CBDT Empowers CPC Bangalore to Rectify and Issue Income Tax Demand in certain cases:

The CBDT has authorised select Commissioners of Income Tax to correct apparent tax errors, issue demands, and delegate powers for faster refund and assessment processing.

CBDT Grants Concurrent Powers to CITs for Quick Resolution of Tax Errors and Refund Issues

CBDT Empowers CPC Bangalore to Rectify and Issue Income Tax Demand in certain cases

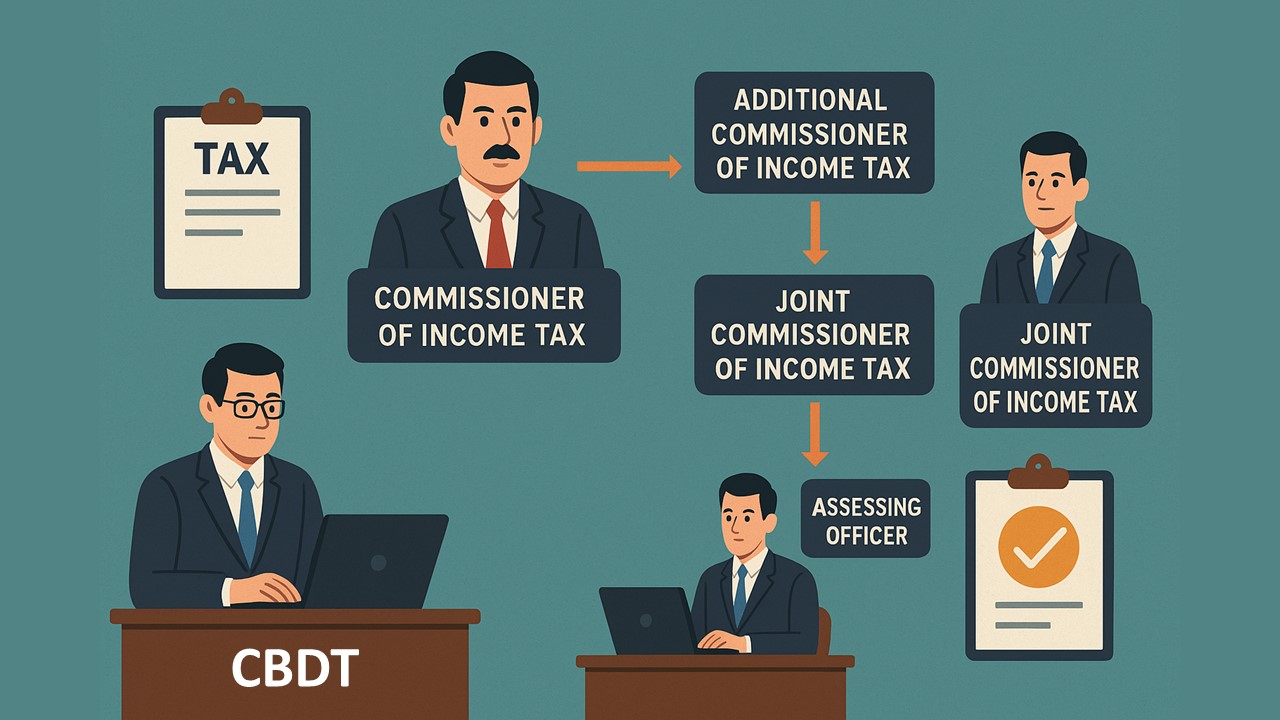

The Central Board of Direct Taxes (CBDT) under the Ministry of Finance (Department of Revenue) has issued an official notification (No. 155/2025), dated October 27, 2025, specifying powers to certain Commissioners of Income Tax (CITs) (details of CITs and their areas or jurisdictions are given below) and allowing them to further pass on these powers to officers working under them, to make the handling of mistakes refunds, and demands quicker and smoother. Here's the comprehensive guide on their concurrent powers:

(i) According to the notification, the Commissioner of Income-tax (mentioned below) is now permitted to exercise their concurrent powers.

1. These powers include correcting mistakes under Section 154 of the Income Tax Act 1961 that are clearly visible from the records. These include:

Refer to the official notification for complete information.

Refer to the official notification for complete information.

- Wrong calculation of tax or refund in any earlier order.

- Refunds were issued incorrectly or not processed properly.

- Ignoring prepaid tax amounts such as TDS, TCS, or advance tax.

- Missing any relief or deduction the taxpayer is eligible for.

- Wrong calculation of interest under Section 244A (interest on refund).

- Simply put, they can fix any obvious errors in tax computation, refund, or demand without needing a full reassessment.

Refer to the official notification for complete information.About Author

Saloni Kumari

Content Writer

Saloni is a Content Writer with 2+ years of experience at studycafe.in. She writes legal, taxation, and finance related content including GST, Income Tax etc. Skilled in translating complex judicial pronouncements and regulatory developments into clear, and reader-friendly articles. Experienced in covering judgements of ITAT, High Court, GSTAT, and news related to Income Tax, GST, and corporate law. She can be reached at [email protected].

Saloni is a Content Writer with 2+ years of experience at studycafe.in. She writes legal, taxation, and finance related content including GST, Income Tax etc. Skilled in translating complex judicial pronouncements and regulatory developments into clear, and reader-friendly articles. Experienced in covering judgements of ITAT, High Court, GSTAT, and news related to Income Tax, GST, and corporate law. She can be reached at [email protected].

StudyCafe

StudyCafe Delhi, Delhi, India

Delhi, Delhi, India 2486

2486My Recent Articles

- ITAT Grants Taxpayer Fresh Opportunity to Contest Rs 44.16 Lakh Addition After Finding No Decision on MeritsPremium

- Trust’s Sections 12AB and 80G Registration Cannot Be Denied Before Charitable Project Is Completed, Holds ITATPremium

- ITAT Says Identity and Creditworthiness Irrelevant Where Loan Was Directly Paid to Haryana Mining DepartmentPremium

- Earlier Rejection Cannot Be Sole Ground to Reject Fresh Section 12AB and 80G Registration Applications, Says ITATPremium

- Cash Deposited During Demonetisation Cannot Be Taxed Under Section 69A if Linked to Business, Holds ITAT Premium

Up Next

Loading suggestions…

Recent Posts

All Posts

Tags

Recent Posts

All Posts