Taxpayer Wins: Tribunal Slams Unnecessary Re-investigation After Source of Funds Was Already Proven:

An appellate authority forced a "do-over" on a tax case despite the Assessing Officer already having officially verified and accepted the taxpayer's proof of funds

Tribunal Rejects Redundant Re-investigation After Funds Were Already Verified

Tax Addition Quashed After AO Verified Funds as Legitimate

Fact of the case

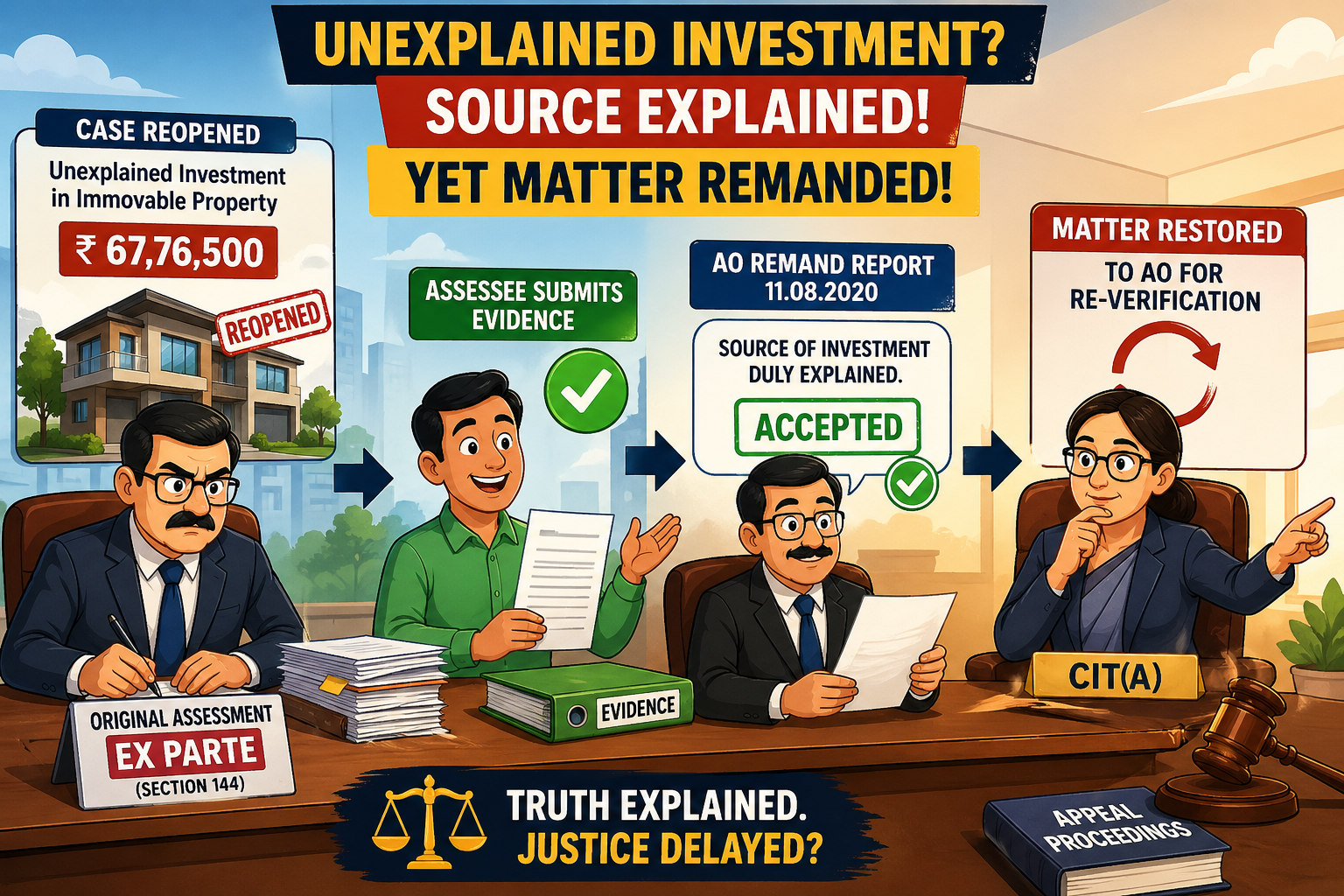

The assessee's case was reopened due to an unexplained investment in an immovable property worth Rs. 67,76,500. The original assessment was completed ex parte under Section 144 of the Act. During subsequent appellate proceedings before the CIT(A), the assessee provided evidence explaining the source of investment. A remand report submitted by the Assessing Officer (AO) on 11.08.2020 explicitly accepted that the source of investment was duly explained. Despite this, the CIT(A) restored the matter to the file of the AO for re-verification.

Issue of the case

Whether the appellate authority was justified in ordering a re-investigation when the assessing officer had already reviewed the evidence and confirmed the source of the investment was legitimate.

[related id="418091]

Decision of the Tribunal

The Income Tax Appellate Tribunal (ITAT) found that the issue of investment had already been thoroughly examined by the AO during the remand proceedings, who had confirmed the source was explained. Consequently, the tribunal held that the CIT(A)’s direction to restore the issue for re-verification was unwarranted and unjustified. The ITAT ordered the deletion of the entire addition of Rs. 67,76,500 and allowed the assessee's appeal.

About Author

Khushi Jain

Legal Content Writer

StudyCafe

StudyCafe Delhi, Delhi, India

Delhi, Delhi, India 80

80My Recent Articles

- ROC Chennai Orders Penalty for delay in filing MGT-17: Short Staff no Excuse

- Penalty Order Passed by ROC Chennai for Non-Disclosure in Form PAS-3

- ROC Imposes Penalty For Non-Compliance In Securities Allotment Filing

- GST: Bombay High Court Upholds Validity of Manual Appeal

- From Rs. 275 Crore to Zero: United Breweries Gets Relief in Sales Tax Dispute

Up Next

Loading suggestions…

Recent Posts

All Posts

Recent Posts

All Posts