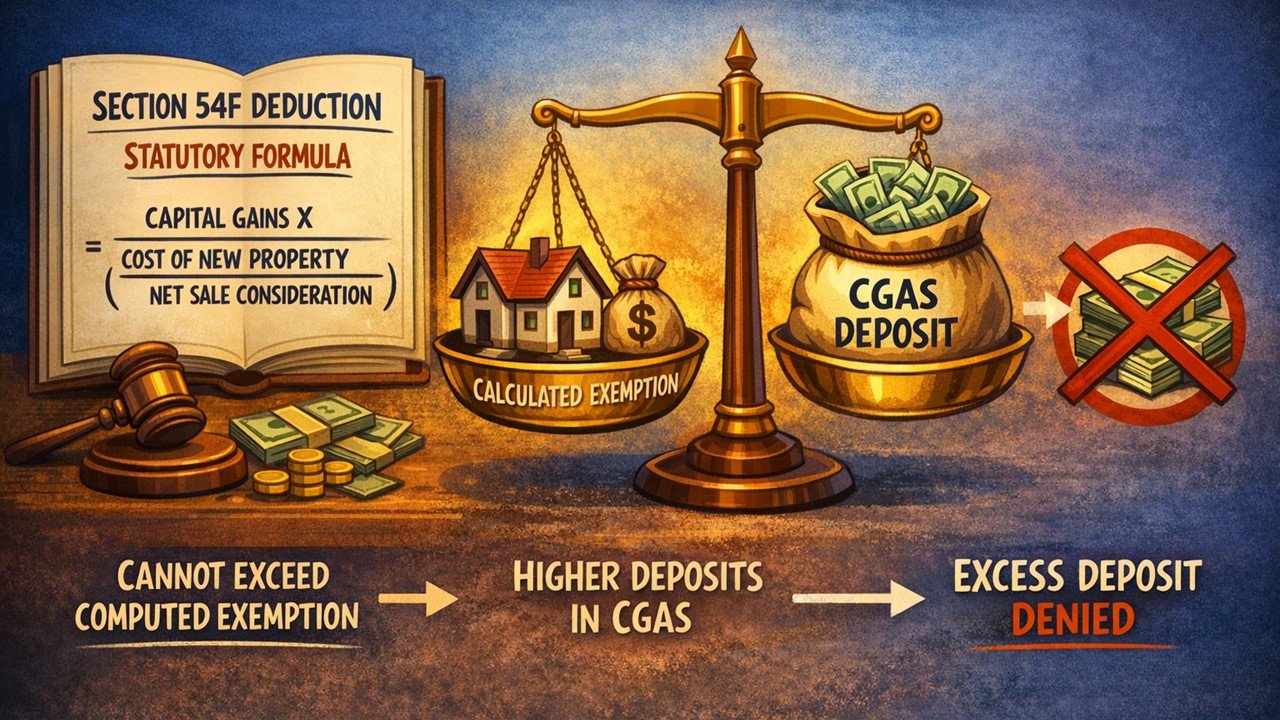

Section 54F Deduction Must Follow Statutory Formula, Not CGAS Deposit: ITAT:

The ITAT held that Section 54F deduction must strictly follow the statutory formula and cannot exceed the computed exemption merely due to higher deposits in the CGAS.

ITAT Clarifies CGAS Deposit Does Not Override Section 54F Calculation

Section 54F Deduction Must Follow Statutory Formula, Not CGAS Deposit: ITAT

The ITAT upheld the Rs. 3.91 lakh addition, ruling that the Section 54F deduction must follow the statutory formula and CGAS deposits cannot exceed the computed eligible exemption.

The Income Tax Appellate Tribunal (ITAT) Ahmedabad Bench “C” has announced its decision on an appeal filed by Sumit H. Bhagchandani against the Deputy Commissioner of Income Tax (DCIT), challenging an order dated August 21, 2025, passed by the CIT(A). The case is related to the Assessment Year 2017-18.

The assessee filed its income tax return (ITR) for the year in consideration, declaring total income at Rs. 2.31 crore. The return included LTCG (Long Term Capital Gain) of Rs. 3.76 crore arising from selling a plot of land on which the assessee had claimed exemption under section 54F of the Income-tax Act, 1961. He invested Rs. 33.36 lakh in the construction of a residential house and deposited Rs. 2.25 crore in the Capital Gains Account Scheme (CGAS), claiming a total deduction of Rs. 2.58 crore.

During the assessment of the return, the Assessing Officer (AO) used a specific statutory formula for the computation of deduction, which worked out at Rs. 2.54 crore. While the assessee had claimed a total deduction of Rs. 2.58 crore. Hence, the AO makes an addition of the excess claimed deduction, i.e., of Rs. 3.91 lakh, to the assessee's income. Completed the assessment, declaring the total income of the assessee at Rs. 2.35 crore.

The assessee argued that the full deposit in the CGAS (Capital Gains Account Scheme) should be treated as an investment and that he had actually spent more than the deposited amount. However, the Tribunal observed that Section 54F clearly provides a statutory formula for the computation of deduction, and the tax authorities had rightly calculated the eligible deduction of the assessee. While a deposit in the CGAS protects eligibility, it does not override the statutory method of calculation.

The tribunal found the disallowance purely arithmetical and in line with the law, hence upheld the impugned order of the CIT(A) and dismissed the appeal of the assessee.

About Author

Saloni Kumari

Content Writer

Saloni is a Content Writer with 2+ years of experience at studycafe.in. She writes legal, taxation, and finance related content including GST, Income Tax etc. Skilled in translating complex judicial pronouncements and regulatory developments into clear, and reader-friendly articles. Experienced in covering judgements of ITAT, High Court, GSTAT, and news related to Income Tax, GST, and corporate law. She can be reached at [email protected].

Saloni is a Content Writer with 2+ years of experience at studycafe.in. She writes legal, taxation, and finance related content including GST, Income Tax etc. Skilled in translating complex judicial pronouncements and regulatory developments into clear, and reader-friendly articles. Experienced in covering judgements of ITAT, High Court, GSTAT, and news related to Income Tax, GST, and corporate law. She can be reached at [email protected].

StudyCafe

StudyCafe Delhi, Delhi, India

Delhi, Delhi, India 2550

2550My Recent Articles

- CBIC Directs CGST Authorities to Share Data with State Mining Departments for Detecting GST Evasion in Illegal Mining Cases

- ICAI Publishes Copy of 77th Annual Report and Accounts of Institute for Year 2025-26 in Gazette of India

- Govt Proposes Major Amendments to Payment and Settlement Systems Act, 2007, and Income Tax Act, 2025

- ICAI Launches Multipurpose Empanelment Form (MEF) 2026-27 at meficai.org; File Before Aug 27

- ITAT Deletes Rs 43.04 Lakh Tax Addition, Says Mere Third-Party Records Cannot Establish Unaccounted PurchasesPremium

Up Next

Loading suggestions…

Recent Posts

All Posts

Recent Posts

All Posts