GSTR 3B Mentioning details of inter-State supplies made to unregistered persons

GSTR 3B Mentioning details of inter-State supplies made to unregistered persons As per Circular Number 89/08/2019-GST dated 18th February, 2

GSTR 3B Mentioning details of inter-State supplies made to unregistered persons

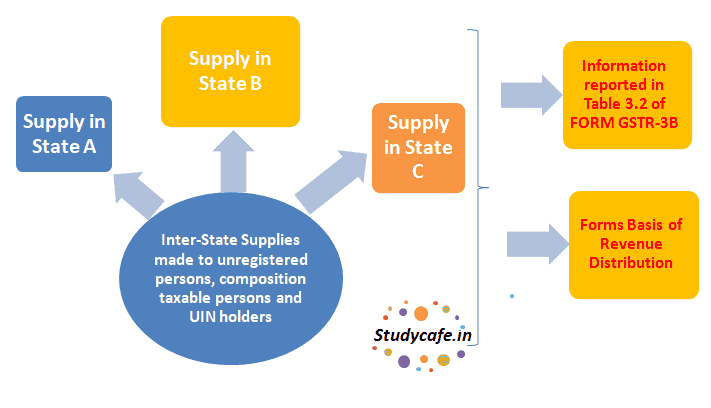

As per Circular Number 89/08/2019-GST dated 18th February, 2019 CBIC has clarified that while filing GST Returns, A registered supplier is required to mention the details of inter -State supplies made to unregistered persons, composition taxable persons and UIN holders in Table 3.2 of FORM GSTR-3B.

Further, the details of all inter-State supplies made to unregistered persons where the invoice value is up to Rs 2.5 lakhs (rate-wise) are required to be reported in Table 7B of FORM GSTR-1.

Why it is important to mention details of inter-State supplies made to unregistered persons in GSTR 3B and GSTR 1

It is important to note that apportionment of IGST collected on interState supplies made to unregistered persons in the State where such supply takes place is based on the information reported in Table 3.2 of FORM GSTR-3B by the registered person. As such, non-mentioning of the said information results in

(i) non-apportionment of the due amount of IGST to the State where such supply takes place; and

(ii) a mis-match in the quantum of goods or services or both actually supplied in a State and the amount of integrated tax apportioned between the Centre and that State, and consequent non-compliance of sub-section (2) of section 17 of the Integrated Goods and Services Tax Act, 2017.

In Simple words, we all know that GST is destination based tax, which means that revenue of GST will be given to state where consumption of Goods/Service Takes Place.

Now when it comes to distribution of Revenue, it is easy for government to identify that which state deserves the revenue when it is case of CGST & SGST. [For supply to both registered and unregistered supplier]

Also in case case of IGST it is easy for government to identify that which state deserves the revenue in case of registered supplier.

But when it comes to distribution of IGST in case of supply to unregistered person, Table 3.2 of FORM GSTR-3B is the mechanism through which we inform government, name of the state where consumption has taken place. And that is the reason due to which it is important to mention details of inter-State supplies made to unregistered persons correctly in table 3.2 of GSTR 3B and Table 7B of FORM GSTR-1 .

Accordingly, CBIC has made it mandatory that the registered persons making inter-State supplies to unregistered persons shall report the details of such supplies along with the place of supply in Table 3.2 of FORM GSTR-3B and Table 7B of FORM GSTR1 as mandated by the law.

Contravention of any of the provisions of the Act or the rules made there under attracts penal action under the provisions of section 125 of the CGST Act.

Disclaimer: The entire contents of this document have been prepared on the basis of relevant provisions and as per the information existing at the time of the preparation. Although care has been taken to ensure the accuracy, completeness and reliability of the information provided, I assume no responsibility therefore. Users of this information are expected to refer to the relevant existing provisions of applicable Laws. The user of the information agrees that the information is not a professional advice and is subject to change without notice. I assume no responsibility for the consequences of use of such information.In no event shall I shall be liable for any direct, indirect, special or incidental damage resulting from, arising out of or in connection with the use of the information.

Circular No. |

Date of issue |

File No. |

Subject |

91/2019 |

18-02-2019 |

F. No. CBEC-20/16/04/2018 - GST |

Seeks to give clarification regarding tax payment made for supply of warehoused goods while being deposited in a customs bonded warehouse for the period July, 2017 to March, 2018. |

90/2019 |

18-02-2019 |

F. No. CBEC-20/16/04/2018 - GST |

Seeks to clarify situations of compliance of rule 46(n) of the CGST Rules, 2017 while issuing invoices in case of inter- State supply. |

89/2019 |

18-02-2019 |

F. No. CBEC-20/16/04/2018 - GST |

Seeks to clarify situations of mentioning details of inter-State supplies made to unregistered persons in Table 3.2 of FORM GSTR-3B and Table 7B of FORM GSTR-1. |

About Author

CA Deepak Gupta

Co Founder

StudyCafe

StudyCafe Delhi, Delhi, India

Delhi, Delhi, India 3423

3423My Recent Articles

- UltraTech Cement slapped with Rs. 808.78 Cr Income Tax Demand

- GST: High Court upheld constitutional validity of Section 16(2)(c), asks government to address ITC issues of genuine purchasers

- Old vs New Tax Regime for Tax Year 2026-27

- High court criticizes Income Tax Department for not releasing ITR Utilities despite 11 years of directions

- Fino Payments Bank CEO Rishi Gupta Gets Bail in GST Case, Bank Clarifies No Direct Link

Loading suggestions…

Recent Posts

All Posts

Tags

No tags yet.

Recent Posts

All Posts

Tags

No tags yet.