MCA Breaking: Definition of "Small Company" Revised; New Limits Starting December 1:

Under the new rules effective from December 1, 2025, the limits for paid-up capital and turnover have been increased to Rs 10 crore and Rs 100 crore, respectively.

MCA Revises Definition of Small Company

MCA Breaking: Definition of "Small Company" Revised; New Limits Starting December 1

The Ministry of Corporate Affairs (MCA) has recently issued a notification dated December 1, 2025, revising the criteria for the definition of "Small Company" under the Companies Act. Starting from December 2025, the limits on paid-up capital and turnover for small companies have been increased. The change aims to reduce the compliance burden on small companies.

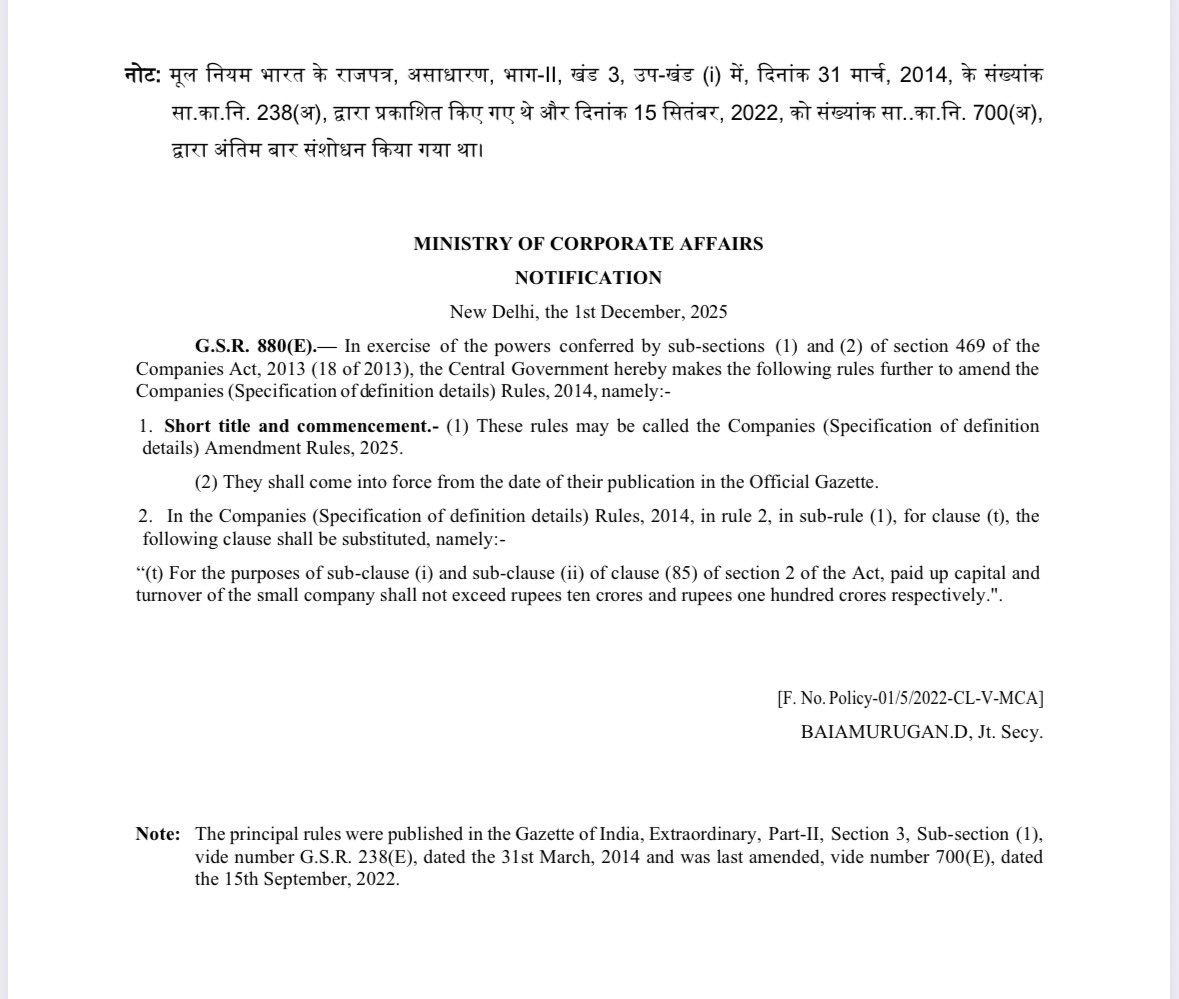

As per the notification, "(t) For the purposes of sub-clause (i) and sub-clause (ii) of clause (85) of section 2 of the Act, paid up capital and turnover of the small company shall not exceed rupees ten crores and rupees one hundred crores respectively."

What Has Changed?

Previously, the paid-up capital for the small companies under the Companies Act was Rs 4 crore, and the turnover limit was Rs 40 Crore. Under the new rules effective from December 1, 2025, the limits for paid-up capital and turnover have been increased to Rs 10 crore and Rs 100 crore, respectively.

This means that to fall under the definition of "small company", the companies must have a Paid-up capital of Rs 10 crore and a Turnover limit of Rs 100 crore. This will allow more companies to be classified as small companies. However, it must be noted that public companies, holding/subsidiary companies, Section 8 companies, and those covered under special acts are not included in this revision.

Small Companies Vs Other Companies

Small companies have several benefits compared to other types of companies. Here is the comparison:

What Has Changed?

Previously, the paid-up capital for the small companies under the Companies Act was Rs 4 crore, and the turnover limit was Rs 40 Crore. Under the new rules effective from December 1, 2025, the limits for paid-up capital and turnover have been increased to Rs 10 crore and Rs 100 crore, respectively.

This means that to fall under the definition of "small company", the companies must have a Paid-up capital of Rs 10 crore and a Turnover limit of Rs 100 crore. This will allow more companies to be classified as small companies. However, it must be noted that public companies, holding/subsidiary companies, Section 8 companies, and those covered under special acts are not included in this revision.

Small Companies Vs Other Companies

Small companies have several benefits compared to other types of companies. Here is the comparison:

What Has Changed?

Previously, the paid-up capital for the small companies under the Companies Act was Rs 4 crore, and the turnover limit was Rs 40 Crore. Under the new rules effective from December 1, 2025, the limits for paid-up capital and turnover have been increased to Rs 10 crore and Rs 100 crore, respectively.

This means that to fall under the definition of "small company", the companies must have a Paid-up capital of Rs 10 crore and a Turnover limit of Rs 100 crore. This will allow more companies to be classified as small companies. However, it must be noted that public companies, holding/subsidiary companies, Section 8 companies, and those covered under special acts are not included in this revision.

Small Companies Vs Other Companies

Small companies have several benefits compared to other types of companies. Here is the comparison:

- Board Meetings: Small companies only need to schedule 2 board meetings a year, with at least a 90-day gap in between. Other companies must hold 4 board meetings a year, with not more than 120 days' gap between them.

- Company Secretary Certification: The small companies are not required to file the CS certification in the annual return form MGT-7, while other companies must comply with this requirement.

- Rotation of Auditors: Small companies are not required to change auditors after a certain period, but other companies must rotate their auditors.

- CARO (Company Auditor's Report Order): CARO is the set of mandatory reporting requirements for auditors. Small companies do not need to follow CARO rules, but other companies must follow these rules.

- Dematerialisation of Shares: Small companies are not required to convert their shares into dematerialised form, while other companies must do it.

About Author

Nidhi

Content Writer

Nidhi is a skilled content writer specializing in personal finance. She creates clear, engaging articles on mutual funds, investments, insurance, and wealth-building strategies. With a passion for simplifying complex financial topics, Nidhi helps readers make informed money decisions with confidence. She can be reached at [email protected]

Nidhi is a skilled content writer specializing in personal finance. She creates clear, engaging articles on mutual funds, investments, insurance, and wealth-building strategies. With a passion for simplifying complex financial topics, Nidhi helps readers make informed money decisions with confidence. She can be reached at [email protected]

Studycafe

Studycafe New Delhi, Delhi, India

New Delhi, Delhi, India 1832

1832My Recent Articles

- Karnataka High Court Gives Another Chance in GST Matter Due to Lack of Hearing

- Delay Should Be Condoned if Explanation is Unrefuted: ITAT

- Non-Service of Income Tax Notice, Ill health of taxpayer, ITAT condones Appeal filing delay

- Books of Accounts Cannot be Rejected Without Any Specific Defect: ITAT Kolkata

- Karnataka High Court Sends ITC Matter Back to GST Authorities for Reconsideration

Up Next

Loading suggestions…

Recent Posts

All Posts

Tags

Recent Posts

All Posts