ROC penalised the company for not disclosing a related-party loan in its Board’s Report and Form AOC-4, violating the Companies Act, 2013.

Vanshika verma | May 27, 2026 |

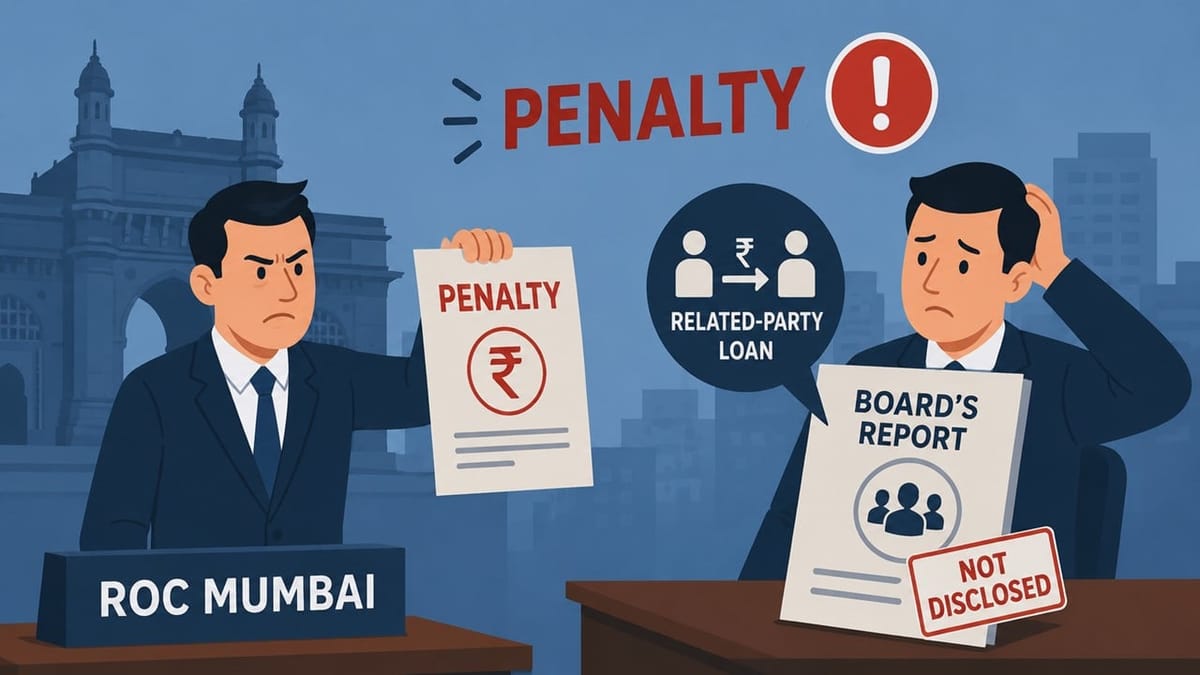

ROC Mumbai Imposes Penalty for Non-Disclosure of Related-Party Loan in Board’s Report

The Registrar of Companies (ROC), Mumbai, has penalised a company, “Om Shyamji Foods Private Limited”, for non-disclosure of related party loan transactions in the Board’s Report and Form AOC-4.

The Ministry of Corporate Affairs had ordered an inspection of the company through a letter dated March 2, 2022. The inspection report was submitted on May 23, 2023. The company had also voluntarily filed an application regarding the matter through Form GNL-1.

During the audit of the financial statements of the company for FY 2020-21, the officials found that the company had taken a loan of Rs. 1,67,20,462 from a related party. But this transaction was not disclosed in the Board’s Report or in Form AOC-4 under Accounting Standard AS-18. It was held to be a violation of Section 134(3)(h) of the Companies Act, 2013, which requires disclosure of related-party contracts and arrangements in the report of the Board of Directors of the company.

A show-cause notice was issued to the company and its directors on 10 October 2025 under Section 454 read with Section 134(8) of the Companies Act. As no reply was submitted on the e-adjudication portal, the adjudicating officer scheduled an e-hearing on 11 December 2025.

The company and its directors contended that as the loan transaction was between sister concerns, it was not governed under Section 188(1) of the Act, which relates to related-party transactions like sale and purchase arrangements. Hence, the company was not required to disclose it in the board’s report.

However, the adjudicating officer rejected this contention. The officer pointed out that the company had earlier admitted its error through a letter dated 31st March 2023, terming it a “clerical error” and requesting condonation. The officer held that the company had indeed violated Section 134(3)(h), based on the admission and inspection findings.

The officer also observed that the company did not qualify as a “small company” during the relevant financial year because its paid-up capital stood at Rs. 2,00,00,000 and turnover exceeded Rs. 16,24,34,127. Therefore, the benefit of reduced penalties under Section 446B could not be granted.

Consequently, the company was fined Rs 3 lakh under Section 134(8) of the Companies Act. The directors were also slapped with penalties of Rs 50,000 each for the default.

In case of any Doubt regarding Membership you can mail us at [email protected]

Join Studycafe's WhatsApp Group or Telegram Channel for Latest Updates on Government Job, Sarkari Naukri, Private Jobs, Income Tax, GST, Companies Act, Judgements and CA, CS, ICWA, and MUCH MORE!"