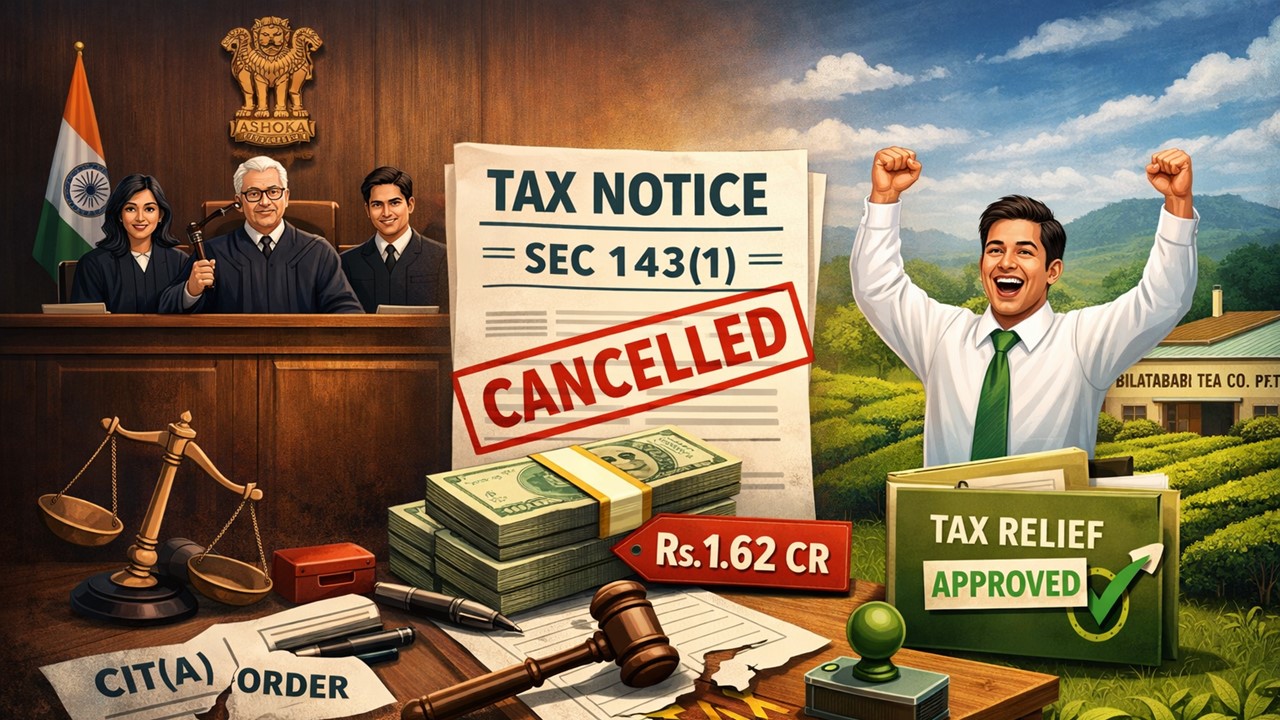

ITAT Quashes Rs. 1.62 Crore Adjustment Made Without Giving Proper Reason or Issuance of Notice:

ITAT held that the Rs. 1.62 crore adjustment made under Section 143(1) without reasons or notice was illegal and deleted the addition, fully allowing the company’s appeal.

Tribunal Gives Full Relief to Assessee Company; Sets Aside CIT(A)'s Order

ITAT Quashes Rs. 1.62 Crore Adjustment Made Without Giving Proper Reason or Issuance of Notice

ITAT Kolkata ruled that the tax authorities had wrongly made a Rs. 1.62 crore adjustment under Section 143(1) without giving reasons and without issuing a notice. The tribunal set aside the order in question and deleted the addition. Fully allowed the appeal of the company.

A company named Bilatibari Tea Company Private Limited has filed the current appeal before the ITAT Kolkata, challenging an order dated March 05, 2025, passed by the NFAC/CIT(A) under section 250 of the Income-tax Act, 1961. The impugned order had disallowed the assessee's amount of Rs. 1.62 crore from the reported income through making an adjustment under Section 143(1)(a)(ii).

The company filed its income tax return (ITR) for the assessment year 2013-14, declaring total income at Rs. 38,74,130. During return processing, the Assessing Officer (AO) assessed the total income of the company at Rs. 2.01 crore by making an adjustment of Rs. 1.62 crore in the return.

The dissatisfied company filed an appeal before the CIT(A). The CIT(A) partially allowed the appeal by restoring the appeal and sending the case back to the Assessing Officer (AO) for fresh consideration. Directed the AO to re-verify the claims made by the assessee company in its ITR.

Dissatisfied with the action of the CIT(A), the assessee company filed an appeal before the ITAT Kolkata. After hearing both sides and checking the records, the Tribunal found that the Assessing Officer/CPC wrongly increased the assessee’s income while processing the return under Section 143(1). There was no calculation mistake and no wrong claim in the return filed by the assessee.

The AO/CPC made adjustments without giving reasons and without issuing a notice under Section 143(2), which is beyond their authority. Since the income was correctly calculated and expenses and depreciation were properly claimed, the adjustment made under Section 143(1)(a) is not valid in law.

Therefore, in conclusion, the tribunal set aside the impugned order of the CIT(A) and deleted the addition made by the AO. Allowed the appeal of the assessee in full.

About Author

Saloni Kumari

Content Writer

Saloni is a Content Writer with 2+ years of experience at studycafe.in. She writes legal, taxation, and finance related content including GST, Income Tax etc. Skilled in translating complex judicial pronouncements and regulatory developments into clear, and reader-friendly articles. Experienced in covering judgements of ITAT, High Court, GSTAT, and news related to Income Tax, GST, and corporate law. She can be reached at [email protected].

Saloni is a Content Writer with 2+ years of experience at studycafe.in. She writes legal, taxation, and finance related content including GST, Income Tax etc. Skilled in translating complex judicial pronouncements and regulatory developments into clear, and reader-friendly articles. Experienced in covering judgements of ITAT, High Court, GSTAT, and news related to Income Tax, GST, and corporate law. She can be reached at [email protected].

StudyCafe

StudyCafe Delhi, Delhi, India

Delhi, Delhi, India 2503

2503My Recent Articles

- Who Needs to File ITR by July 31? Check Eligibility, Due Dates, and Extension Update

- ITR Filing Deadline 2026: July 31 or August 31? Know Who Can File Income Tax Return by Which Date

- ITAT Sets Aside Ex Parte Assessment, Orders Fresh Hearing With Notices on Both Departmental and Form 36 Email IDsPremium

- CBDT Issues Guidance Note on Crypto-Asset Reporting Under Income Tax Act, 2025

- IITian Earning Rs 1 Crore Borrowed Rs 15,000 to Pay Tax Before ITR Deadline, CA's Viral Post Sparks Financial Literacy Debate

Up Next

Loading suggestions…

Recent Posts

All Posts

Tags

Recent Posts

All Posts