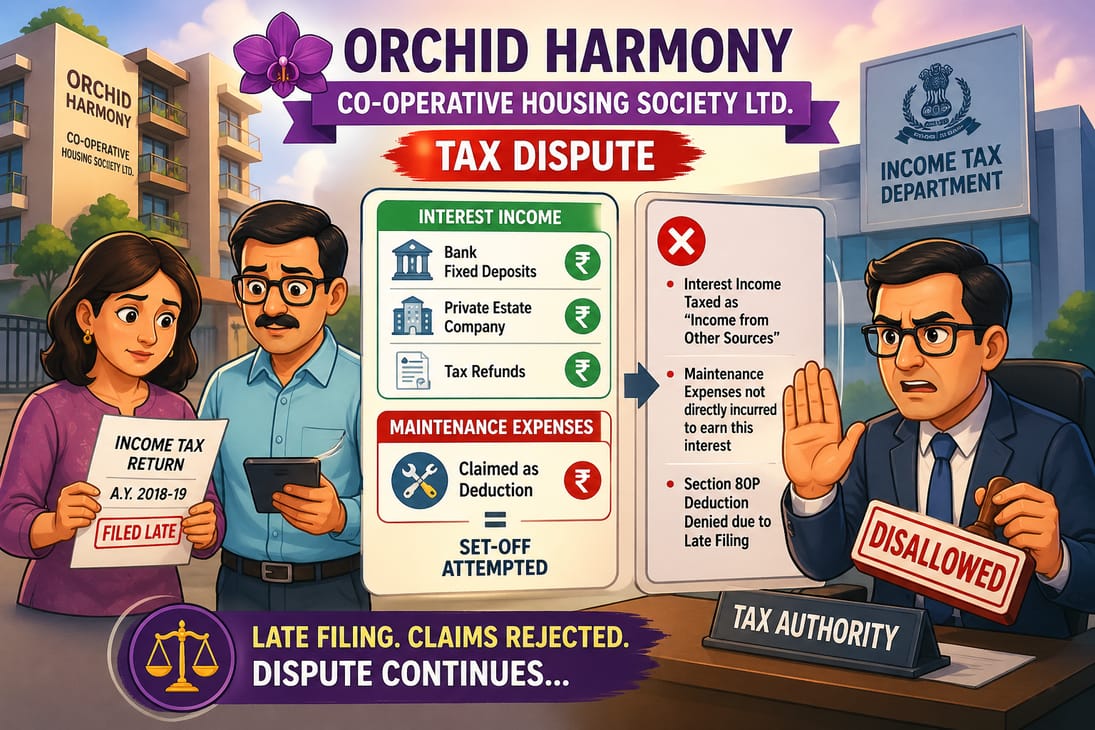

A cooperative housing society filed its tax return late and sought deductions on interest income, leading to a dispute with tax authorities over taxability and eligibility.

Khushi Jain | Apr 28, 2026 |

A delayed filing shouldn’t kill your tax benefits, but don’t expect maintenance costs to offset your interest income.

Facts of the case

The Orchid Harmony Co-operative Housing Service Society Ltd. faced a tax dispute after filing its income tax return for the 2018-19 assessment year past the legal deadline.

The society had reported interest income from bank fixed deposits, a private estate company, and tax refunds, and it attempted to offset this income by claiming an equal amount in maintenance expenses. However, tax authorities classified this interest as “Income from Other Sources” and disallowed the maintenance deduction, arguing that these expenses were not directly incurred to earn that interest. Additionally, the society was initially denied a tax deduction under section 80P specifically because their return was filed late.

Issue of the case

1. Whether the housing society’s interest income from bank and private investments should be taxed as “Income from Other Sources,”?

2. Whether the society is allowed to deduct its routine maintenance and administrative costs from that interest, and finally?

3. Whether the society is still entitled to a tax deduction under section 80P even though it missed the original deadline for filing its tax return.

Decision of the tribunal

The Tribunal decided that the interest a housing society earns from its bank accounts and investments is taxable as “Income from Other Sources” because the society owns these funds and is simply choosing to spend them on maintenance later, rather than the money being diverted away from them by a legal obligation at the source.

Because of this, the Tribunal ruled that the society cannot deduct its general maintenance and administrative costs against this interest, as those expenses were not directly and exclusively incurred to earn the interest income itself. However, the Tribunal did grant the society a win regarding the deduction under section 80P, concluding that the society should not be denied this tax benefit solely because it filed its return after the standard due date.

In case of any Doubt regarding Membership you can mail us at [email protected]

Join Studycafe's WhatsApp Group or Telegram Channel for Latest Updates on Government Job, Sarkari Naukri, Private Jobs, Income Tax, GST, Companies Act, Judgements and CA, CS, ICWA, and MUCH MORE!"