Ulips Bought After Jan 2021 Will be Taxable; Exempt Only Under These Conditions: Govt issues rules

Deepak Gupta | Jan 20, 2022 |

Budget 2021 had proposed to remove the tax-exempt status on the proceeds of ULIPs if the annual premium exceeded Rs 2.5 lakh.

On January 19, 2022, the Central Board of Direct Taxes (CBDT) publishes the Computation of Capital Gains rule, which explains the mechanism for determining whether ULIPs are tax-exempt.

However, there were many questions about how the framework would work, particularly in the case of multiple ULIPs, which include both types purchased before and after the budget proposals.

Old ULIPs purchased before February 1, 2021 were regarded completely tax-free; however, this does not mean that you can continue to enjoy tax-free status by purchasing new ULIPs with premiums up to Rs 2.5 lakh. According to the current CBDT notification, the aggregate premium of both new and old ULIPs would be considered for exemption, and if the total surpasses Rs 2.5 lakh, the exemption will not be granted for new ULIPs with premiums above Rs 2.5 lakh.

If you were going to purchase ULIPs in order to benefit from tax-free returns, you’ll need to be cautious and double-check if they will qualify for tax exemption under the new tax laws.

The same are explained by way of examples of different situations:-

Situation1: No consideration is received by the assessee on any eligible ULIPs during any previous year preceding the current previous year or consideration has been received on such eligible ULIPs but has not been claimed exempt. The exemption under clause (10D) of

section 10 of the Act shall be determined as under:

i. If the assessee has received consideration, during the current previous year, under one eligible ULIP only and the amount of premium payable on such eligible ULIP does not exceed Rs 2,50,000 for any of the previous years during the term of such eligible ULIP, such consideration shall be eligible for exemption under the said clause (10D);

ii. If the assessee has received consideration, during the current previous year, under one eligible ULIP only and the amount of premium payable on such eligible ULIP exceeds Rs 2,50,000 for any of the previous years during the term of such eligible ULIP, such consideration shall not be eligible for exemption under the said clause (10D);

iii. If the assessee has received consideration, during the current previous year, under more than one eligible ULIPs and the aggregate of the amount of premium payable on such eligible ULIPs does not exceed Rs 2,50,000 for any of the previous years during the term of such eligible ULIPs, such consideration shall be eligible for exemption under the said clause (10D);

iv. If the assessee has received consideration, during the current previous year, under more than one eligible ULIPs and the aggregate of the amount of premium payable on such eligible ULIPs exceeds Rs 2,50,000 for any of the previous years during the term of such eligible ULIPs, the consideration under only such eligible ULIPs shall be eligible for exemption under the said clause (10D) where aggregate of the amount of the premium payable does not exceed Rs 2,50,000 for any of the previous years during their term (Refer Examples).

Situation 2: Consideration has been received by the assessee under any one or more eligible ULIPs during any previous year preceding the current previous year and it has been claimed to be exempt under clause (10D) of section 10 of the Act. Such eligible ULIPs are referred as “Old ULIPs” in this paragraph and corresponding examples and reference to eligible ULIPs shall not include old ULIPs. The exemption under clause (10D) of section 10

of the Act shall be determined as under:

i. If the assessee has received consideration, during the current previous year, under one eligible ULIP only and aggregate amount of premium payable on such eligible ULIP and old ULIPs does not exceed Rs 2,50,000 for any of the previous year during the term of such eligible ULIP, the consideration under such eligible ULIP shall be eligible for exemption under the said clause (10D);

ii. If the assessee has received consideration, during the current previous year, under one eligible ULIP only and aggregate amount of premium payable on such eligible ULIP and old ULIPs exceeds Rs 2,50,000 for any of the previous year during the term of such eligible ULIP, the consideration under such eligible ULIP shall not be eligible for exemption under the said clause (10D);

iii. If the assessee has received consideration, during the current previous year, under more than one eligible ULIPs and aggregate of the amount of premium payable on such eligible ULIPs and old ULIPs does not exceeds Rs 2,50,000 for any of the previous year during the term of such eligible ULIPs, such consideration shall be eligible for exemption under the said clause (10D);

iv. If the assessee has received consideration, during the current previous year, under more than one eligible ULIPs and aggregate of the amount of premium payable on such eligible ULIPs and old ULIPs exceeds Rs 2,50,000 for any of the previous year during the term of such eligible ULIPs, consideration under only such eligible ULIPs shall be eligible for exemption under the said clause (10D) where aggregate amount of premium along with the aggregate amount of premium of old ULIPs does not exceed Rs 2,50,000 for any of the previous year during the term of any of such eligible ULIPs (refer examples).

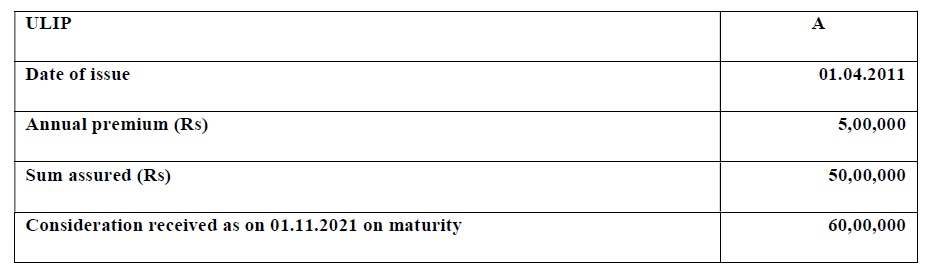

Example 1:

The assessee has the following policy which satisfies all the conditions laid down in clause (10D) of section 10 of the Act (other than the conditions provided under the fourth and fifth proviso of the said clause, applicability whereof is being explained in the example).

Taxability as per fourth proviso to clause (10D) of section 10 of the Act:

The sum received on maturity will be exempt under clause (10D) of section 10 of the Act as the policy has been issued before 01.02.2021 and accordingly not covered by the 4th to 7th provisos to the said clause (10) of section 10, inserted by Finance Act, 2021.

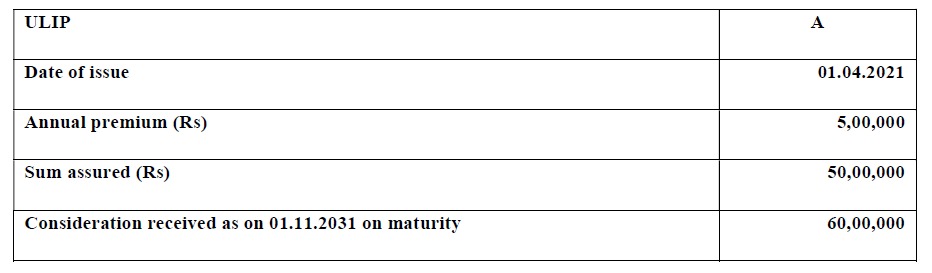

Example 2:

The assessee has the following policy which satisfies all the conditions laid down in clause (10D) of section 10 of the Act (other than the conditions provided under the fourth and fifth proviso of the said clause, applicability whereof is being explained in the example). The assesse did not receive any consideration under any other eligible ULIPs in earlier previous years preceding the previous year 2031-32.

Taxability as per fourth proviso to clause (10D) of section 10 of the Act:

The consideration received will not be exempt under clause (10D) as per the provisions of fourth proviso since the annual premium payable on the policy exceeded Rs 2,50,000.

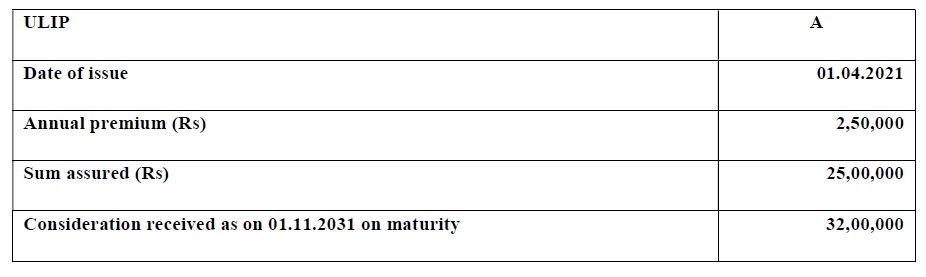

Example 3:

The assessee has the following policy which satisfies all the conditions laid down in clause (10D) of section 10 of the Act (other than the conditions provided under the fourth and fifth proviso of the said clause, applicability whereof is being explained in the example). The assessee did not receive any consideration under any other eligible ULIPs in earlier previous years preceding the previous year 2031-32.

Taxability as per fourth proviso to clause (10D) of section 10 of the Act:

The consideration received will be exempt under clause (10D) as the provisions of fourth proviso will not apply since the annual premium payable on the policy does not exceed Rs 2,50,000.

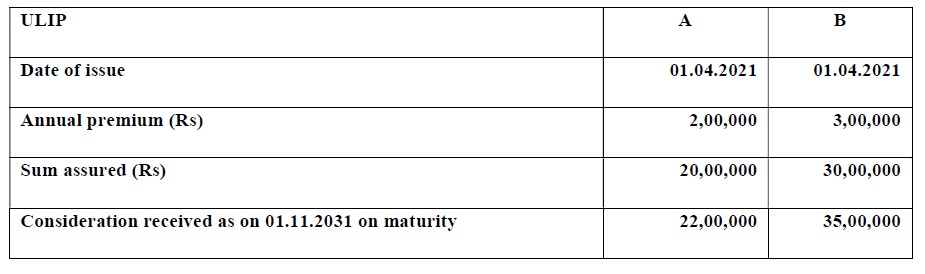

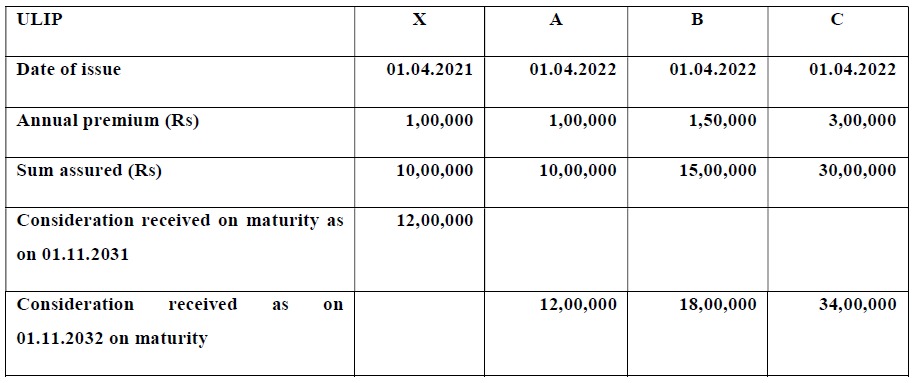

Example 4:

The assessee has the following policies all of which satisfy all the conditions laid down in clause (10D) of section 10 of the Act (other than the conditions provided under the fourth and fifth proviso of the said clause, applicability whereof is being explained in the example). The assessee did not receive any consideration under any other eligible ULIPs in earlier previous years preceding the previous year 2031-32.

Taxability as per fifth proviso to clause (10D) of section 10 of the Act:

The consideration received under ULIP “B” will not be exempt under clause (10D) as per the provisions of fifth proviso, since aggregate of the annual premium payable for ULIP “A” and ULIP “B” exceeds Rs 2,50,000 during the term of these policies. However, the consideration received under ULIP “A” shall be exempt under clause (10D) since its annual premium does not exceed Rs 2,50,000 in any of the previous years during the term of the policy.

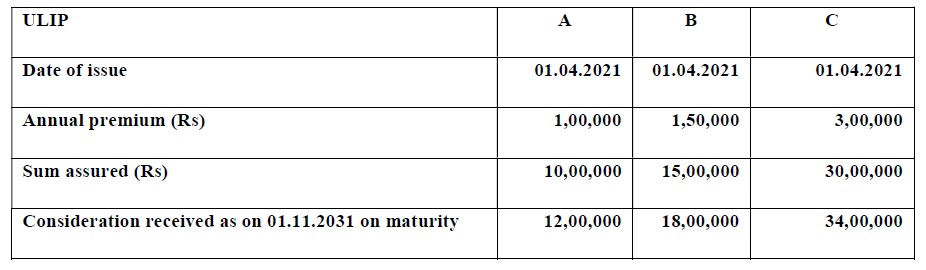

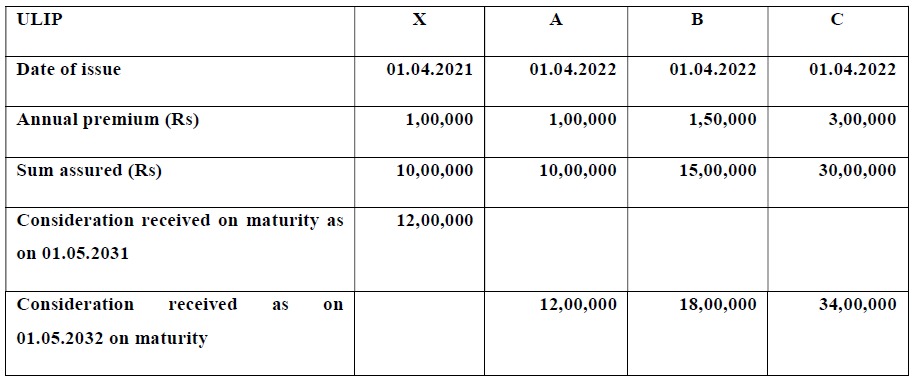

Example 5:

The assessee has the following policies all of which satisfy all the conditions laid down in clause (10D) of section 10 of the Act (other than the conditions provided under the fourth and fifth proviso of the said clause, applicability whereof is being explained in the example). The assessee did not receive any consideration under any other eligible ULIPs in earlier previous years preceding the previous year 2031-32.

Taxability as per fifth proviso to clause (10D) of section 10 of the Act:

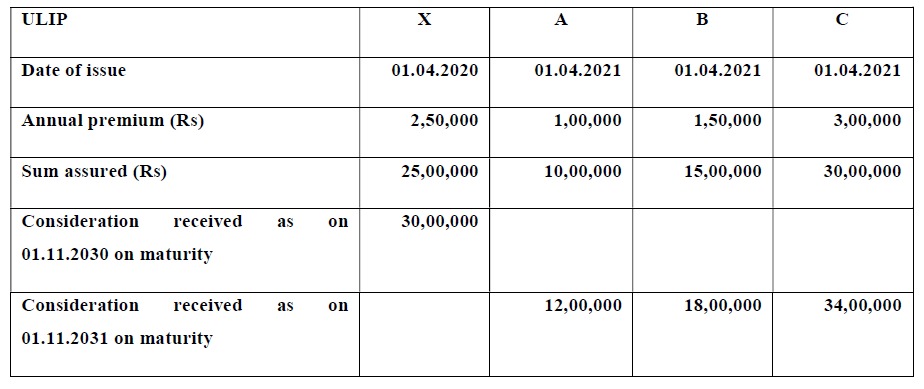

Example 6:

The assessee has the following policies all of which satisfy all the conditions laid down in clause (10D) of section 10 of the Act (other than the conditions provided under the fourth and fifth proviso of the said clause, applicability whereof is being explained in the example). The assessee did not receive any consideration under any other eligible ULIPs in earlier previous years preceding the previous year 2030-31.

Taxability as per fifth proviso to clause (10D) of section 10 of the Act:

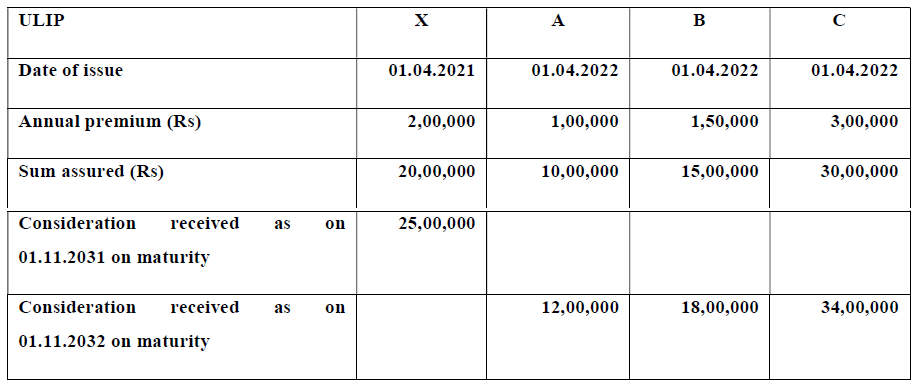

Example 7:

The assessee has the following policies all of which satisfy all the conditions laid down in clause (10D) of section 10 of the Act (other than the conditions provided under the fourth and fifth proviso of the said clause, applicability whereof is being explained in the example). The assessee did not receive any consideration under any other eligible ULIPs in earlier previous years preceding the previous year 2031-32.

Taxability as per fifth proviso to clause (10D) of section 10 of the Act:

Example 8:

The assessee has the following policies all of which satisfy all the conditions laid down in clause (10D) of section 10 of the Act (other than the conditions provided under the fourth and fifth proviso of the said clause, applicability whereof is being explained in the example). The assessee did not receive any consideration under any other eligible ULIPs in earlier previous years preceding the previous year 2031-32.

Taxability as per fifth proviso to clause (10D) of section 10 of the Act:

Example 9:

The assessee has the following policies all of which satisfy all the conditions laid down in clause (10D) of section 10 of the Act (other than the conditions provided under the fourth and fifth proviso of the said clause, applicability whereof is being explained in the example). The assessee did not receive any consideration under any other eligible ULIPs in earlier previous years preceding the previous year 2031-32. (It needs to be specified that consideration under ULIP “X” has not been claimed exempt)

Taxability as per fifth proviso to clause (10D) of section 10 of the Act:

The consideration under ULIP “X” was not claimed to be exempt under clause (10D) by the assessee therefore it is not covered within the definition of old ULIP.

The consideration received under ULIPs “A” and “B” will be exempt under clause (10D). However, since aggregate of the annual premium payable for the ULIPs “A” and “B” together did not exceed Rs 2,50,000 for any of the previous years during the term of any of these ULIPs “A” or “B” and ULIP “X” was not claimed to be exempt under clause (10D)the consideration received under ULIP “C” will be taxable as per the provisions of fifth proviso to the said clause (10D) of section 10 of the Act.

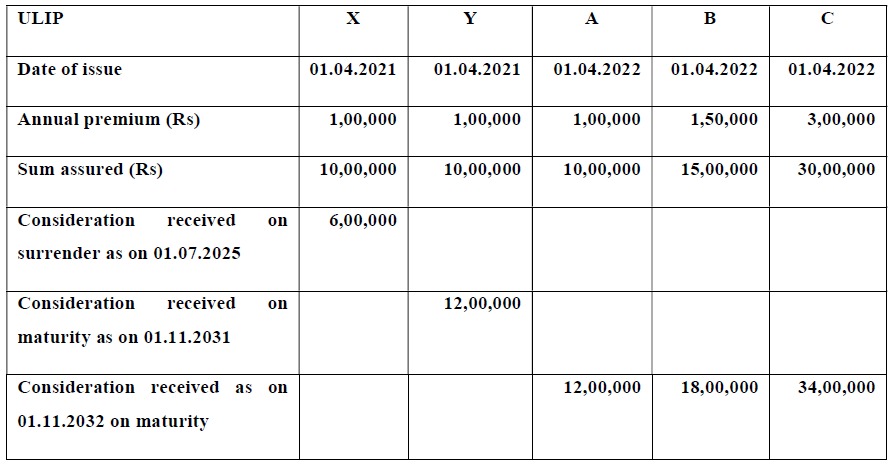

Example 10:

The assessee has the following policies all of which satisfy all the conditions laid down in clause (10D) of section 10 of the Act (other than the conditions provided under the fourth and fifth proviso of the said clause, applicability whereof is being explained in the example). The assessee did not receive any consideration under any other eligible ULIPs in earlier previous years preceding the previous year 2032-33 other than under ULIPs “X” and “Y”

Taxability as per fifth proviso to clause (10D) of section 10 of the Act:

Example 11: If in Example 10, the assessee does not claim exemption with respect to the surrender value of ULIP “X”, then the consideration received under ULIP “Y” will be exempt for the previous year 2031-32 and the consideration received under ULIP “B” will be exempt for the previous year 2032-33 under clause (10D). The exemption is restricted to ULIP “B” since the aggregate of the annual premium payable for the ULIPs “Y” and “B” together did not exceed Rs 2,50,000 for any of the previous years during the term of ULIP “Y” or “B” and the assessee did not claim ULIP “X” as exempt. ULIP “B” is preferred in place of ULIP “A” as it is more beneficial to the assessee.

In case of any Doubt regarding Membership you can mail us at [email protected]

Join Studycafe's WhatsApp Group or Telegram Channel for Latest Updates on Government Job, Sarkari Naukri, Private Jobs, Income Tax, GST, Companies Act, Judgements and CA, CS, ICWA, and MUCH MORE!"