TDS on Purchase & TCS on Sale explained with charts and Tally Entry

Understanding Compliance:

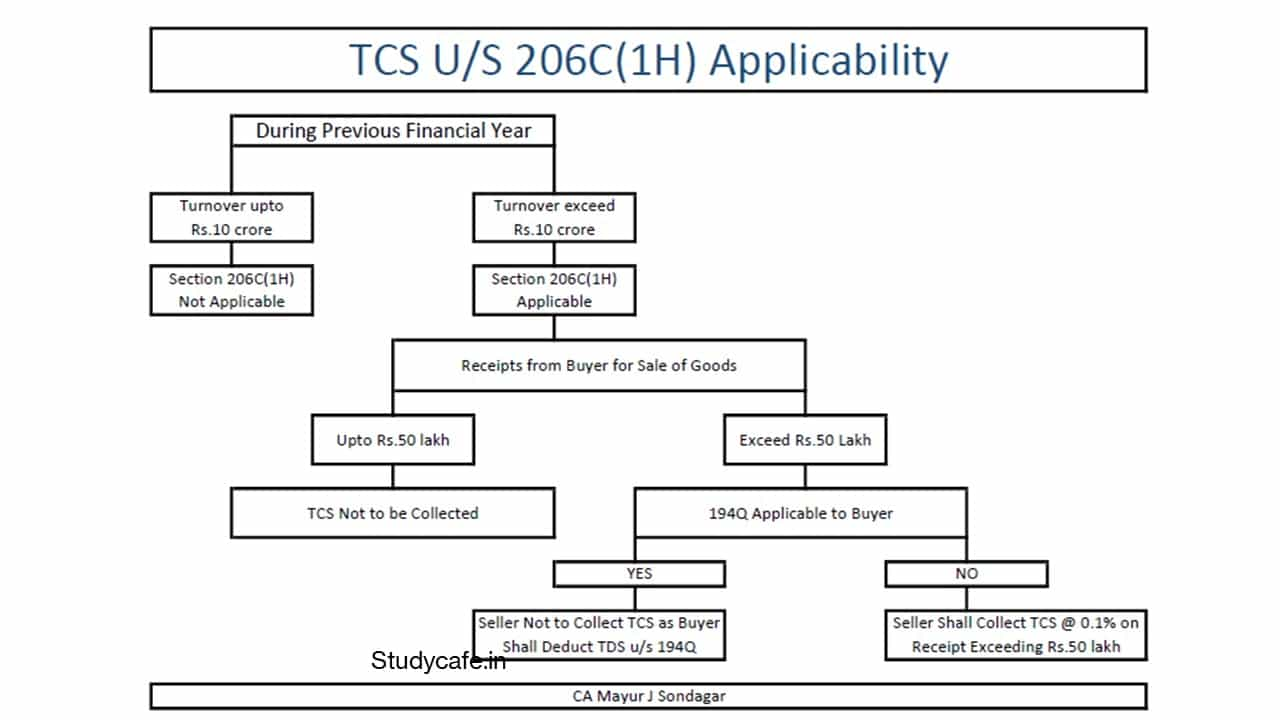

From Seller Side

| 1 |

If Sale Receipts Above 50 lakh |

If Buyer is not liable to Deduct TDS u/s 194Q then TCS u/s 206C(1H) @ 0.1 % on Receipts Above 50 lakh |

| If Buyer is liable to Deduct TDS under any other provision of this Act and has deducted such amount then No TCS u/s 206C(1H) |

| If Buyer is liable to Deduct TDS under any other provision of this Act and has not deducted such amount then TCS u/s 206C(1H) @ 0.1 % on Receipts Above 50 lakh |

| 2 |

If Sale Receipts upto 50 lakh |

No TCS u/s 206(1H) |

[caption id="attachment_101490" align="aligncenter" width="1280"]

TDS on Purchase & TCS on Sale explained with charts and Tally Entry[/caption]

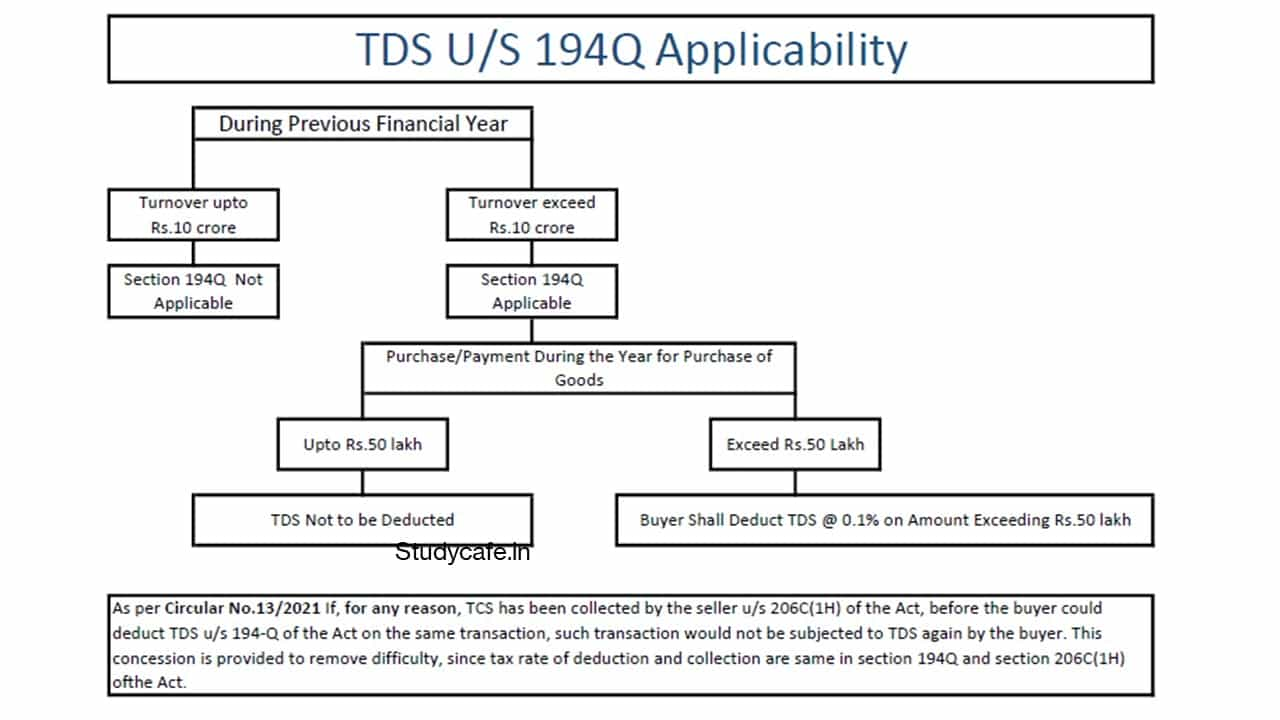

From Buyer Side

| 1 |

If Purchase Value Above 50 lakh |

Deduction TDS u/s 194Q @ 0.1 % on Value Above 50 lakh |

| 2 |

If Purchase Value upto 50 lakh |

No TDS u/s 194Q but TCS u/s 206(1H) may be applicable if aggregate payment (Including last year due) exceed 50 lakh during the year |

Let's Have some Examples

| Seller's Turnover (Cr) |

Buyer's Turnover (Cr) |

Transaction Value (Lakh) |

Receipt (Lakh) |

Section Applicable |

Reason |

| 13.00 |

12.00 |

60.00 |

60.00 |

194Q - TDS |

No TCS as TDS applied |

| 8.00 |

12.00 |

60.00 |

60.00 |

194Q - TDS |

Buyer's Turnover Above 10 Cr |

| 13.00 |

7.00 |

60.00 |

60.00 |

206C(1H) - TCS |

Seller's Turnover Above 10 Cr |

| 8.00 |

7.00 |

60.00 |

60.00 |

No TDS/TCS |

Turnover upto 10 Cr |

| 13.00 |

12.00 |

45.00 |

45.00 |

No TDS/TCS |

Transaction Value upto 50 Lakh |

| 13.00 |

7.00 |

45.00 |

60.00 |

206C(1H) - TCS |

Receipts Above 50 Lakh |

| 8.00 |

12.00 |

45.00 |

60.00 |

No TDS |

Transaction Value upto 50 Lakh |

| 13.00 |

7.00 |

60.00 |

45.00 |

No TCS |

Receipts upto 50 Lakh |

Short Summary:

| Particular |

SECTION 194Q |

SECTION 206C(1H) |

| Tax |

TDS |

TCS |

| Applicable to |

Buyer |

Seller |

| Applicable on |

Purchase of Goods |

Sale of Goods |

| Turnover Limit of Previous F.Y. |

10 Crore |

10 Crore |

| Threshold Limit |

50 Lakh |

50 Lakh |

| Normal Rate |

0.1% |

0.1% |

| Rate Without PAN |

5.0% |

1.0% |

| Time of Deduction/Collection |

Payment or Credit whichever is earlier |

At the time of Receipt |

| Deposit Date |

7th of Next Month |

7th of Next Month |

| TDS Return Form |

Form 26Q |

Form 27EQ |

Accounting Entries For TCS u/s 206C(1H) & TDS u/s 194Q

For Seller if he is liable to Collect TCS & Buyer have not Deducted TDS

| S.No. |

Transaction Type |

Particular |

Debit |

Credit |

| ENTRY NO. 1 |

At the time of Booking Sale Transaction |

Sundry Debtors |

1,05,000.00 |

|

| To Sale |

|

1,00,000.00 |

| To GST |

|

5,000.00 |

| ENTRY NO. 2 |

On Receipt of Sale Proceeds from Debtors |

Bank A/c |

1,05,000.00 |

|

| To Sundry Debtors |

|

1,05,000.00 |

| ENTRY NO. 3 |

Provision for TCS Liability on Date of Receiving Sale Proceeds |

Sundry Debtors |

105 |

|

| To TCS Payable |

|

105 |

| ENTRY NO. 4 |

On Payment of TCS on 7th of Next Month |

TCS Payable |

105 |

|

| To Bank A/c |

|

105 |

For Buyer if Seller have Collected TCS (Buyer is not liable to Deduct TDS)

| S.No. |

Transaction Type |

Particular |

Debit |

Credit |

| ENTRY NO. 1 |

At the time of Booking Purchase Transaction |

Purchase |

1,00,000.00 |

|

| GST |

5,000.00 |

|

| To Sundry Creditors |

|

1,05,000.00 |

| ENTRY NO. 2 |

On Payment to Sundry Creditors |

Sundry Creditors |

1,05,000.00 |

|

| To Bank A/c |

|

1,05,000.00 |

| ENTRY NO. 3 |

On Receipt of Debit note from Creditors |

TCS Receivable |

105 |

|

| To Sundry Creditors |

|

105 |

| ENTRY NO. 4 |

On Payment of TCS to Sundry Creditors |

Sundry Creditors |

105 |

|

| To Bank A/c |

|

105 |

For Seller if Buyer have Deducted TDS (Seller Shall not to Collect TCS)

| S.No. |

Transaction Type |

Particular |

Debit |

Credit |

| ENTRY NO. 1 |

At the time of Booking Sale Transaction |

Sundry Debtors |

1,05,000.00 |

|

| To Sale |

|

1,00,000.00 |

| To GST |

|

5,000.00 |

| ENTRY NO. 2 |

Receipt of Sale Proceeds from Debtors |

Bank A/c |

1,04,900.00 |

|

| To Sundry Debtors |

|

1,04,900.00 |

| ENTRY NO. 3 |

Entry of TDS Receivable on date of Receipt from Debtors |

TDS Receivable |

100 |

|

| To Sundry Debtors |

|

100 |

For Buyer if he is liable to Deduct TDS

| S.No. |

Transaction Type |

Particular |

Debit |

Credit |

| ENTRY NO. 1 |

At the time of Booking Purchase Transaction |

Purchase |

1,00,000.00 |

|

| GST |

5,000.00 |

|

| To Sundry Creditors |

|

1,04,900.00 |

| To TDS Payable |

|

100 |

| ENTRY NO. 2 |

On Payment of TDS on 7th of Next Month |

TDS Payable |

100 |

|

| To Bank A/c |

|

100 |

*Assumed GST Rate at 5 % / TCS Rate at 0.1 % / TDS Rate at 0.1 % / Threshold Limit of Rs.50 Lakh was crossed

*TCS to be Collected on Total Amount including GST

*TDS to be Deducted on Amount excluding GST & Purchase Return

Mumbai, Maharashtra, India

Mumbai, Maharashtra, India 12

12