ITAT holds demat transfer taxable while permitting examination of other deduction and loss claims.

Meetu Kumari | Jun 17, 2026 |

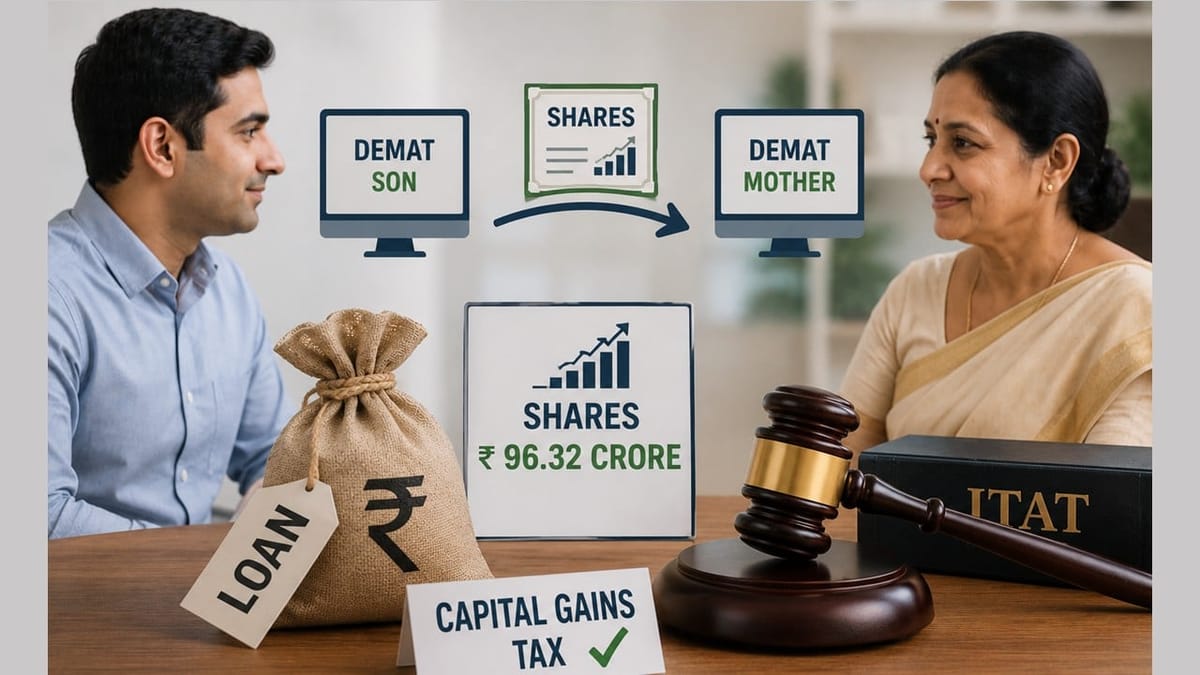

Son Transferred Shares Worth Rs. 96.32 Crore to Mother’s Demat Account as ‘Loan’; ITAT Upholds Capital Gains Tax on Transfer

The Delhi Bench of the Income Tax Appellate Tribunal (ITAT) dismissed the cross appeals filed by the Revenue and the assessee, Gurpreet Singh Dhillon, for Assessment Year 2013-14. The dispute primarily related to the taxability of shares transferred by the assessee to his mother, the allowability of interest expenditure under Section 57(iii), deduction under Section 54F, and set-off of derivative trading losses.

The assessee had filed his return declaring income of Rs.1.02 lakh. During scrutiny assessment, the Assessing Officer made several additions, including long-term capital gains of Rs.96.32 crore on transfer of shares, disallowance of interest expenditure claimed under Section 57(iii), denial of deduction under Section 54F, and rejection of set-off of F&O losses.

On the issue of interest expenditure, the Tribunal noted that the assessee had advanced loans to M/s Birdie & Birdie Realtors Pvt. Ltd. and claimed deduction of interest paid on borrowings against interest income earned. The CIT(A) had examined the flow of funds and found a direct nexus only in respect of a Rs.31 crore loan advanced during the relevant year out of funds borrowed from Religare Securities Ltd. Consequently, only proportionate interest expenditure of Rs.57.95 lakh was allowed under Section 57(iii), while the balance claim was disallowed. The Tribunal upheld this approach, observing that deduction under Section 57(iii) is available only where a direct nexus exists between borrowed funds and income-generating advances.

The major controversy concerned 31.73 lakh shares of Religare Enterprises Ltd. transferred by the assessee to his mother’s demat account, which the assessee described as a “loan of shares.” The tax authorities treated the transaction as a transfer attracting capital gains tax. Upholding this view, the Tribunal observed that once shares are transferred to another person’s demat account, the right to deal with and sell those shares passes to the recipient. The original holder loses control over the shares, making it a transfer within the meaning of Section 2(47) of the Income-tax Act. Accordingly, the capital gains addition computed by the Assessing Officer was sustained.

As an alternative claim, the assessee sought deduction under Section 54F on account of investment in a residential property worth about Rs.132.74 crore. Although the claim had not been made in the original return, the CIT(A) directed the Assessing Officer to examine and allow the deduction in accordance with law. The Tribunal affirmed this direction, holding that a legitimate claim can be considered during appellate proceedings if the necessary material is available on record.

The Tribunal also upheld the CIT(A)’s direction regarding the assessee’s claim for set-off of Rs.2.25 crore loss arising from futures and options trading. It observed that although the claim had not been made in the return, appellate authorities are empowered to entertain such claims and direct verification by the Assessing Officer. The AO was therefore directed to examine the claim and grant the set-off in accordance with Sections 70 and 71 of the Act.

Thus, the Tribunal dismissed both the Revenue’s appeal and the assessee’s appeal.

To Read Full Order, Download PDF Given Below

In case of any Doubt regarding Membership you can mail us at [email protected]

Join Studycafe's WhatsApp Group or Telegram Channel for Latest Updates on Government Job, Sarkari Naukri, Private Jobs, Income Tax, GST, Companies Act, Judgements and CA, CS, ICWA, and MUCH MORE!"