ITAT Rejects 100% Addition on Suspicious Sales; Remands Case for Fresh Consideration:

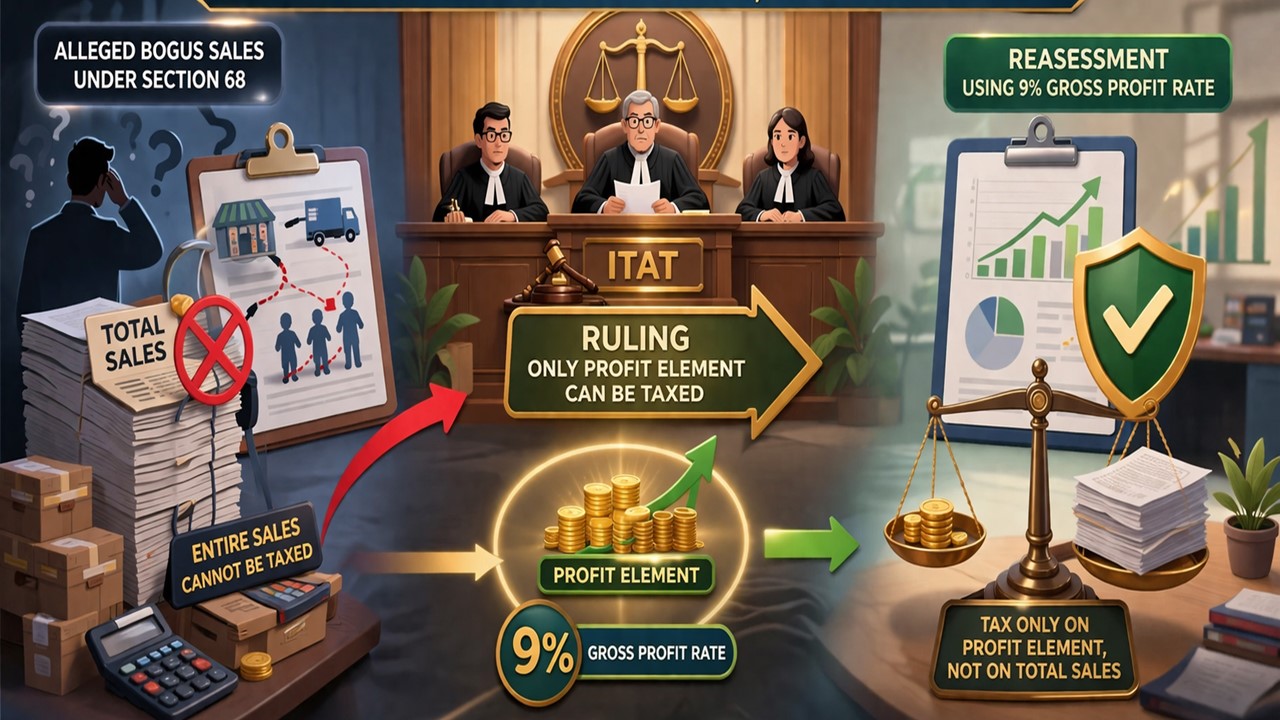

The ITAT ruled that in cases of alleged bogus sales under Section 68, only the profit element, not the entire sales amount, can be taxed, directing reassessment using a 9% gross profit rate.

ITAT Limits Additions to 9% Profit on Alleged Bogus Sales

ITAT Rejects 100% Addition on Suspicious Sales; Remands Case for Fresh Consideration

The Income Tax Appellate Tribunal (ITAT), Ahmedabad Bench, has recently delivered its judgement in a dispute that mainly relates to the additions made by the tax authorities under Section 68 of the Income Tax Act, which deals with unexplained cash credits, for Assessment Years 2014-15, 2015-16, and 2016-17.

The assessee company, Shri Bhumika Strips Private Limited, is engaged in the business of manufacturing stainless steel products. It furnished its income tax return (ITR) for the Assessment Year 2014-15, declaring its total income at Rs 20,65,910. The tax authorities had received information from the Investigation Wing that the assessee had taken the benefit of accommodation entry for Rs 1.60 crore from several companies. The tax authorities treated certain sales as suspicious and made an addition amounting to Rs 1.60 crore to the assessee's income as unexplained income for AY 2014-15. Similar additions were made for the other years.

The assessee argued that all the sales in question were properly recorded, supported by invoices and already included in taxable income. It further flagged that its booked accounts were not rejected by the tax authorities. Hence, it is unfair to make an addition to the entire sales amount. When the tribunal analysed the facts of the case, it noted that it is a settled legal principle that when sales are recorded in the books, only the profit element embedded in such transactions can be taxed, not the full amount. The Tribunal also noted that the company’s average gross profit rate over the years was around 9%.

Accordingly, the tribunal instructed the tax authorities to recalculate the additions by applying a 9% gross profit rate rather than taxing the entire sales in question. The case is sent back to the tax authorities with directions to freshly consider it after giving the assessee a proper opportunity of hearing. Thus, the appeal was allowed for statistical purposes.

About Author

Saloni Kumari

Content Writer

Saloni is a Content Writer with 2+ years of experience at studycafe.in. She writes legal, taxation, and finance related content including GST, Income Tax etc. Skilled in translating complex judicial pronouncements and regulatory developments into clear, and reader-friendly articles. Experienced in covering judgements of ITAT, High Court, GSTAT, and news related to Income Tax, GST, and corporate law. She can be reached at [email protected].

Saloni is a Content Writer with 2+ years of experience at studycafe.in. She writes legal, taxation, and finance related content including GST, Income Tax etc. Skilled in translating complex judicial pronouncements and regulatory developments into clear, and reader-friendly articles. Experienced in covering judgements of ITAT, High Court, GSTAT, and news related to Income Tax, GST, and corporate law. She can be reached at [email protected].

StudyCafe

StudyCafe Delhi, Delhi, India

Delhi, Delhi, India 2490

2490My Recent Articles

- ITAT Remands TDS Appeal After CIT(A) Failed to Decide Actual CAM Charges IssuePremium

- ITAT Rules in Taxpayer's Favour, Holds Delay in Filing Form 67 Cannot Be Sole Ground to Deny Foreign Tax CreditPremium

- ITAT Revives Tax Appeals for Six AYs After Finding Insufficient Hearing Time and Ignored Adjournment RequestPremium

- ITAT Grants Fresh Opportunity to Explain Rs 2.39 Crore Demonetisation Cash Deposit Addition After Main Director’s DeathPremium

- ITAT Grants Taxpayer Fresh Opportunity to Contest Rs 44.16 Lakh Addition After Finding No Decision on MeritsPremium

Up Next

Loading suggestions…

Recent Posts

All Posts

Recent Posts

All Posts