UPS Vs NPS: Here's How You Can Choose Right Option For Yourself:

The Government of India introduced Unified Pension Scheme (UPS) in the year 2024. The central government employees can now choose between the already existing NPS and newly introduced UPS.

All About Newly Introduced Unified Pension Scheme.

Table of Contents

UPS Vs NPS: Here's How You Can Choose Right Option for Yourself

Nearly 27 lakh central government employees have to choose if they wish to continue with the National Pension System (NPS) or switch to the freshly introduced Unified Pension Scheme (UPS), and this choice must be made by June 30, 2025. This crucial decision will define how comfortably these employees shall live after their retirement. This switch can only be opted for once and cannot be changed later on. Newly recruited employees also have the facility to opt for UPS within 30 days of their joining. Both NPS and UPS come with their own benefits, such as UPS giving the promise of guaranteed payouts and NPS providing greater flexibility.What is the Unified Pension Scheme (UPS)?

The UPS was recently introduced by the government in the year 2024. This scheme targets providing a guaranteed pension but includes a contribution model like NPS. As of now, UPS is available to all central government employees and may extend further to state government employees. The government introduced UPS as an alternative to the NPS. UPS been operational since April 1, 2025. The UPS essentially attempts to resolve the perceived flaws in the NPS:- Firstly, it comes with provisions for guaranteed pension payouts after retirement. If an employee works for more than 25 years in a central government posting, they are obliged to receive 50% of their average pay for the prior 12 months as a pension. A minimum of 10 years of service grants a pension of Rs. 10,000 per month.

- Secondly, the pension payment under the UPS will be indexed to inflation through periodic adjustments in the dearness relief.

- Can be opted for by any central government employee.

- Employees who are covered under NPS can go for UPS.

- Demands 10% employee contribution of basic pay plus DA.

- Guaranteed pension amount based on the last 12 months’ salary.

- Government contribution of 18.5%.

- Financial security for dependents ensured with family pension provision.

- Inflation-linked adjustments protect purchasing power.

- Gratuity benefits included.

- No payout of lump sum upon retirement.

- No clarification of taxation details at this stage.

- May not provide financial flexibility.

What is the National Pension Scheme (NPS)?

In the year 2004, the National Pension Scheme or NPS, was introduced. It is a market-linked pension scheme where an employee's retirement corpus depends on investment performance. This scheme was further extended to cover private-sector employees, NRIs, and self-employed individuals. Under the NPS, employees have to contribute regularly, and after retirement, 40% of the accumulated corpus is usable for annuity , the remaining 60% can be withdrawn without any burden of taxation. There is no fixed pension amount, as it depends upon investment performance. Eligibility Criteria for NPS- Government and private-sector employees: both can enroll.

- NRIs and self-employed individuals can also avail.

- Mandatory contributions are required during service.

- Higher returns, as it is linked to market investments.

- A withdrawal of partial lump sum (60%) is allowed upon retirement.

- Flexible in terms of choosing fund managers and investment options.

- NPS deduction under Sections 80C, 80CCD (1B), and 80CCD (2).

- No guaranteed pension, as it completely depends upon market performance.

- 40% of the corpus must be annuitized; this reduces immediate liquidity.

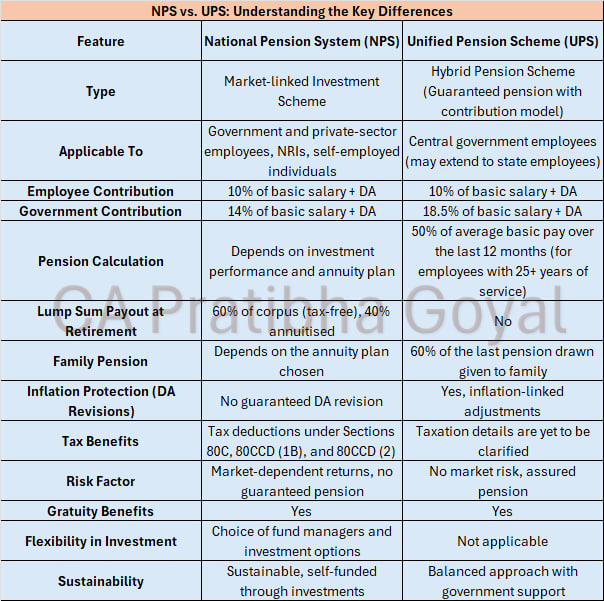

NPS vs. UPS: Understanding the Key Differences

Type: NPS is a Market-linked Investment Scheme, but UPS is a Hybrid Pension Scheme (Guaranteed pension with contribution model). Applicability: UPS is for Central government employees. It may be extended to state employees. NPS however was also extended to private-sector employees, NRIs, self-employed individuals besides government employees. Contribution:- Employee Contribution is same in NPS and UPS. (10% of basic salary + Dearness Allowance)

- Government Contribution is 18.5% of Basic Salary and Dearness Allowance in UPS and 14% of Basic Salary and Dearness Allowance in NPS.

- Depends on investment performance and annuity plan in NPS

- 50% of average basic pay over the last 12 months (for employees with 25+ years of service) in UPS

What to Choose Between NPS and UPS

Here's what you should keep in mind while choosing a pension scheme: For Flexibility and Market-Linked Growth: You should go for NPS.- Allows choosing investment options and fund managers.

- Tax benefits under Sections 80C, 80CCD (1B), and 80CCD (2).

- Private-sector employees, NRIs, and self-employed individuals can opt for this scheme.

- No guaranteed returns, as these depend upon market performance.

- Higher contribution of government (18.5%).

- Assured family pension and minimum pension.

- Guaranteed pension amount of 50% of the last 12 months' average salary (for employees with 25+ years of service).

- Details on taxation are yet unclear.

Conclusion

One should keep in mind their financial goals, job security, employer status and risk appetite while opting for a pension scheme.About Author

Shriya Mishra

Content Writer

Shriya writes engaging and easy-to-understand content on budgeting, mutual funds, insurance, income tax, GST, company law and financial planning. Her mission is to guide readers toward smarter money habits and long-term wealth creation. She can be reached at [email protected]

Shriya writes engaging and easy-to-understand content on budgeting, mutual funds, insurance, income tax, GST, company law and financial planning. Her mission is to guide readers toward smarter money habits and long-term wealth creation. She can be reached at [email protected]

Studycafe

Studycafe Delhi, Delhi, India

Delhi, Delhi, India 56

56My Recent Articles

- Income Tax Dept Breaks Silence: No Mass Scrutiny for Small Taxpayers

- GST Return Filing to Get Tougher from July 1: Major Changes You Must Know

- Tax Trouble for Delhivery: Rs. 1.36 Cr Penalty Order from Income Tax

- Canada to remove Digital Services Tax to Restart Trade Talks with US

- IEC Update Deadline Ends Today: Don't Miss Final Date to Avoid Penalties

Up Next

Loading suggestions…

Recent Posts

All Posts

Tags

No tags yet.

Recent Posts

All Posts

Tags

No tags yet.