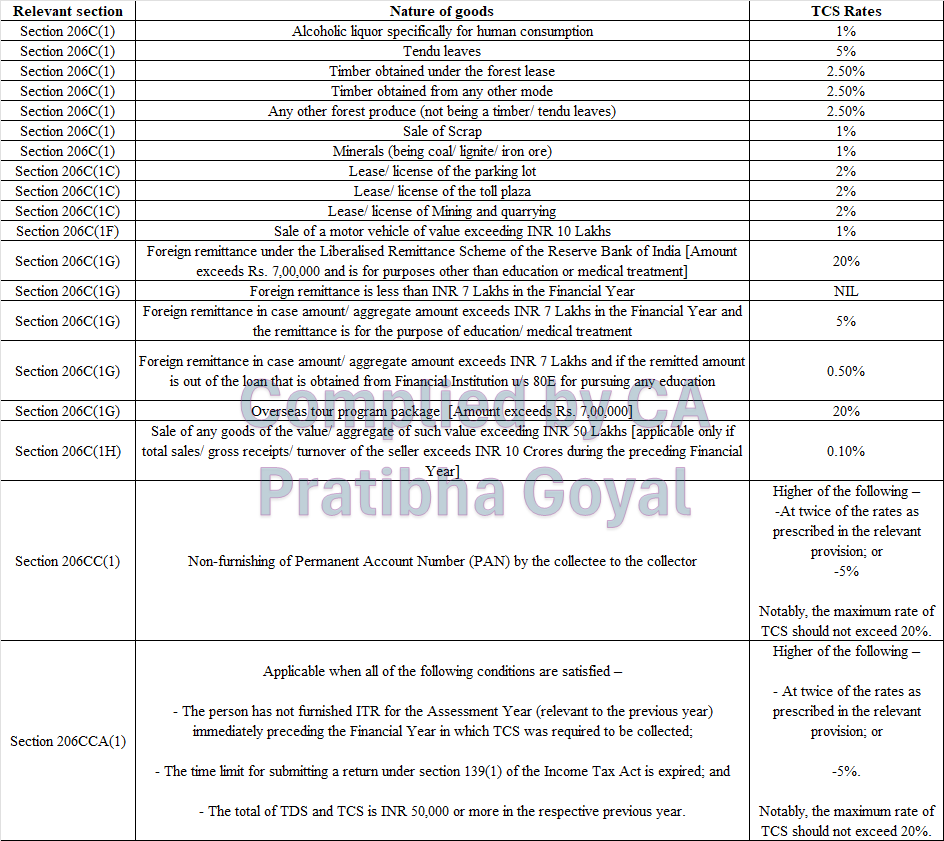

TCS Rate Chart For Assessment year 2025-26 or Financial Year 2024-25:

TCS Rate Chart For Assessment year 2025-26 or Financial Year 2024-25 The Article contains TCS Rate Chart for Assessment year 2025-26 or Financial Yea…

TCS Rate Chart

TCS Rate Chart For Assessment year 2025-26 or Financial Year 2024-25

The Article contains TCS Rate Chart for Assessment year 2025-26 or Financial Year 2024-25. Refer TCS chart for AY 2025-26 in pdf download, TCS rate chart for FY 2024-25 pdf, TCS rate chart FY 2024-25, TCS rates for FY 2024-25, TCS rate chart pdf for your compliances.

In this Article we shall discuss other compliances related to TCS as well, like: Provision for TCS, RATE OF TAX COLLECTION AT SOURCE (TCS), TIME OF DEPOSIT TCS, TCS Payment, TCS Return forms, DUE DATE OF SUBMISSION OF TCS RETURN, MODE OF FURNISHING RETURNS OF TCS, Certificate of TCS, Time limit for issuing TCS certificate, CONSEQUANCE ON DEFAULT IN TCS PROVISIONS

TCS Rate Chart For Assessment year 2025-26 or Financial Year 2024-25

Please note that provisions of Section 206C(1G)(a) - TCS on foreign remittance through Liberalised Remittance Scheme, Section 206C(1G)(b) - TCS on selling of overseas tour package, Section 206C(1H) - TCS on sale of goods over a limit [Not Applicable if the seller is liable to collect TCS under other provision of section 206C] have been introduced by Finance Act 2020 and are applicable with effect from 1st October 2020.

TCS Rate Chart For Assessment year 2021-22 or Financial Year 2020-21

| Section | Goods & Services liable to TCS | Rate of TDS applicable for the period | |

| 14-05-2020 to 31-03-2021 | 14-05-2020 - 31-03-2021 | ||

| Section 206C(1) | Alcoholic liquor for human consumption | 1% | 0.75% |

| Section 206C(1) | Timber obtained under Forest lease Timber obtained by any mode other than under a forest lease Any other forest produce not being timber or tendu leaves | 2.50% | 1.88% |

| Section 206C(1) | Tendu leaves | 5% | 3.75% |

| Section 206C(1) | Minerals, being coal or ignite or iron ore | 1% | 0.75% |

| Section 206C(1) | Scrap | 1% | 0.75% |

| Section 206C(1C) | Parking Lot | 2% | 1.50% |

| Section 206C(1C) | Toll Plaza | 2% | 1.50% |

| Section 206C(1C) | Mining & quarrying | 2% | 1.50% |

Basic Steps involved in TCS Compliance

- COLLECTION AT SOURCE UNDER SECTION 206(C)

- DEPOSIT OF TAX COLLECTED AT SOURCE IN GOVERNMENT’S TREASURY WITHIN THE STIPULATED TIME

- SUBMISSION OF TCS RETURN WITHIN STIPULATED TIME

- TAG OR ADD OF CHALLAN TO THE TCS STATEMENT

- DOWNLOAD OF TCS CERTIFICATE FROM TRACES

Provision for TCS

Profits and gains from the business of trading, grants of lease or license, sale of motor vehicle under section 206C as Income tax collected at source i.e. TCS Every person , being a seller shall at the time of debiting of the amount payable by the buyer to the account of buyer or at the time of receipt of such amount from the said buyer, whichever is earlier, collect from the buyer of such amount as income tax. TCS shall not be collected if buyer declares that purchase of goods shall be utilized for the purpose of manufacture, processing or producing articles or things.TIME OF DEPOSIT TCS

| Taxpayer | Date of Deposit |

| Is office of the Govt. and tax is paid without production of income tax challan. | On the same day on which tax is deducted |

| Is office of the Govt. and tax is paid with production of income tax challan. | On or before 7 days from the end of month in which tax is collected. |

| Tax is collected by a person other than office of Government | On or before 7 days from the end of month in which tax is collected. |

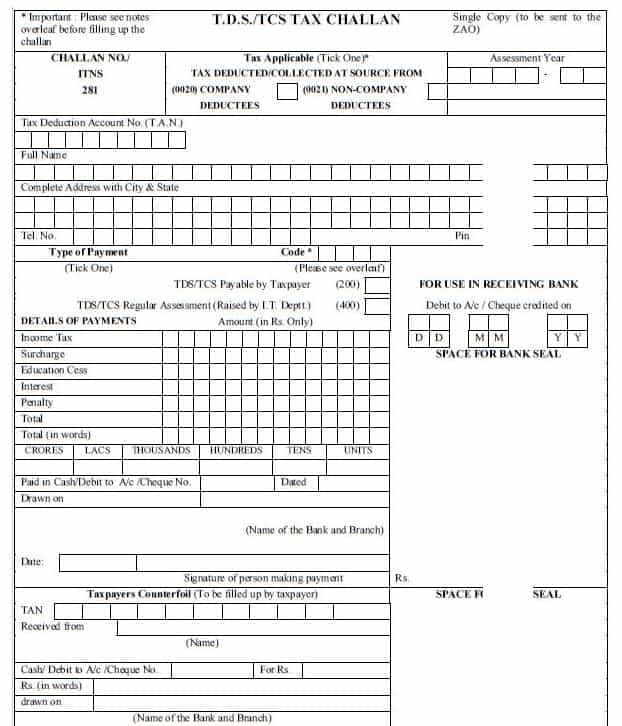

How to Make TCS Payment?

- TCS should be deposit in Challan No. 281

- TCS will have to deposit through internet banking.

- Indicate accurate TAN in challan

- Minor Head of Challan – 200 : TCS payable by tax payer

- Minor Head of Challan – 400: TCS Regular assessment raised by Income Tax Department.

- Amount of TCS, Interest, Late filing fee, penalty etc, should be separately shown while filing the challan

- Note down BSR code, Challan serial number, Date of payment, and amount of challan. This will help you in case challan is misplaced.

TCS Return form

TCS Return has to be submitted quarterly in Form No. 27EQ.Due Date of Submission of TCS Return form

Due Date of Submission of TCS Return form are given below:| Quarter | Period | Due Date |

| 1st Quarter | 1st April to 30th June | 15th July |

| 2nd Quarter | 1st July to 30th September | 15th Oct |

| 3rd Quarter | 1st October to 31st December | 15th Jan |

| 4th Quarter | 1st January to 31st March | 15th May |

How to Furnish Return of TCS

- In case where deductor or collector are an office of Govt. or Principal officer of a company or is person who is required to get his account audited u/s 44AB in immediately preceding financial year or when the numbers of collectee’s are more than 20, then TCS quarterly return shall be submitted electronically.

- Other than above, any other collector can submit TCS return either in paper format or electronically.

- Electronic return can be uploaded with Digital signature or verification of form 27A electronically

- Electronic return will be uploaded in FVU file

- FVU file can be generated through e-TCS RPU (return prepare utility) which is available in

- https://www.tin-nsdl.com/services/etds-etcs/etds-rpu.html

- In every quarter download latest e-TCS RPU

- In e-TCS return details of challan paid [ i.e. TCS amount, Interest, Fee, Other/penalty, BSR code, Challan serial No., Date of challan, Minor head] , details of deductee/collectee has to fill like section under which payment made, PAN, Name, Date of payment, Date deposit of TCS, amount paid, amount of TCS, Rate of TCS etc,.

Process of TCS return by the Income tax department through Traces

- After uploading of TCS return, IT department will process the return.

- Collector has to registered in Traces site and create User ID and Password

- After uploading return, TCS return can be process without default. If TCS return is process with default, that means there is some error in return and there may be demand of short deduction, interest, late filing fee or penalty.

- To know details of process with defaults, justification report has to be downloading.

- If there is demand of short deduction or interest or late filing fee, then collector has to deposit the demand under minor head 400 showing separately TCS, Interest, late fee or others penalty and add this challan to the respective quarterly statement.

- After Tag/add of challan, again TCS correction return has to be uploaded.

- When TCS return is process without default, that means TCS return process is completed. Thereafter TCS certificate has to download.

Certificate of TCS or TCS Certificate

Form 27D is the TCS Certificate. Same is issued within 15 Days of furnishing the TCS Return.Time limit for issuing TCS certificate

| For the Quarter ending | Form No 27D |

| Jun-30 | Jul-30 |

| Sep-30 | Oct-30 |

| Dec-31 | Jan-30 |

| Mar-31 | May-30 |

CONSEQUANCE ON DEFAULT IN TCS PROVISIONS

| Failure to collect tax at source and paid. [Sec 206C (7)] | Tax with interest @ 1% per month |

| Failure in furnish TCS return within stipulated time [U/S 234E] | Rs. 200 per day and shall not exceed the amount of tax deducted/collected. |

| Penalty for failure to furnish quarterly TCS return [271H] | Rs. 10000/- to Rs. 100000/- |

About Author

CA Pratibha Goyal

Co Founder

CA Pratibha Goyal is Chartered Accountant qualified in 2016, is a Member of The Institute of Chartered Accountants of India having wide experience in the field of Auditing, Taxation, ROC, GST and Secretarial matters etc.

She has written over a thousand articles & has made several videos on topics related to Auditing & Taxation. As a Speaker she has delivered various sessions on various branches of NIRC of ICAI.

CA Pratibha Goyal is Chartered Accountant qualified in 2016, is a Member of The Institute of Chartered Accountants of India having wide experience in the field of Auditing, Taxation, ROC, GST and Secretarial matters etc.

She has written over a thousand articles & has made several videos on topics related to Auditing & Taxation. As a Speaker she has delivered various sessions on various branches of NIRC of ICAI.

Studycafe

Studycafe New Delhi, Delhi, India

New Delhi, Delhi, India 1486

1486My Recent Articles

- Biggest Labour Reform in Indian History: 4 Labour Codes Effective from today

- Tax Audit and ITR Due date not extended in this case: Know More

- Government notifies Agreement and Protocol between India and Qatar [Read Notification]

- CA Breaking: Results of ICAI Examination to be announced soon, Know probable Date

- Breaking: GSTR-3B Due Date for September 2025 extended by CBIC amid Diwali Festivities

Up Next

Loading suggestions…

Recent Posts

All Posts

Tags

No tags yet.

Recent Posts

All Posts

Tags

No tags yet.