B2B mandatory, B2C Optional: GSTN system only validates mandatory B2B section in GSTR-1, Clarifies CBIC:

Registered taxpayers whose total turnover was up to Rs. 5 crore in the last financial year are not required to mention the HSN code in their tax invoices

HSN Code Mandatory for B2B, Optional for Small B2C Taxpayers

B2B mandatory, B2C Optional: GSTN system only validates mandatory B2B section in GSTR-1, Clarifies CBIC

The Central Board of Direct Taxes & Customs (CBIC) on its twitter handle has clarified that GSTN system only validates mandatory B2B section in GSTR-1 Return.

CBIC wrote that in accordance with Notification No. 12/2017-Central Tax dated 28th June 2017 (as amended), any registered taxpayer whose total turnover was up to Rs. 5 crore in the last financial year is not required to mention the number of digits of the HSN (Harmonised System of Nomenclature) code in their tax invoices released by him/her under the designated rules for the sales made to unregistered persons. This means that for B2C (Business to Consumer) transactions, small taxpayers have the option to leave out HSN codes on invoices.

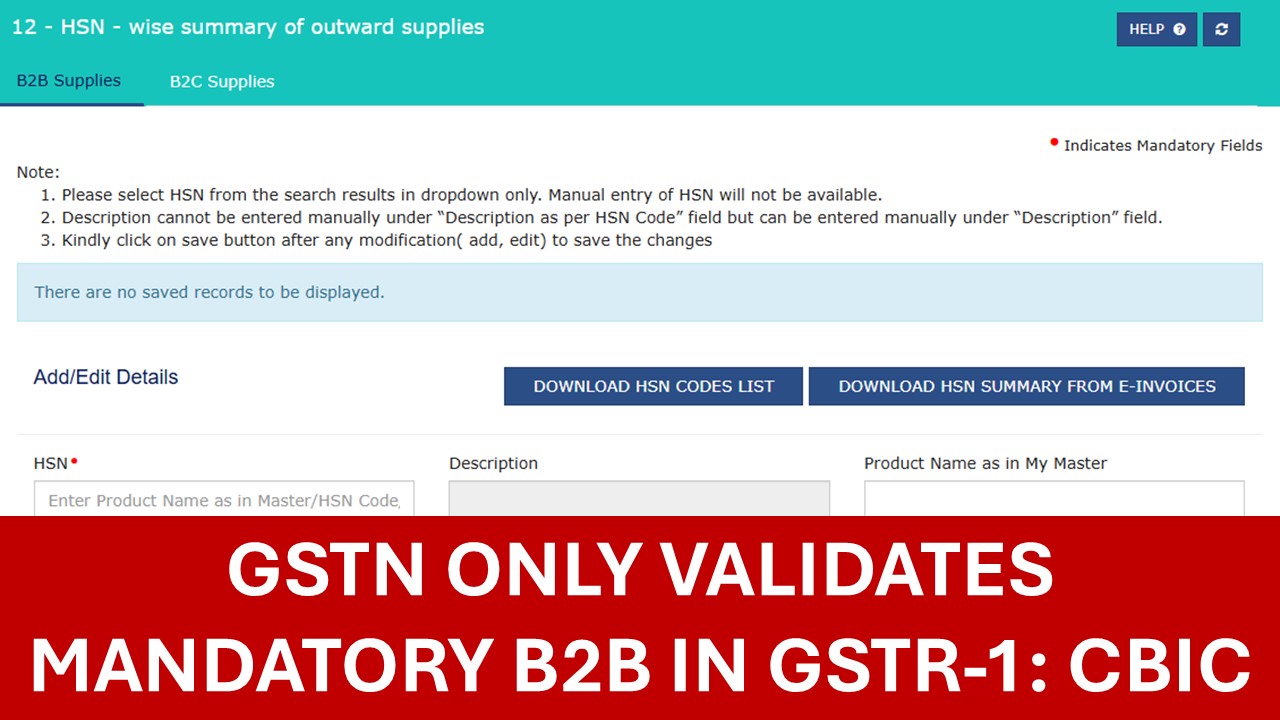

The Goods and Services Tax Network (GSTN) issued an advisory on May 01, 2025, saying Table 12 for the GSTR-1/1A return has been divided into two distinct sections: “B2B Supplies” and “B2C Supplies.” One for the purpose of B2B (Business to Business) supplies and the other for B2C (Business to Customer) supplies. Hence, taxpayers are now required to enter HSN summary details into both B2B and B2C separately under their respective sections.

In addition to this, the new feature has been implemented in the system. This feature will verify the HSN-wise values filled in Table 12 and confirm if the values align with the values mentioned in other parts of the tax return. This feature has been introduced to ensure that the data filed is accurate and consistent across all sections. For B2B transactions, the HSN summary is compulsory. Taxpayers are recommended to fill in the details accurately, as the system will not permit submission if it is left blank.

However, for B2C transactions, the GST system has not made it compulsory to provide an HSN summary, since the rule already permits small taxpayers with a total turnover of up to Rs. 5 crore to skip the HSN code. Hence, the system will not show any error if the B2C HSN section is left unfilled by such taxpayers.

This new setup ensures that B2B transactions are reported more accurately while still keeping compliance simple for small businesses dealing with regular customers.

About Author

Saloni Kumari

Content Writer

Saloni is a Content Writer with 2+ years of experience at studycafe.in. She writes legal, taxation, and finance related content including GST, Income Tax etc. Skilled in translating complex judicial pronouncements and regulatory developments into clear, and reader-friendly articles. Experienced in covering judgements of ITAT, High Court, GSTAT, and news related to Income Tax, GST, and corporate law. She can be reached at [email protected].

Saloni is a Content Writer with 2+ years of experience at studycafe.in. She writes legal, taxation, and finance related content including GST, Income Tax etc. Skilled in translating complex judicial pronouncements and regulatory developments into clear, and reader-friendly articles. Experienced in covering judgements of ITAT, High Court, GSTAT, and news related to Income Tax, GST, and corporate law. She can be reached at [email protected].

StudyCafe

StudyCafe Delhi, Delhi, India

Delhi, Delhi, India 2486

2486My Recent Articles

- ITAT Grants Taxpayer Fresh Opportunity to Contest Rs 44.16 Lakh Addition After Finding No Decision on MeritsPremium

- Trust’s Sections 12AB and 80G Registration Cannot Be Denied Before Charitable Project Is Completed, Holds ITATPremium

- ITAT Says Identity and Creditworthiness Irrelevant Where Loan Was Directly Paid to Haryana Mining DepartmentPremium

- Earlier Rejection Cannot Be Sole Ground to Reject Fresh Section 12AB and 80G Registration Applications, Says ITATPremium

- Cash Deposited During Demonetisation Cannot Be Taxed Under Section 69A if Linked to Business, Holds ITAT Premium

Up Next

Loading suggestions…

Recent Posts

All Posts

Tags

No tags yet.

Recent Posts

All Posts

Tags

No tags yet.