Rule 88A Input Tax Credit Set off Explained with Examples

Rule 88A Input Tax Credit Set off Explained with Examples Government has eased cash flow concerns of trade industry with relaxations in ITC

Rule 88A Input Tax Credit Set off Explained with Examples

Government has eased cash flow concerns of trade industry with relaxations in ITC setoff mechanism vide Notification number 16/2019 - Central Tax dated 29th March 2019 by inserting Rule 88A.

Legal Text

Section 49A as inserted by Section 21 of CGST Amendment Act 2018 is given below for your reference:

Notwithstanding anything contained in section 49, the input tax credit on account of central tax, State tax or Union territory tax shall be utilized towards payment of integrated tax, central tax, State tax or Union territory tax, as the case may be, only after the input tax credit available on account of integrated tax has first been utilized fully towards such payment

Rule 88A reads as inserted Notification Number 16/2019 - Central Tax dated 29th March 2019 is given below for your kind referance:

Rule 88A. Order of utilization of input tax credit.- Input tax credit on account of integrated tax shall first be utilised towards payment of integrated tax, and the amount remaining, if any, may be utilised towards the payment of central tax and State tax or Union territory tax, as the case may be, in any order:

Provided that the input tax credit on account of central tax, State tax or Union territory tax shall be utilised towards payment of integrated tax, central tax, State tax or Union territory tax, as the case may be, only after the input tax credit available on account of integrated tax has first been utilised fully.

Rule 88A Input Tax Credit Set off Explained with Examples

Impact of Amendment

Earlier Government has changed the order of setoff by introducing section 49A w.e.f 1st February 2019 which said that IGST Credit should be set off fully before taking setting of CGST or SGST Credit.

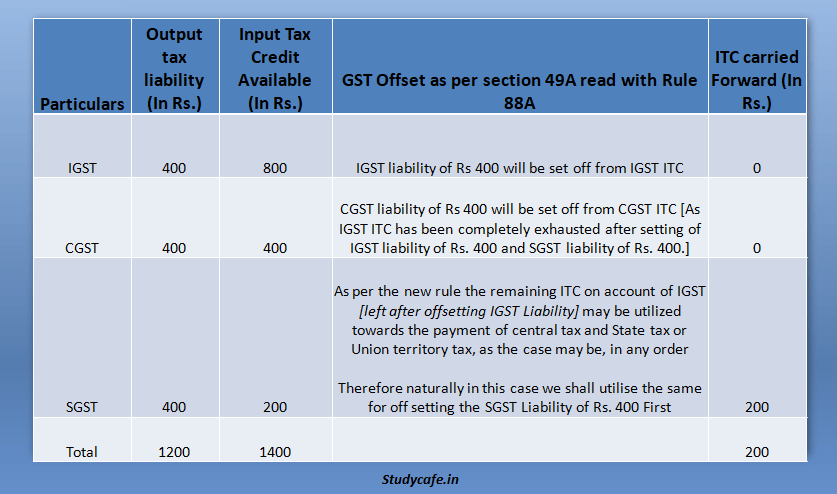

This has been illustrated by below mentioned example.

This has brought situation of cash crunch in the industry as was explained in my old article but the same has been eased by the GOM with relaxations in ITC setoff mechanism vide Notification number 16/2019 - Central Tax dated 29th March 2019 by inserting Rule 88A as this rule says that "Input tax credit on account of integrated tax shall first be utilised towards payment of integrated tax, and the amount remaining, if any, may be utilised towards the payment of central tax and State tax or Union territory tax, as the case may be, in any order"

Now lets Continue the above mentioned example to understand, what has changed.

[caption id="attachment_62433" align="aligncenter" width="837"] Rule 88A Input Tax Credit Set off Explained with Examples[/caption]

Below table shall illustrates the amendment in Order of Utilisation of ITC -

| ITC Balance | Utilized for Set off against liability of | Conclusion | |||

| IGST | IGST | CGST | SGST | UTGST | After utilization towards payment of IGST only, same can be used for set off of liability for CGST or SGST or UTGST (in any manner) |

| CGST | IGST | CGST | NA | NA | Cannot be used against SGST/UTGST |

| SGST | IGST | NA | SGST | NA | Cannot be used against CGST/UTGST |

| UTGST | IGST | NA | NA | UTGST | Cannot be used against CGST/SGST |

Note

1.) Taxpayers should note that Utilization of CGST/SGST/UTGST shall be allowed only when ITC for IGST has been first utilized in full.

2.) Taxpayers should note that Utilization of IGST ITC shall be allowed only when IGST liability has been fully paid first. After using it for IGST liability, it can be used for any other tax liability.D

Please remember that this article is based on personal understanding of Author which may be different from understanding of other person.

Compiled by CA Pratibha Goyal

Disclaimer : The entire contents of this document have been prepared on the basis of relevant provisions and as per the information existing at the time of the preparation. Although care has been taken to ensure the accuracy, completeness and reliability of the information provided, I assume no responsibility therefore. Users of this information are expected to refer to the relevant existing provisions of applicable Laws. The user of the information agrees that the information is not a professional advice and is subject to change without notice. I assume no responsibility for the consequences of use of such information. In no event shall I shall be liable for any direct, indirect, special or incidental damage resulting from, arising out of or in connection with the use of the information.

About Author

CA Deepak Gupta

Co Founder

StudyCafe

StudyCafe Delhi, Delhi, India

Delhi, Delhi, India 3423

3423My Recent Articles

- UltraTech Cement slapped with Rs. 808.78 Cr Income Tax Demand

- GST: High Court upheld constitutional validity of Section 16(2)(c), asks government to address ITC issues of genuine purchasers

- Old vs New Tax Regime for Tax Year 2026-27

- High court criticizes Income Tax Department for not releasing ITR Utilities despite 11 years of directions

- Fino Payments Bank CEO Rishi Gupta Gets Bail in GST Case, Bank Clarifies No Direct Link

Loading suggestions…

Recent Posts

All Posts

Tags

No tags yet.

Recent Posts

All Posts

Tags

No tags yet.