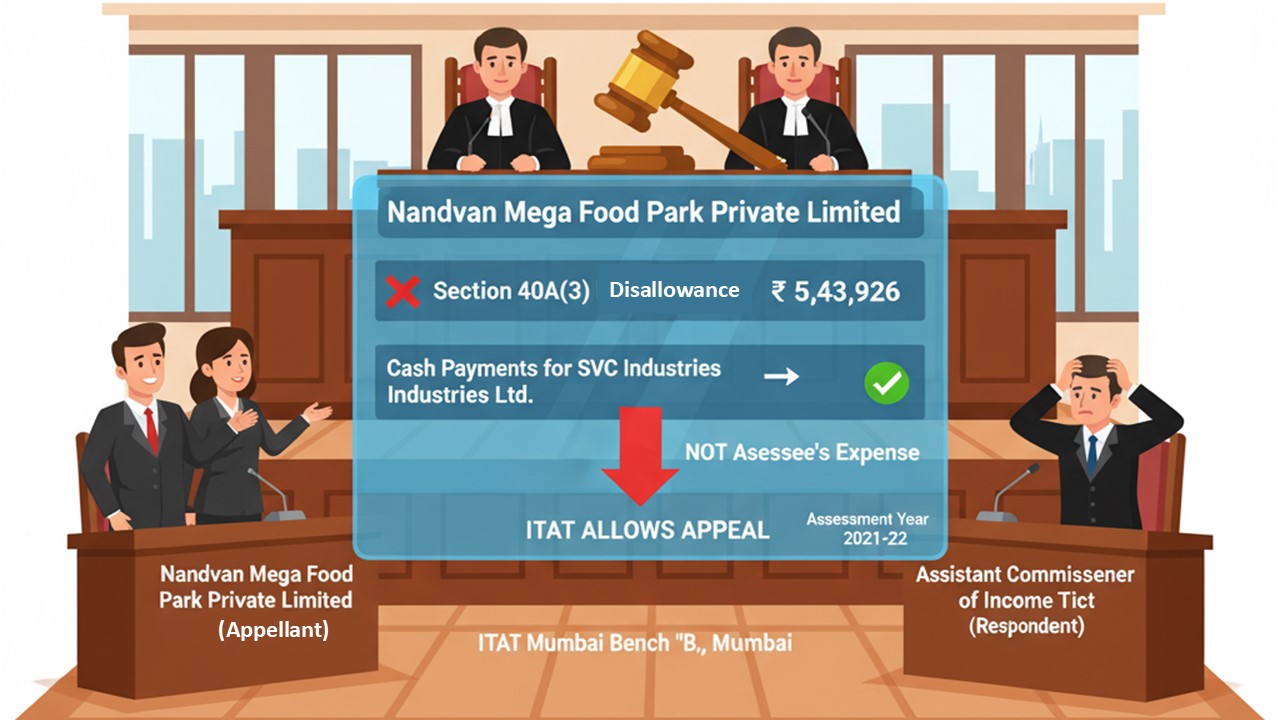

ITAT Deletes Disallowance Under Section 40A(3) for Cash Payments Made on Behalf of Third Party:

ITAT Mumbai ruled that cash payments made on behalf of another company cannot be disallowed under Section 40A(3), deleting the Rs. 5.43 lakh addition.

Tribunal Holds Section 40A(3) Not Applicable Since Payments Were Not Assessee’s Own Expenses

ITAT Deletes Disallowance Under Section 40A(3) for Cash Payments Made on Behalf of Third Party

The assessing officer (AO) recently made a disallowance on a company of Rs. 543,926 under section 40A(3). The ITAT ruled that since the cash payments were made for another company and were not claimed as the assessee’s own business expenses, Section 40A(3) did not apply. Hence, the addition made by the tax officer was dismissed.

The present appeal has been filed by a company named Nandvan Mega Food Park Private Limited (Appellant) against the Assistant Commissioner of Income Tax, Central Circle - 6(2) (Respondent) in the Income Tax Appellate Tribunal (ITAT) “B” Bench, Mumbai, before Shri Vikram Singh Yadav (Accountant Member) and Shri Sandeep Singh Karhail (Judicial Member). The case is related to the assessment year 2021-22.

The appeal has been filed challenging an order dated 29.03.2025, issued under section 250 of the Income Tax Act, 1961, by the learnt Commissioner of Income Tax (Appeals) [CIT(A)]. When the hearing was scheduled on this case, no one attended the hearing in person and no application was even furnished seeking any postponement or adjournment. Also, the notice sent to the assessee informing them of the scheduled date of the hearing via registered post was returned unserved. Therefore, the present case has been decided by only hearing one side, i.e., the learnt Departmental Representative (DR), not the assessee, meaning the present order is an ex parte order.

Background of Case:

The company is involved in the business of manufacturing, trading, and deemed manufacturing, including the processing of agro-based products, including packing or non-packing. A search and seizure operation under Section 132 of the Income Tax Act was carried out in the case of M/s Overseas Infrastructure Alliance (India) Private Limited. Following this, a notice under Section 148 was issued to the assessee on March 09, 2023.

In response to this notice, on May 05, 2023, the assessee filed its income tax return (ITR), declaring a total loss of Rs. 45,65,949. Thereafter, the assessee was issued statutory notices under section 143(2) and section 142(1) of the Act for further assessment.

During the review of records, the Assessing Officer (AO) noticed from the books of M/s SVC Industries Ltd. that the assessee had made cash payments exceeding Rs. 10,000 per day, totalling Rs. 543,926 during the year. The AO asked the assessee to explain why these payments should not be disallowed under Section 40A(3), which restricts large cash payments.

Since the AO was not satisfied with the explanation given by the assessee, the AO added Rs. 543,926 to the assessee’s income under Section 40A(3).

CIT(A)'s Decision:

Assessee dissatisfied with the action of the assessing officer (AO), then filed an appeal before the Commissioner of Income Tax (Appeals) [CIT(A)]; however, the CIT(A) endorsed the arguments served by the assessing officer and dismissed the appeal vide the present impugned order dated 29.03.2025.

ITAT Mumbai's Decision:

Thereafter, the assessee filed an appeal challenging the CIT(A)'s order by the Commissioner of Income Tax (Appeals) [CIT(A)] confirming a disallowance of Rs. 543,926 under Section 40A(3) of the Income Tax Act. This section disallows cash payments exceeding Rs. 10,000 made for business expenses.

The ITAT noted the following:

- The AO had based the disallowance only on the ledger entries between the two companies.

- The payments were shown to be made for SVC Industries Ltd, not for Nandvan Mega Food Park Private Limited.

- These payments were also not claimed as expenses by Nandvan Mega Food Park in its books.

- Therefore, the tribunal said no disallowance can be made in Nandvan’s hands under Section 40A(3) because the expenses did not belong to it.

- In the final decision, the tribunal deleted the disallowance of Rs. 5,43,926 made by the assessing officer (AO) and allowed the appeal filed by the assessee.

About Author

Saloni Kumari

Content Writer

Saloni is a Content Writer with 2+ years of experience at studycafe.in. She writes legal, taxation, and finance related content including GST, Income Tax etc. Skilled in translating complex judicial pronouncements and regulatory developments into clear, and reader-friendly articles. Experienced in covering judgements of ITAT, High Court, GSTAT, and news related to Income Tax, GST, and corporate law. She can be reached at [email protected].

Saloni is a Content Writer with 2+ years of experience at studycafe.in. She writes legal, taxation, and finance related content including GST, Income Tax etc. Skilled in translating complex judicial pronouncements and regulatory developments into clear, and reader-friendly articles. Experienced in covering judgements of ITAT, High Court, GSTAT, and news related to Income Tax, GST, and corporate law. She can be reached at [email protected].

StudyCafe

StudyCafe Delhi, Delhi, India

Delhi, Delhi, India 2489

2489My Recent Articles

- ITAT Rules in Taxpayer's Favour, Holds Delay in Filing Form 67 Cannot Be Sole Ground to Deny Foreign Tax CreditPremium

- ITAT Revives Tax Appeals for Six AYs After Finding Insufficient Hearing Time and Ignored Adjournment RequestPremium

- ITAT Grants Fresh Opportunity to Explain Rs 2.39 Crore Demonetisation Cash Deposit Addition After Main Director’s DeathPremium

- ITAT Grants Taxpayer Fresh Opportunity to Contest Rs 44.16 Lakh Addition After Finding No Decision on MeritsPremium

- Trust’s Sections 12AB and 80G Registration Cannot Be Denied Before Charitable Project Is Completed, Holds ITATPremium

Up Next

Loading suggestions…

Recent Posts

All Posts

Recent Posts

All Posts