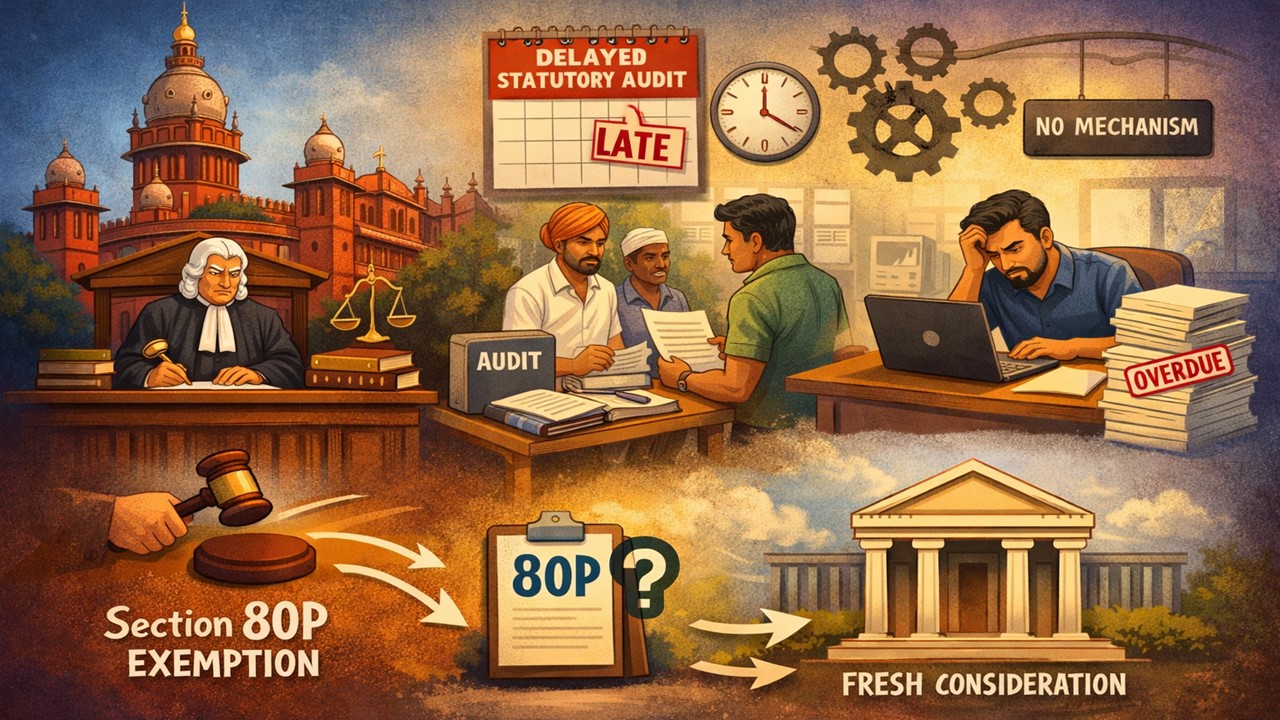

High Court Grants Section 80P Exemption despite Belated ITR Filing:

The HC holds that cooperative societies generally face difficulty in filing returns timely because of the belated approval of statutory audits and the absence of an adequate mechanism.

Section 80P Exemption Case Remanded for Fresh Consideration

High Court Grants Section 80P Exemption despite Belated ITR Filing

The Madras High Court grants relief to Irukkandurai Primary Agriculture Cooperative Credit Society, holding that cooperative societies generally face difficulty in filing returns timely because of the belated approval of statutory audits and the absence of an adequate mechanism.

The tax authorities had rejected the society's tax exemption claim, made under Section 80P of the Income Tax Act, 1961, because it had not furnished its ITR within the statutory time limit prescribed under Section 80-AC.

During the personal hearing before the High Court, the petitioner claimed that the delay was not intentional, and additionally, it was also willing to file an application seeking condonation of the delay under Section 119(2)(b) of the Act. However, the tax authorities claimed that the society had neither filed an application for condonation of delay nor furnished any appeal challenging the denial of its Section 80P exemption claim.

When the court analysed the case, it noted that cooperative societies often face practical difficulties like belated approval of statutory audits and the absence of an adequate mechanism, which ultimately leads to delays in filing their returns. The court highlighted that such delays are not always due to the intention of tax evasion but sometimes due to procedural challenges.

Considering all the challenges faced by society, the court decided to grant it another chance of relief. The society has been directed to file an application seeking condonation of delay within two weeks with the Chief Commissioner, explaining the detailed reasons behind the delay. Thereafter, the Chief Commissioner must decide on the application within three months. Thereafter, the society is directed to file an appeal before the ITAT along with the condonation of the delay application. The Tribunal has been asked to consider the Chief Commissioner’s decision while deciding the appeal.

About Author

Saloni Kumari

Content Writer

Saloni is a Content Writer with 2+ years of experience at studycafe.in. She writes legal, taxation, and finance related content including GST, Income Tax etc. Skilled in translating complex judicial pronouncements and regulatory developments into clear, and reader-friendly articles. Experienced in covering judgements of ITAT, High Court, GSTAT, and news related to Income Tax, GST, and corporate law. She can be reached at [email protected].

Saloni is a Content Writer with 2+ years of experience at studycafe.in. She writes legal, taxation, and finance related content including GST, Income Tax etc. Skilled in translating complex judicial pronouncements and regulatory developments into clear, and reader-friendly articles. Experienced in covering judgements of ITAT, High Court, GSTAT, and news related to Income Tax, GST, and corporate law. She can be reached at [email protected].

StudyCafe

StudyCafe Delhi, Delhi, India

Delhi, Delhi, India 2490

2490My Recent Articles

- ITAT Remands TDS Appeal After CIT(A) Failed to Decide Actual CAM Charges IssuePremium

- ITAT Rules in Taxpayer's Favour, Holds Delay in Filing Form 67 Cannot Be Sole Ground to Deny Foreign Tax CreditPremium

- ITAT Revives Tax Appeals for Six AYs After Finding Insufficient Hearing Time and Ignored Adjournment RequestPremium

- ITAT Grants Fresh Opportunity to Explain Rs 2.39 Crore Demonetisation Cash Deposit Addition After Main Director’s DeathPremium

- ITAT Grants Taxpayer Fresh Opportunity to Contest Rs 44.16 Lakh Addition After Finding No Decision on MeritsPremium

Up Next

Loading suggestions…

Recent Posts

All Posts

Recent Posts

All Posts