CBDT Mandates Structured UIN System for Form 121 (Earlier Form 15G & 15H) Declarations: Effective April 01, 2026:

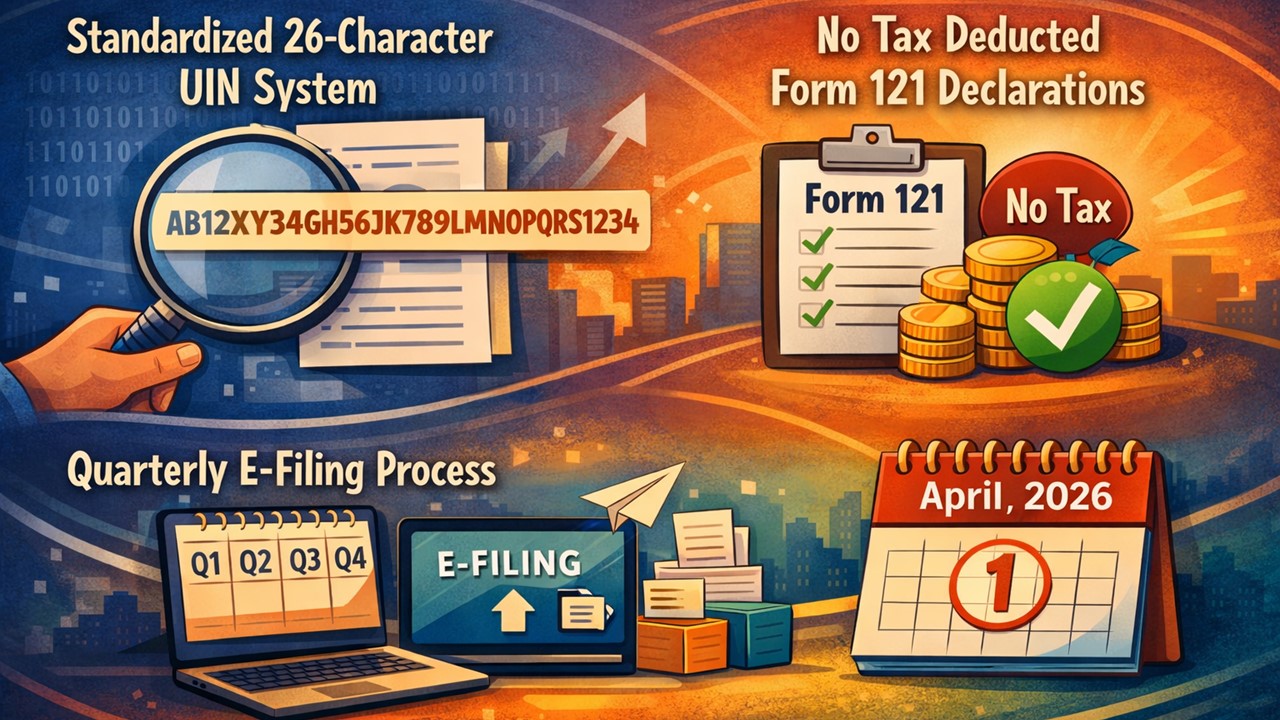

CBDT has mandated a standardised 26-character UIN system and quarterly e-filing process for Form 121 declarations where tax is not deducted, effective April 1, 2026.

CBDT Introduces 26-Character UIN System for Non-Deduction Declarations

CBDT Mandates Structured UIN System for Form 121 (Earlier Form 15G & 15H) Declarations: Effective April 01, 2026

The Directorate of Income-tax (Systems), New Delhi, under the Central Board of Direct Taxes (CBDT), Ministry of Finance, has issued a Notification No. 01/CPC(TDS)/2026, dated March 28, 2026, informing a clear procedure or format for generating and managing Unique Identification Numbers (UIN) for declarations filed in Form No. 121 and quarterly filing of Part B, under the Income-tax Act, 2025.

The notification is for cases where tax is not deducted as per the declaration furnished by the payee to the payer. As per the new rules, it has been made compulsory for the payer (person responsible for paying any income or sum of any nature specified under section 393(6) of the Act) to permit the payee to furnish Part A of Form No. 121 under section 397 of the Income Tax Act 2025, either in paper form or in electronic form after due verification through an electronic process.

The payee must provide their PAN in the declaration. The payer must provide a 26-character Unique Identification Number (UIN) to each received declaration under Sub-rule (3) of Rule 211 of the Rules. Thereafter, the payer must submit Part B of Form No. 121, which includes details of all declarations received, on a quarterly basis through the income tax e-filing portal at www.incometax.gov.in, within the prescribed time limit under section 393(7) of the Income Tax Act, 2025.

If a declaration is received in paper form, it must be digitised and assigned a UIN in the same sequence as electronic submissions. The sequence numbering will restart from "1" at the beginning of each tax year for every TAN. For every declaration received, the payer is required to generate a 26-character UIN. This UIN consists of three parts: a sequence number starting with “D” followed by nine digits, the relevant tax year in six-digit format, and the payer’s TAN.

The procedure or the format specified in the notification is scheduled to take effect from April 01, 2026.

Refer to the official notification for complete information

About Author

Saloni Kumari

Content Writer

Saloni is a Content Writer with 2+ years of experience at studycafe.in. She writes legal, taxation, and finance related content including GST, Income Tax etc. Skilled in translating complex judicial pronouncements and regulatory developments into clear, and reader-friendly articles. Experienced in covering judgements of ITAT, High Court, GSTAT, and news related to Income Tax, GST, and corporate law. She can be reached at [email protected].

Saloni is a Content Writer with 2+ years of experience at studycafe.in. She writes legal, taxation, and finance related content including GST, Income Tax etc. Skilled in translating complex judicial pronouncements and regulatory developments into clear, and reader-friendly articles. Experienced in covering judgements of ITAT, High Court, GSTAT, and news related to Income Tax, GST, and corporate law. She can be reached at [email protected].

StudyCafe

StudyCafe Delhi, Delhi, India

Delhi, Delhi, India 2515

2515My Recent Articles

- Missed July 31 ITR Deadline? Here’s What Taxpayers Need to Know Now

- Confused Between Belated, Revised and Updated Return? Here's Clarification on What You Should File

- Missed the July 31 ITR Deadline? File Your Belated Return to Avoid Penalties, Refund Loss, and Tax Notices

- Why Do You Need to File an ITR? 6 Key Reasons Every Taxpayer Must Know Before July 31 Deadline

- SC Directs IGP Kiran S. to Head Reconstituted SIT, Directs CA Appointment in Ayodhya Ram Temple Donation Theft Probe

Up Next

Loading suggestions…

Recent Posts

All Posts

Recent Posts

All Posts