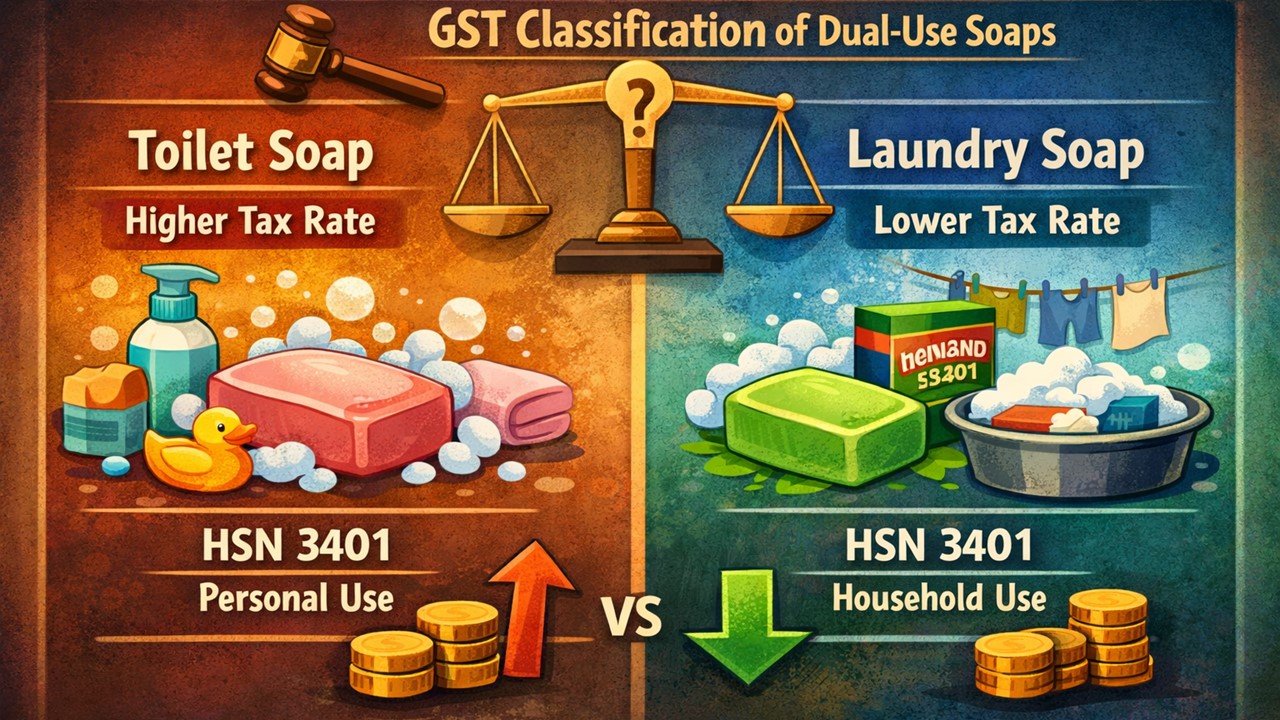

Toilet Soap vs Laundry Soap under GST: AAR Clarifies Classification of Dual-Use Soap under HSN 3401:

The AAR clarifies the GST classification and applicable tax rate for dual-use soap products, distinguishing “toilet soap” and “laundry soap” under HSN 3401.

AAR on Classification and Tax Rate after Notification 9/2025

Toilet Soap vs Laundry Soap under GST: AAR Clarifies Classification of Dual-Use Soap under HSN 3401

The company, M/s Tarwani Soap Industries (applicant), has filed an application dated October 14, 2025, seeking the Chhattisgarh Authority for Advance Ruling (AAR) Goods and Services Tax (GST) under Section 98 of the Chhattisgarh Goods and Services Tax Act, 2017.

The applicant possesses its registered office at Dhusera, Village-Dewarbhatta, Manabasti, Abhanpur, Raipur, Chhattisgarh, and is registered under GST, having GSTIN 22AAOFT9412HIZ1.

The applicant is engaged in the manufacture and supply of soap, primarily serving rural markets. The soap manufactured is multi-use and can be used for both personal hygiene (bathing) and laundry purposes, depending on consumer preference. Considering the proposals suggested in the recent 56th GST Council meeting held on September 03 and 04, 2025, the government issued a Notification No. 9/2025-CentralTax(Rate) dated September 17, 2025, effective from September 22, 2025, which has changed GST rates on soaps under HSN Code 3401. Now, the applicant has some questions regarding its business.

Questions Asked Before Chhattisgarh AAR:

The applicant has asked the following questions seeking the Chhattisgarh Authority for Advance Ruling (AAR):

"(i) The definition or guiding principle for determining "toilet soap" under HSN 3401, as referred to in Schedule I, Entry No. 251 of Notification No. 9/2025-Central Tax (Rate), 2025;

(ii) What constitutes "other soap (not toilet soap)" under Schedule II, Entry No.66 of the said notification:

(iii) Whether, given the composition of the applicant's soap (having TFM>60%) and its dual- use nature (bathing and laundry). The product should be classified under HSN 3401 19 41 ("Toilet soap") or HSN 340119 42 ("Laundry soap");

(iv) The applicable GST rate thereon."

Answers Given by Chhattisgarh AAR:

The Chhattisgarh Authority for Advance Ruling (AAR) has given the following answers to the questions asked by the applicant:

Answer (i): H.S. Code 3401 11, belonging to goods for toilet use (including medicated products), is the definition or guiding principle for determining "toilet soap" under heading no. 3401, as referred to in Schedule I, Entry No. 251 of Notification No. 9/2025-Central Tax (Rate), 2025, dated September 17, 2025.

Answer (ii): "Laundry soaps" constitute "other soap (not toilet soap)" under Schedule II, Entry No. 66 of Notification No. 9/2025-Central Tax (Rate), 2025, dated September 17, 2025.

Answer (iii): As per the information submitted by the applicant, "Toilet soaps" for washing the skin, manufactured and sold/supplied by the applicant, fall under ITC (HS) Code 3401 11 90, while "Laundry soaps" (other than toilet soaps) for washing purposes, manufactured and sold/supplied by the applicant, merit classification under 340119 42.

Answer (iv): As per Serial no. 251 of Schedule-I to Notification no. 9/2025-Central Tax (Rate) 2025, read with the corresponding Integrated Tax (Rate) Notification, both effective from September 22, 2025, toilet soaps (other than industrial soaps) in the form of bars, cakes, moulded pieces or shapes manufactured and sold or supplied by the applicant for washing of skin are classified under Heading no. 3401, attract GST at 5% [CGST 2.5% + CGGST 2.5%]

On the other hand, as per Serial no. 66 of Schedule II to Notification no. 9/2025-Central Tax (Rate) 2025, read with the corresponding Integrated Tax (Rate) Notification, both effective from September 22, 2025, laundry soaps in the form of cakes, moulded pieces or shapes, whether or not containing soap [other than toilet soap in the form of bars], cakes, moulded pieces or shapes manufactured and sold/supplied by the applicant for washing purposes are classified under Heading no. 3401; it attracts GST at 18% [CGST 9% + CGGST 9%].

About Author

Saloni Kumari

Content Writer

Saloni is a Content Writer with 2+ years of experience at studycafe.in. She writes legal, taxation, and finance related content including GST, Income Tax etc. Skilled in translating complex judicial pronouncements and regulatory developments into clear, and reader-friendly articles. Experienced in covering judgements of ITAT, High Court, GSTAT, and news related to Income Tax, GST, and corporate law. She can be reached at [email protected].

Saloni is a Content Writer with 2+ years of experience at studycafe.in. She writes legal, taxation, and finance related content including GST, Income Tax etc. Skilled in translating complex judicial pronouncements and regulatory developments into clear, and reader-friendly articles. Experienced in covering judgements of ITAT, High Court, GSTAT, and news related to Income Tax, GST, and corporate law. She can be reached at [email protected].

StudyCafe

StudyCafe Delhi, Delhi, India

Delhi, Delhi, India 2484

2484My Recent Articles

- ITAT Says Identity and Creditworthiness Irrelevant Where Loan Was Directly Paid to Haryana Mining DepartmentPremium

- Earlier Rejection Cannot Be Sole Ground to Reject Fresh Section 12AB and 80G Registration Applications, Says ITATPremium

- Cash Deposited During Demonetisation Cannot Be Taxed Under Section 69A if Linked to Business, Holds ITAT Premium

- ITAT Condones 1,731-Day Delay, Remands Cancer Trust's Section 12A Registration Application for Fresh ConsiderationPremium

- ITAT Lowers Estimated Profit Rate from 8% to 4% After Considering State Shutdown and Medicine Trade MarginsPremium

Up Next

Loading suggestions…

Recent Posts

All Posts

Recent Posts

All Posts