A complete guide to all seven ITR forms for AY 2026-27, explaining who should file each form and how choosing the correct ITR can help avoid notices, penalties, and refund delays.

Vanshika verma | Jun 8, 2026 |

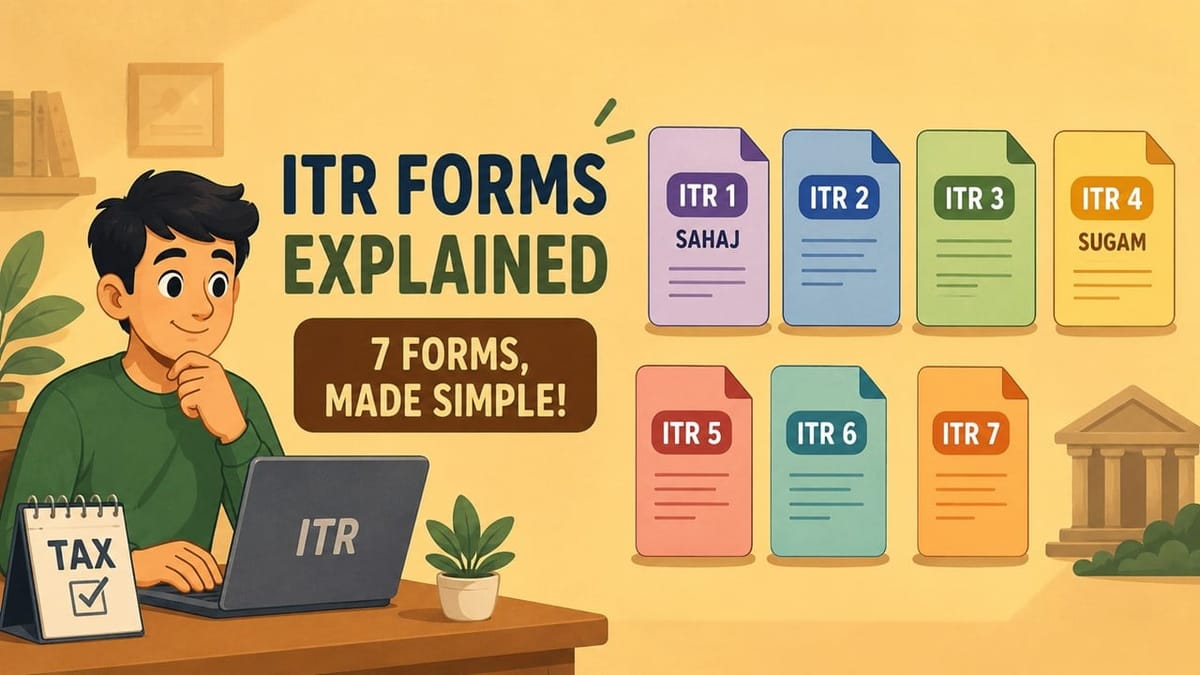

Filing Your ITR? Here’s a Simple Breakdown of All 7 Income Tax Return Forms

Choosing the correct ITR form is the first important step of filing your Income Tax Return (ITR) for Assessment Year (AY) 2026-27. Tax experts say a wrong form can make your return ‘defective‘ under Section 139(9) of the Income Tax Act. This can cause an income tax notice and delay in processing your tax refund.

In case if there is any defect in your return, the Income Tax Department generally allows 15 days’ time for the taxpayers to rectify the defect. If the problem is not rectified within the defined time limit, the return might be considered invalid. This can result in penalties, scrutiny from tax authorities and even denied refund claims.

The Income Tax Department has prescribed seven different forms of ITR for the purpose of correct filing by the taxpayers. Each form is designed to apply to a particular classification of taxpayers, determined by factors like income origins, residency status, and the type of income earned.

Before filing your return, it is important to know which ITR form is applicable to you. Using the correct format will help to ensure your return is processed smoothly, you get your refund faster and avoid unnecessary notices from the tax department. Here is a look at the seven ITR forms and who should use them:

ITR-1, also called Sahaj, is a simple income tax return form meant for resident individuals whose total annual income is up to Rs 50 lakh.

This form can be used by people who earn income from salary or pension. It is also suitable for those who have income from one house property and agricultural income up to Rs 5,000 during the financial year.

In addition, taxpayers can use ITR-1 if they earn income from other sources such as savings account interest, fixed deposit (FD) interest, or family pension.

The form also allows reporting of long-term capital gains under Section 112A up to Rs 1.25 lakh. It can further include certain income that is legally clubbed with the taxpayer’s income, such as income earned by a spouse or minor child in specified situations.

Who is not eligible to file ITR-1?

ITR-1 (Sahaj) is not available for everyone. It cannot be used by non-residents or Resident but Not Ordinarily Resident (RNOR) individuals. It is also not applicable to taxpayers whose total income exceeds Rs 50 lakh in a financial year.

People who earn income from a business or profession cannot file ITR-1. Similarly, individuals who own more than one house property are not eligible to use this form.

ITR-1 can also not be filed by company directors or by people who have invested in unlisted equity shares. Those who earn income from lotteries, racehorses, betting, or gambling activities are also excluded from using this return form.

In addition, taxpayers with agricultural income above Rs 5,000 cannot file ITR-1. The form is also not meant for individuals who have taxable capital gains, including long-term capital gains (LTCG) under Section 112A exceeding Rs 1.25 lakh during the year.

Further, individuals covered under Section 194N (related to tax deduction on large cash withdrawals) or those who have opted for deferred tax payment on ESOPs received from eligible start-ups are not eligible to file ITR-1.

ITR-2 is meant for individuals and Hindu Undivided Families (HUFs) who do not earn income from a business or profession. It can be used by taxpayers who earn income from salary, pension, house property, capital gains, foreign assets or income, and other sources.

The form is also applicable to individuals whose total income exceeds Rs 50 lakh in a financial year or who own more than one house property. Non-Resident Indians (NRIs), Residents but Not Ordinarily Residents (RNORs), and taxpayers who need to report foreign assets or foreign income can also file ITR-2.

In addition, individuals whose income includes that of a spouse or minor child under clubbing provisions, as well as partners in partnership firms receiving interest, salary, commission, bonus or remuneration from the firm, can use ITR-2, provided they do not have business income in their own name.

Who cannot file ITR-2?

ITR-2 cannot be used by taxpayers who earn income from a business or profession. Individuals who run a business, work as professionals, or have business income from a partnership firm are required to file other applicable income tax return forms instead.

ITR-3 is meant for individuals and Hindu Undivided Families (HUFs) who earn income from a business or profession. This includes business owners, freelancers, consultants, and partners in partnership firms who receive salary, commission, bonus, or other remuneration from the firm.

The form can also be used by taxpayers who have invested in unlisted equity shares during the financial year. Individuals earning business income along with salary, pension, capital gains, house property income, or income from other sources are also eligible to file ITR-3.

Who cannot file ITR-3?

Companies, charitable trusts, partnership firms, LLPs, Associations of Persons (AOPs), and Bodies of Individuals (BOIs) cannot file ITR-3. Taxpayers who are eligible to file ITR-1, ITR-2, or ITR-4 should also not use this form.

ITR-4, also known as Sugam, is designed for resident individuals, HUFs, and firms (excluding LLPs) that opt for the presumptive taxation scheme under Sections 44AD, 44ADA, or 44AE.

ITR-4: Who can file?

Taxpayers with a total income of up to Rs 50 lakh can use this form if they have income from salary or pension, own up to two house properties, have agricultural income of up to Rs 5,000 and earn certain income from other sources. Long-term capital gains under Section 112A up to Rs 1.25 lakh are also allowed.

Who cannot file ITR-4?

Non-Resident Indians (NRIs), Resident Not Ordinarily Residents (RNORs) and taxpayers with short-term capital gains cannot use ITR-4.

The form is also not available for taxpayers with long-term capital gains under Section 112A above Rs 1.25 lakh, agricultural income above Rs 5,000, income from more than two house properties, income taxable at special rates or investments in unlisted equity shares.

ITR-5 is meant for partnership firms, Limited Liability Partnerships (LLPs), Associations of Persons (AOPs), Bodies of Individuals (BOIs) and similar entities. However, entities that are required to file ITR-7 cannot use this form.

Most companies operating in India are required to file ITR-6. However, companies claiming exemption under Section 11 for income from charitable or religious activities must file ITR-7 instead.

ITR-7 is meant for charitable and religious trusts, political parties, educational institutions, hospitals, research associations, business trusts, investment funds, and other organisations that are required to file returns under Sections 139(4A) to 139(4F) of the Income Tax Act.

In case of any Doubt regarding Membership you can mail us at [email protected]

Join Studycafe's WhatsApp Group or Telegram Channel for Latest Updates on Government Job, Sarkari Naukri, Private Jobs, Income Tax, GST, Companies Act, Judgements and CA, CS, ICWA, and MUCH MORE!"