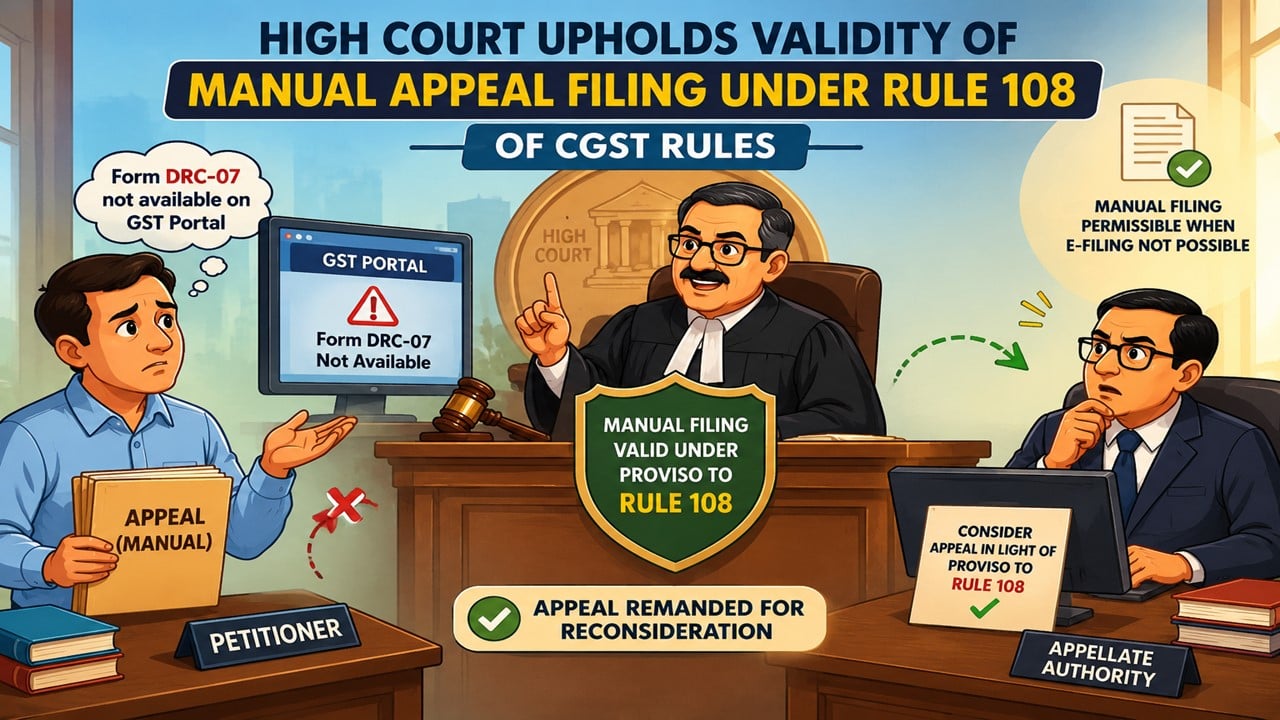

GST: Bombay High Court Upholds Validity of Manual Appeal:

The High Court held that since the GST portal did not provide the required form, manual filing was valid under the proviso to Rule 108, and directed the appellate authority to reconsider the appeal properly.

Tribunal Directed to Accept Manual Appeal Where E-Filing is Not Possible

GST: Bombay High Court Upholds Validity of Manual Appeal

The petitioner, Dinesh Dnyandeorao Pawade, approached the High Court because his appeal was not accepted by the Joint Commissioner (Appeals).

The main issue was that the appellate authority refused to accept his appeal in manual form. They insisted that the appeal must be filed only through the electronic GST portal as per Rule 108(1) of the CGST Rules, 2017.

However, the petitioner faced a practical difficulty. The required document, Form DRC-07, was not available on the GST portal. Because of this technical issue, it was not possible for him to file the appeal electronically.

[related id="420606."]

Despite this situation, the appellate authority did not consider the problem and still rejected the manual appeal.

The High Court observed that the authority had missed an important part of the law. Rule 108 has a proviso (an exception clause), which clearly states that if electronic filing is not possible due to technical issues or unavailability of required forms, then manual filing of the appeal is allowed.

Since Form DRC-07 was not available on the portal, the petitioner was justified in filing the appeal manually. The Court held that the appellate authority should have considered this practical difficulty instead of rejecting the appeal outright.

Therefore, the High Court ruled that the rejection of the appeal was not valid in law. It set aside the order and sent the matter back (remanded it) to the appellate authority.

The Court also directed the authority to reconsider the appeal properly, keeping in mind the proviso to Rule 108, and to decide the matter quickly and fairly.

About Author

Khushi Jain

Legal Content Writer

StudyCafe

StudyCafe Delhi, Delhi, India

Delhi, Delhi, India 80

80My Recent Articles

- ROC Chennai Orders Penalty for delay in filing MGT-17: Short Staff no Excuse

- Penalty Order Passed by ROC Chennai for Non-Disclosure in Form PAS-3

- ROC Imposes Penalty For Non-Compliance In Securities Allotment Filing

- From Rs. 275 Crore to Zero: United Breweries Gets Relief in Sales Tax Dispute

- Mere production of invoices, ledger extracts, and banking transactions not sufficient to stablish Valid Purchase: ITAT

Up Next

Loading suggestions…

Recent Posts

All Posts

Recent Posts

All Posts