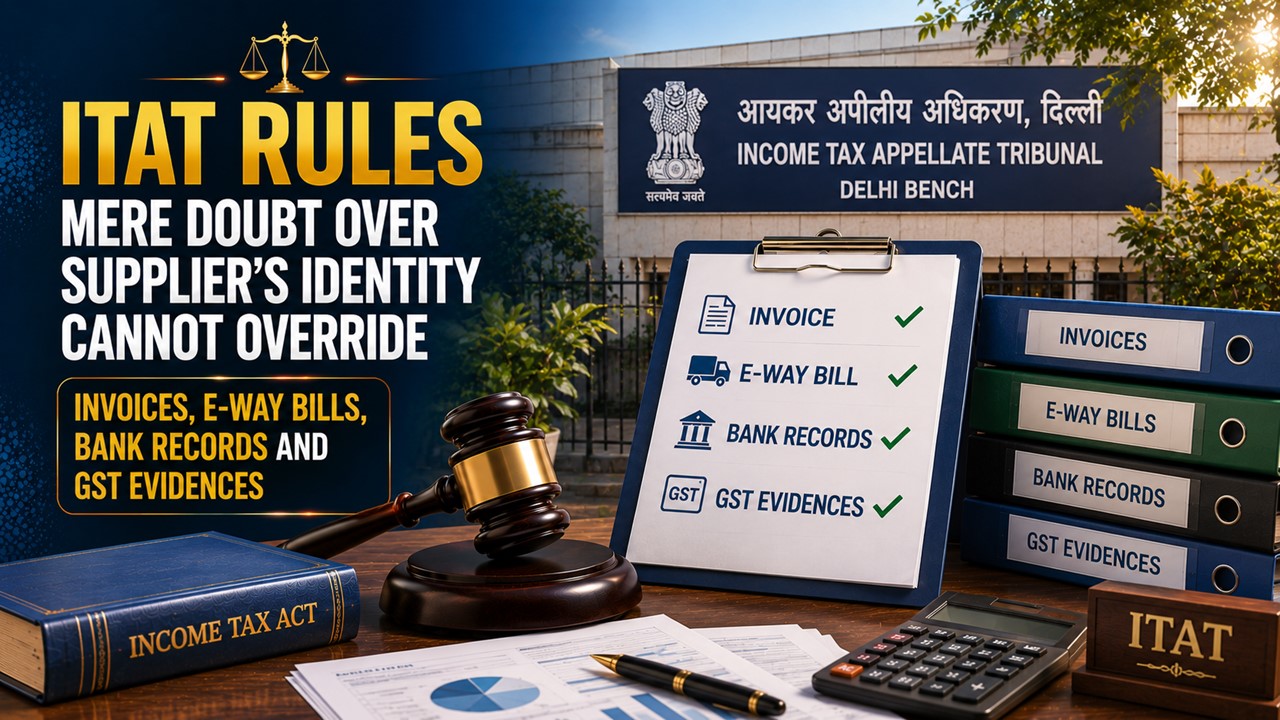

ITAT Restores 12AB and 80G to Trust After Finding No Commercial Activity:

Tribunal finds rejection based on isolated trust deed clauses unsustainable; remands for de novo decision

Dominant Purpose Test Prevails: ITAT Backs Charitable Trust’s Claim

ITAT Restores 12AB and 80G to Trust After Finding No Commercial Activity

Registered under the Gujarat Public Trusts Act, 1950, the assessee is involved in educational and charitable activities. The Trust received provisional registration under Section 12AB of the Income-tax Act on 24.03.2023. Later, on 03.01.2024, it applied for regular registration under Section 12A(1)(ac)(iii) and approval under Section 80G(5)(iii) through Form 10AB. However, both applications were rejected by the CIT (E). The CIT(E) cited Object Nos. 4 and 7 of the trust deed, which mentioned development projects such as roads and drainage, as well as the implementation of government programs, believing they were commercial in nature. The Section 80G application was rejected solely due to the denial of registration under Section 12AB.

Issue Raised: Whether the rejection of registration under Section 12AB and consequent denial of approval under Section 80G can be sustained when based only on a selective reading of certain object clauses in the trust deed, without any finding of actual commercial activity or misuse of funds.

ITAT's Decision: The Hon'ble ITAT set aside both impugned orders passed by the CIT(E) and remanded the matters back for fresh consideration. The Tribunal held that the CIT(E) erred in rejecting the applications merely based on two object clauses without examining the trust deed as a whole or verifying if any activity under those clauses had actually been undertaken. It noted that the conclusion of possible commercial activity was speculative and that there was no evidence of a relationship between the financial statements and the objected clauses. The tribunal stressed that concerns about potential future misuse cannot be grounds for denying registration under Section 12AB; if they do, they may be considered during Section 13 assessment.

The tribunal restored both applications to the CIT(E) to examine the submissions afresh, avoid premature conclusions, and provide a reasonable opportunity of hearing to the assessee.

To Read Full Order, Download PDF Given Below

About Author

Meetu Kumari

Content Manager

Meetu Kumari is an Experienced Advocate and Content Writer with 4+ years of demonstrated history of working in the law practice industry. Skilled in Developing Content, Researching, and Drafting. Strong professional with a Bachelor of Science (B.Sc.) focused on Law from Gujarat National Law University.

Meetu Kumari is an Experienced Advocate and Content Writer with 4+ years of demonstrated history of working in the law practice industry. Skilled in Developing Content, Researching, and Drafting. Strong professional with a Bachelor of Science (B.Sc.) focused on Law from Gujarat National Law University.

Studycafe

Studycafe Jodhpur, Rajasthan, India

Jodhpur, Rajasthan, India 2234

2234My Recent Articles

- HC Sets Aside GST Registration Revocation Rejection Over Procedural Lapse.Premium

- ITAT Upholds Deletion of Bogus Purchase Additions Lacking Search EvidencePremium

- High Court Refuses GST Writ, Directs Appeal Against Fake ITC DemandPremium

- ITAT Restricts Bogus Purchase Addition to 1.15% Profit Element Despite Seller DenialsPremium

- ITAT Upholds Reassessment, Rejects Challenge Over Absence of Section 143(2) NoticePremium

Up Next

Loading suggestions…

Recent Posts

All Posts

Recent Posts

All Posts