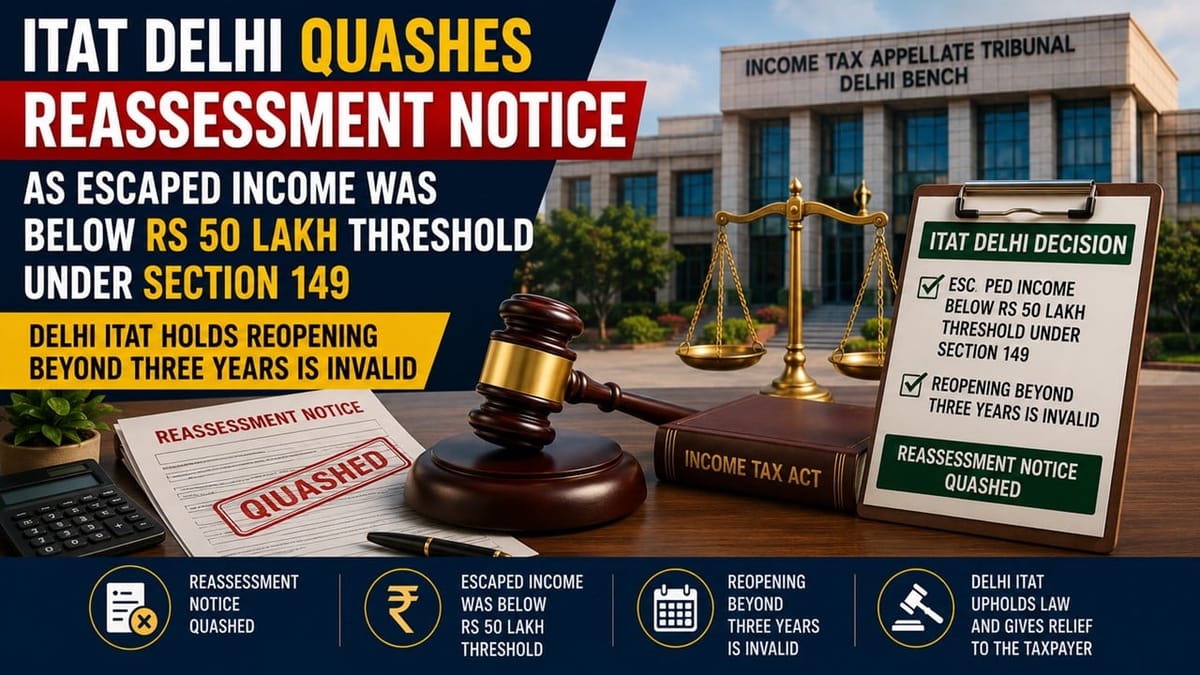

The Income Tax Appellate Tribunal (ITAT), Delhi, has quashed reassessment proceedings holding that the alleged escaped income was only Rs 4.27 lakh and not the entire transaction value.

Saima | Jun 15, 2026 |

Commodity Trader’s Rs. 2.48 Crore NSEL Transactions Drew Tax Scrutiny; ITAT Cancels Reassessment Over Rs. 4.27 Lakh Profit

The Income Tax Appellate Tribunal (ITAT), Delhi, held that where the income allegedly escaping assessment is below Rs 50 lakh, reopening beyond three years is impermissible and the notice issued under Section 148 is liable to be quashed.

The assessee had filed his return of income for assessment year 2014-15 but based on information received through the Insight Portal and an investigation report from the Mumbai Investigation Wing regarding transactions in the National Spot Exchange Limited (NSEL), the AO initiated reassessment proceedings under Sections 147 and 148. According to the department, client code modifications reflected transactions amounting to Rs 2.48 crore in the assessee’s name. On this basis, the AO passed an order under Section 148A(d) and issued notice under Section 148 of the Income-tax Act.

The assessee contended that the department had mechanically treated the entire transaction value of Rs 2.48 crore as escaped income without appreciating the nature of the transactions. The assessee further argued that the reopening was initiated after the expiry of three years and therefore could survive only if the conditions stipulated under Section 149(1)(b) were satisfied, namely that income represented in the form of an asset amounting to Rs 50 lakh or more had escaped assessment after relying on Union of India v. Ashish Agarwal for reference under Section 149.

The Tribunal observed that the AO had proceeded merely on the basis of information available on the Insight Portal and had failed to examine the true nature of the transactions. The department presumed that the entire turnover had escaped assessment, whereas the actual profit in those transactions was only Rs 4.27 lakh. The Tribunal observed that Section 149(1)(b) permits reopening after three years only where the AO furnishes material showing escaped income represented in the form of an asset amounting to Rs 50 lakh or more. In the present case, the amount involved was far below the statutory threshold.

Since the conditions prescribed under Section 149(1)(b) were not fulfilled, the notice issued under Section 148 was held to be beyond the period of limitation. Allowing the appeal, the Delhi Bench of the ITAT held that the reassessment proceedings were barred by limitation and, consequently, quashed the notice issued under Section 148 of the Income-tax Act, 1961.

In case of any Doubt regarding Membership you can mail us at [email protected]

Join Studycafe's WhatsApp Group or Telegram Channel for Latest Updates on Government Job, Sarkari Naukri, Private Jobs, Income Tax, GST, Companies Act, Judgements and CA, CS, ICWA, and MUCH MORE!"