore Tax Addition Over Violation of Natural JusticePremium

- ITAT Upholds Rs 16.5 Lakh Addition Under Section 69C Over Bogus Purchase ClaimPremium

- ITAT: Gross Profit Cannot Be Estimated Without Rejecting Books of AccountPremium

Up Next

Loading suggestions…

Recent Posts

All Posts

Tags

Recent Posts

All Posts