Tax Assessment Refinement: Judicial Ruling on Profit Estimation vs. Full Addition:

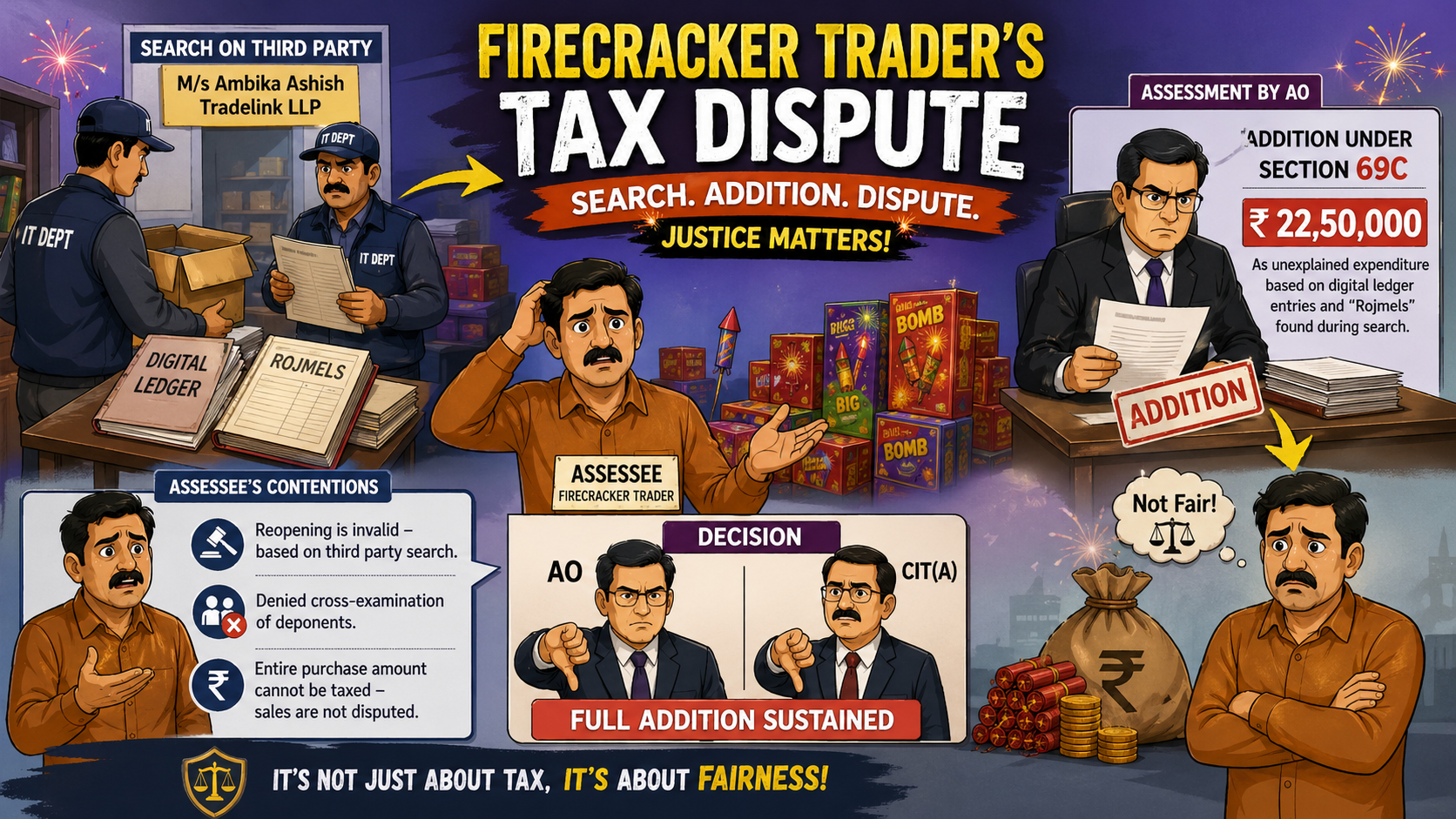

An individual firecracker trader faced an assessment reopening and a Rs. 2,250,000 addition for unexplained purchases discovered in third-party search records.

Reevaluating Taxation on Unsubstantiated Expenditure

Tax Assessment Refinement: Judicial Ruling on Profit Estimation vs. Full Addition

Between Documentary Evidence and Natural Justice: Fighting for Fair Taxation on Disputed Business Expenditures

Facts of the case

The assessee, a firecracker trader, faced an assessment reopening following a search on a third-party entity (M/s Ambika Ashish Tradelink LLP). The Assessing Officer (AO) added Rs. 22,50,000 as unexplained expenditure under Section 69C, based on digital ledger entries and "Rojmels" discovered during the search. The assessee contested the validity of the reopening, the denial of cross-examination of deponents, and argued that the entire purchase amount should not be taxed, as sales were not disputed. Both the AO and the CIT(A) sustained the full addition.

Issue of the case

1. Whether the failure to provide an opportunity for cross-examination of persons whose statements were relied upon invalidates the assessment.

2. Whether the entire amount of alleged unaccounted purchases is taxable, or if the addition should be restricted to the embedded profit element.

Decision of the Tribunal

The ITAT held that the denial of cross-examination did not vitiate the assessment because the addition was primarily supported by cogent documentary evidence (Rojmel/ledger data), with statements serving only as corroborative material. However, the Tribunal allowed the appeal in part, ruling that because the Revenue did not disturb the sales declared by the assessee, the purchases must have been incurred. Citing precedents such as CIT v. Simit P. Sheth, the Tribunal directed the AO to restrict the addition to a reasonable estimate of the profit element embedded in the purchases, rather than the entire purchase price.

About Author

Khushi Jain

Legal Content Writer

StudyCafe

StudyCafe Delhi, Delhi, India

Delhi, Delhi, India 80

80My Recent Articles

- ROC Chennai Orders Penalty for delay in filing MGT-17: Short Staff no Excuse

- Penalty Order Passed by ROC Chennai for Non-Disclosure in Form PAS-3

- ROC Imposes Penalty For Non-Compliance In Securities Allotment Filing

- GST: Bombay High Court Upholds Validity of Manual Appeal

- From Rs. 275 Crore to Zero: United Breweries Gets Relief in Sales Tax Dispute

Up Next

Loading suggestions…

Recent Posts

All Posts

Recent Posts

All Posts